Kentucky Mortgage Closing Costs Explained (2025 Homebuyer Guide)

Buying a home in Kentucky comes with one final step before you get your keys — closing costs. These are the fees and services required to finalize your mortgage, covering everything from the appraisal to title insurance. Whether you're purchasing with an FHA loan, VA loan, USDA Rural Housing loan, KHC program, or a Conventional mortgage, understanding these costs will help you budget and avoid surprises at the closing table.

💰 What Are Mortgage Closing Costs?

Mortgage closing costs are the final fees and charges due at settlement for a home purchase or refinance. These costs cover third-party services like appraisals, title searches, insurance, inspections, and lender processing fees. Unlike your down payment, closing costs are separate — and they can add up quickly.

In Kentucky, the total amount varies based on several factors:

- Loan type (FHA, VA, USDA, Conventional, KHC)

- Home price and location

- Down payment percentage

- Credit score and loan approval timeline

- County and local recording fees

- Lender and service provider choices

📋 Common Closing Costs in Kentucky (2025)

Here's a breakdown of typical closing costs you'll encounter as a Kentucky homebuyer:

| Fee Type | Typical Cost Range | Who Pays? |

|---|---|---|

| Appraisal Fee | $500–$800 | Borrower (upfront) |

| Home Inspection | $300–$700 | Borrower (optional but recommended) |

| Credit Report Fee | $50–$150 | Borrower |

| Loan Origination Fee | 0.5–3% of loan | Borrower |

| Title Search & Insurance | 0.5–1% of home price | Borrower (varies by county) |

| Recording Fees | $40–$200 | Borrower |

| Prepaid Taxes & Insurance | 6-12 months escrow | Borrower |

| FHA/VA/USDA Funding Fees | 0%–3.6% of loan | Borrower (can be financed) |

| Homeowners Insurance (1st year) | $800–$3000 | Borrower |

| HOA Fees (if applicable) | $100–$500 | Borrower |

🏡 Who Pays Closing Costs in Kentucky?

While most closing costs are paid by the buyer, there are several ways to reduce your out-of-pocket expenses. Here's how it works:

Buyer Pays (Standard)

As the borrower, you're responsible for most closing costs. However, you have options to reduce the burden.

Seller Concessions

The seller can contribute to your closing costs through what's called a "seller concession" or "seller credit." The maximum amount varies by loan type:

- FHA Loans: Up to 6% of the home purchase price

- VA Loans: Up to 4% of the home purchase price

- USDA Loans: Up to 6% of the home purchase price

- Conventional Loans: 3–9% depending on down payment (typically 3% with 25% down, up to 9% with 3% down)

- KHC Programs: Often allows up to 3-6% seller contribution

Lender Credits

Another way to reduce closing costs is through a lender credit. This works like this: you accept a slightly higher interest rate in exchange for the lender paying some or all of your closing costs. This is particularly helpful if you don't have enough cash at closing but plan to stay in the home for many years.

Financing Costs Into the Loan

With FHA, VA, and USDA loans, you can roll certain upfront fees (like FHA mortgage insurance or VA funding fees) directly into your loan amount. This reduces the cash you need at closing, though it does increase your monthly payment slightly.

🔍 Understanding Your Loan Estimate & Closing Disclosure

The federal government requires lenders to provide clear, standardized disclosures about your loan costs. Here's what you need to know:

Loan Estimate (Due Within 3 Business Days)

After you submit your mortgage application, your lender must provide a Loan Estimate within three business days. This document outlines:

- Loan terms and interest rate

- Monthly principal and interest payment

- Estimated closing costs (broken down by fee)

- Comparison of different loan options

Review this carefully and compare it with estimates from other lenders. Under RESPA (Real Estate Settlement Procedures Act), many of your closing costs cannot increase by more than 10% from the Loan Estimate to your final closing.

