I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Kentucky USDA Rural Housing Eligibility Map and County List 2026 | Zero Down Homes

Kentucky USDA Rural Housing & Property Eligibility Guide for 2026

Kentucky homebuyers using the USDA Rural Housing program in 2026 need a fast and accurate way to verify whether a property is located in an eligible rural area.

This updated guide includes your Kentucky USDA map images, a full county eligibility list, income-limit guidance, and a simple tool to check property eligibility by address.

Check Kentucky USDA Property Eligibility for 2026

Enter the full property address below to instantly confirm whether the home is located in a USDA-eligible rural zone.

2026 USDA Property Eligibility County List for Kentucky

All non-hyperlinked counties are fully eligible.

Jefferson County (Louisville) and Fayette County (Lexington) remain completely ineligible for USDA Rural Housing in 2026 due to population size.

Adair

Allen

Anderson

Ballard

Barren

Bath

Bell

Boone

Bourbon

Boyd

Boyle

Bracken

Breathitt

Breckinridge

Bullitt

Butler

Caldwell

Calloway

Campbell

Carlisle

Carroll

Carter

Casey

Christian

Clark

Clay

Clinton

Crittenden

Cumberland

Daviess

Edmonson

Elliott

Estill

Fayette (ineligible)

Fleming

Floyd

Franklin

Fulton

Gallatin

Garrard

Grant

Graves

Grayson

Green

Greenup

Hancock

Hardin

Harlan

Harrison

Hart

Henderson

Henry

Hickman

Hopkins

Jackson

Jefferson (ineligible)

Jessamine

Johnson

Kenton

Knott

Knox

Larue

Laurel

Lawrence

Lee

Leslie

Letcher

Lewis

Lincoln

Livingston

Logan

Lyon

McCracken

McCreary

McLean

Madison

Magoffin

Marion

Marshall

Martin

Mason

Meade

Menifee

Mercer

Metcalfe

Monroe

Montgomery

Morgan

Muhlenberg

Nelson

Nicholas

Ohio

Oldham

Owen

Owsley

Pendleton

Perry

Pike

Powell

Pulaski

Robertson

Rockcastle

Rowan

Russell

Scott

Shelby

Simpson

Spencer

Taylor

Todd

Trigg

Trimble

Union

Warren

Washington

Wayne

Webster

Whitley

Wolfe

Woodford

Kentucky USDA Rural Housing Property Eligibility County List Map for Eligible Properties

USDA Property Eligibility Text Description County List for Kentucky

VA mortgage loans are one of the strongest home financing options available to Kentucky veterans and active-duty service members. With no down payment in most cases, flexible credit guidelines, and no monthly private mortgage insurance, the VA program can make homeownership in the Bluegrass State more attainable and more affordable.

On this page, you will find an overview of how VA loans work in Kentucky, what it takes to qualify, how they compare to other loan programs such as FHA and USDA, and how to work with a local VA mortgage specialist to structure your approval correctly.

What Is a VA Mortgage Loan?

A VA mortgage loan is a home loan backed by the U.S. Department of Veterans Affairs. The VA does not lend the money directly. Instead, approved lenders originate the loan, and the VA provides a guaranty. That guaranty reduces the lender’s risk and allows more flexible terms than many conventional mortgage programs.

Eligible borrowers include veterans, active-duty service members, qualifying members of the National Guard and Reserves, and certain surviving spouses who meet the VA’s service requirements.

Key Benefits of VA Loans for Kentucky Borrowers

No down payment in most cases when you have full VA entitlement and the property appraises for at least the purchase price.

Competitive interest rates that are often lower than comparable conventional mortgage options.

No monthly private mortgage insurance, which helps keep the total payment more affordable.

Flexible credit underwriting standards compared to many traditional loan programs.

Limits on certain closing costs and the ability to ask the seller for concessions toward closing expenses.

If you are comparing VA financing to other options, such as FHA or USDA Rural Housing, it can be helpful to review all three side by side. You can learn more about those programs here:

VA eligibility is based on service history and discharge status. In general, you may be eligible if you:

Are a veteran who meets minimum active-duty service requirements, or

Are currently on active duty, or

Are a qualifying member of the National Guard or Reserves, or

Are an eligible surviving spouse of a veteran.

You will also need a valid Certificate of Eligibility (COE), which confirms your entitlement status and whether you have used the benefit before. A VA-approved lender can often retrieve your COE electronically as part of the pre-approval process.

VA Loan Requirements in Kentucky

Credit Expectations

The VA does not set a hard minimum credit score, but lenders do. Most Kentucky lenders look for a score of around 580 or higher for VA loans. Some may consider exceptions with strong compensating factors such as solid income stability, verified reserves, or strong residual income.

If your scores are lower, it may be worth reviewing other options such as FHA or working through a short-term credit improvement plan. You can compare programs and credit score guidelines on these pages:

Lenders generally prefer to see at least two years of verifiable employment or income history, though there can be flexibility for certain situations:

Two years of continuous employment in the same line of work is ideal.

Self-employed borrowers are usually asked for two years of business tax returns.

Recently discharged service members may be able to qualify using their new civilian job offer and military history.

Recent college graduates sometimes qualify with their degree and new employment, even without a long work history.

Debt-to-Income (DTI) Ratio

The VA guideline ratio is 41 percent, especially on manually underwritten loans. Automated underwriting systems may approve higher ratios when compensated by strong residual income, stable employment, and solid credit history. The goal is to make sure the payment is sustainable given your overall obligations.