Closing Disclosure (Due 3 Days Before Closing)

Before your closing appointment, you'll receive a Closing Disclosure listing your final costs. This is your chance to verify that everything matches your Loan Estimate. You have the right to review this document for at least three business days before signing.

🎯 Kentucky Closing Costs by Loan Type

FHA Loans (First-Time Homebuyers)

FHA loans are popular with Kentucky first-time homebuyers because they allow lower down payments (3.5%) and more flexible credit requirements. However, FHA comes with upfront and annual mortgage insurance premiums:

- Upfront FHA Mortgage Insurance: 1.75% of loan amount (can be financed)

- Annual Mortgage Insurance: 0.45–0.80% annually (added to monthly payment)

- Total FHA Closing Costs: 1–7% of loan amount

VA Loans (Veterans & Active Duty)

VA loans offer excellent benefits for military members and veterans, with no down payment required and no mortgage insurance. Instead, there's a VA funding fee:

- VA Funding Fee: 2.3% of loan (first-time use, no down payment) — can vary based on service and down payment

- Total VA Closing Costs: 1-4% of loan amount

USDA Rural Housing Loans (Rural Kentucky)

USDA loans are designed for rural Kentucky properties with zero down payment required:

- USDA Guarantee Fee: 1% of loan (upfront, can be financed)

- Annual Mortgage Insurance: 0.35% annually

- Total USDA Closing Costs: 1–6% of loan amount

Conventional Loans

Conventional loans don't have government insurance fees, making them attractive once you have a higher down payment and good credit:

- Loan Origination Fee: 0.5–1%

- Private Mortgage Insurance (PMI): 0.5–2% annually (if down payment < 20%)

- Total Conventional Closing Costs: 1–5% of loan amount

Kentucky Housing Corporation (KHC) Loans

KHC programs offer first-time homebuyers down payment and closing cost assistance:

- Down Payment Assistance: Up to $12,500

- Closing Cost Assistance: Often available

- Interest Rate: Competitive rates

- Total KHC Closing Costs: Can be significantly reduced with assistance programs

💡 How to Reduce Closing Costs in Kentucky

Here are proven strategies to minimize your closing costs:

1. Compare Multiple Lenders

Don't just accept the first offer. Get Loan Estimates from at least 3 lenders. Even small differences in origination fees and closing costs can save you hundreds or thousands of dollars. Under federal law, many costs have a 10% limit on increases from estimate to final, so comparing early pays off.

2. Negotiate Seller Concessions

In today's market, sellers are often motivated to negotiate. Work with your real estate agent to request seller concessions to cover your closing costs. Remember the limits for each loan type (FHA: 6%, VA: 4%, USDA: 6%, Conventional: varies).

3. Explore Kentucky Housing Corporation (KHC) Programs

KHC closing cost assistance programs can cover $0 to 100% of your closing costs depending on your income, credit, and the specific program. As a Kentucky first-time homebuyer, you may qualify for up to $12,500 in down payment assistance plus closing cost help.

4. Ask About Lender Credits

Some lenders will absorb closing costs in exchange for a slightly higher interest rate. Calculate whether this makes sense long-term. If you plan to stay in the home for 5+ years, a lower rate usually outweighs the higher closing costs.

5. Roll Fees Into the Loan

With FHA, VA, and USDA loans, you can finance certain upfront fees (funding fees, mortgage insurance). This reduces cash needed at closing but increases your loan amount and monthly payment.

6. Shop for Services

Your lender cannot force you to use specific appraisers, inspectors, or title companies. Get competitive quotes and choose the best value.

7. Close Before Month-End

Closing late in the month can reduce your prepaid taxes and insurance (escrow), which lowers immediate out-of-pocket costs.

📊 Closing Costs Breakdown Example

Scenario: $300,000 home purchase with FHA loan, 3.5% down payment ($10,500), $289,500 loan amount, 6.5% interest rate

| Item | Cost |

|---|---|

| Appraisal | $650 |

| Credit Report | $40 |

| Loan Origination (0.75%) | $2,171 |

| Title Search & Insurance | $1,200 |

| Recording & Transfer Fees | $120 |

| Upfront FHA Mortgage Insurance (1.75%) | $5,067 |

| Homeowners Insurance (1 year) | $1,200 |

| Property Taxes (prepaid, 2 months) | $1,500 |

| TOTAL CLOSING COSTS | $11,948 |

With seller concessions up to 6% ($18,000), the seller could help pay a significant portion of these costs.

Ready to Get Started?

Get a personalized closing cost estimate and explore loan options that fit your budget.

Contact Joel Lobb, Kentucky Mortgage Broker

Specializing in FHA, VA, USDA & KHC Loans for Kentucky Homebuyers

NMLS #57916 | Equal Housing Lender

❓ Frequently Asked Questions

Can I negotiate closing costs in Kentucky?

Yes. You can negotiate with sellers through your real estate agent, ask lenders for credits or better terms, and shop around for services like appraisals and title insurance. Every dollar saved adds up.

Can I pay closing costs from my down payment savings?

No. Down payment and closing costs are separate. However, sellers can help via concessions, and lenders can offer credits. Additionally, FHA, VA, and USDA programs allow financing certain fees into the loan.

Are there any Kentucky-specific closing cost fees?

Kentucky counties have varying recording and transfer fees. Jefferson County (Louisville) fees differ from rural counties. Your lender will break these down in your Loan Estimate.

Can closing costs be rolled into my mortgage?

Yes, depending on your loan type. FHA, VA, and USDA loans allow you to finance upfront mortgage insurance and funding fees. Conventional loans typically don't allow this, but lender credits can help reduce upfront costs.

What if closing costs exceed my Loan Estimate?

Under RESPA, many closing costs cannot increase by more than 10% from your Loan Estimate to your Closing Disclosure. If you see major discrepancies, contact your lender immediately.

Does Kentucky have first-time homebuyer assistance?

Yes! The Kentucky Housing Corporation (KHC) offers closing cost assistance, down payment programs, and favorable rates for first-time buyers. You may qualify for $0 to $30,000+ depending on the program.

Call/Text -

Call/Text -

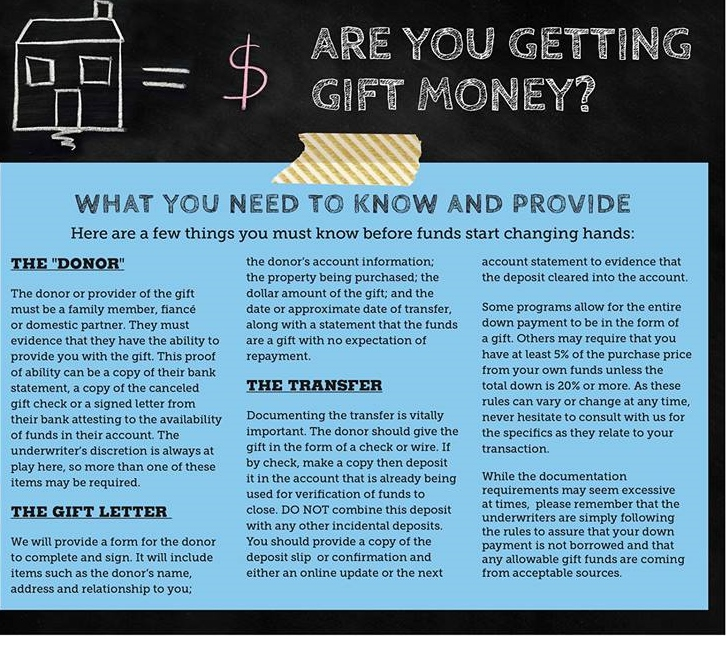

FHA gift funds can come from family members, employers, charities, and government programs

FHA gift funds can come from family members, employers, charities, and government programs