Second-Tier Entitlement

If you have used a VA loan before, you may still be able to obtain another VA mortgage using second-tier entitlement. This can allow you to:

Purchase another home while keeping your current VA-financed property, subject to entitlement and county-level limits, or

Obtain a new VA loan after paying off a previous one, even if your entitlement has not been fully restored yet.

Bankruptcy and Foreclosure Waiting Periods

VA guidelines provide a path back to homeownership after major credit events, but there are waiting periods:

Chapter 7 bankruptcy: typically two years from discharge.

Chapter 13 bankruptcy: usually after 12 months of on-time plan payments with trustee approval.

Foreclosure: generally a two-year waiting period before a new VA loan.

Kentucky Real Estate Market and VA Loans

Kentucky offers a mix of urban markets such as Louisville, Lexington, and Northern Kentucky, along with many suburban and rural communities. Home prices in much of the state are often below the national average, which works well with the VA program’s zero-down structure.

In some areas, veterans also compare VA financing with USDA Rural Housing loans, especially when the property is located in a USDA-eligible area. You can learn more about USDA’s zero-down option and compare it to VA here: Kentucky USDA / Rural Housing Loans.

Typical Steps to Secure a VA Loan in Kentucky

Confirm basic VA eligibility and request or retrieve your Certificate of Eligibility.

Connect with a VA-approved Kentucky lender who understands local guidelines and property types.

Complete a pre-approval, including credit review, income documentation, and a preliminary payment analysis.

Begin home shopping with a purchase price range and estimated payment in mind.

Once under contract, order the VA appraisal and complete any additional inspections.

Provide any final documents requested by underwriting and move to closing.

VA Loan Limits and Entitlement

For borrowers with full entitlement, there is no VA-imposed loan limit. The maximum loan amount is based on income, credit, residual income, and lender overlays. For borrowers with partial entitlement, county loan limits and entitlement formulas may apply.

Appraisal, Property Standards, and Termite Requirements

VA Appraisal

A VA-approved appraiser will review the property to ensure that it supports the purchase price and meets the VA’s Minimum Property Requirements. This includes basic safety, soundness, and sanitation standards. Turn times typically run about seven to ten days, depending on volume and location.

Termite Inspection

In most parts of Kentucky, a wood-destroying insect (termite) inspection is required for VA loans. The seller often pays for this inspection, though this can be negotiated as part of the purchase contract.

Average Time Frame to Close a VA Loan

Most VA loans in Kentucky close in about 30 to 45 days. This is slightly longer than some conventional files due to the appraisal process and specific documentation requirements, but with complete paperwork and responsive communication, the timeline can often be managed effectively.

Common Issues That Can Delay or Prevent Closing

Property condition problems that do not meet VA Minimum Property Requirements.

An appraisal value that comes in below the contract price, requiring renegotiation or additional funds.

Job changes, reduced hours, or loss of income during the loan process.

New debt taken on before closing that pushes the debt-to-income ratio too high.

Insufficient funds for closing costs or required reserves.

Title or legal issues with the property that must be resolved before closing.

With proper planning, most of these issues can either be avoided or addressed early enough in the process to keep the file moving forward.

Working with a Local Kentucky VA Mortgage Specialist

Because VA loans have their own rules around entitlement, residual income, property standards, and closing costs, it helps to work with a loan officer who understands the details and has experience with Kentucky veterans and active-duty buyers.

About Joel Lobb

Joel Lobb is an Army veteran and experienced mortgage professional who has focused his practice on helping Kentucky homebuyers, including many VA borrowers, structure approvals that fit both their budget and long-term plans.

Clients frequently mention clear communication, realistic expectations, and a hands-on approach from application through closing. Whether it is a first VA purchase, a move to a larger home, or combining a VA purchase with a Kentucky Housing Corporation program, Joel’s focus is on building a complete, sustainable financing plan.

What Veterans Say

Past clients describe the process as straightforward and organized, even when timelines are tight or credit profiles are complex. Many note that the payment and structure ended up better than they expected at the beginning of the process.

Contact Joel Lobb — Mortgage Broker, FHA, VA, KHC, USDA

Address: 10602 Timberwood Cir, Suite 3, Louisville, KY 40223

If you are a veteran, active-duty service member, or surviving spouse considering a VA loan in Kentucky, you can request a free consultation to review your options and compare VA with FHA, USDA, and KHC programs based on your credit, income, and timeline.

My wife and I have struggled most of our lives with poor choices in marriage or in what I will call lifestyle choices but the one thing that we had to do on our own, and that was to just pay my bills on time and believe it or not that wasn't as easy as one might think. I went through a lot of different banks and/or loan officers,or bank reps. Then thru my researching came across Joel,Jeana and I still believe that God the Father lead us to Joel. You see I'm on a fixed income and was barely able to get from month to month. W ith no money down and on a very short time limit Joel was to get us into home that more than met our needs. It met our wants as well needs and our is more than 2X the size of the house we were renting, And 4X the size of the outside of the house we were renting. And for only $160.oo more a month than what we were paying in rent. A lot of people said it couldn't be done even people in tha thefield . What I know is that Joel Lobb worked extra hard and longer hours to achieve my wife and I's dreams even though we had a lifetime of adverseties I don't think of myself as being special. I do however believe that Mr.Lobb worked as hard for me as he does for any of his other clients. He was always transparent and tanaitous in his work ethics. So in my experiences with people in general I think it would be a good idea to give Joel and the mortgage company he represents a serious try.

Joel did an outstanding job. I am a 100% disabled retired Army Soldier. My wife and I have never bought a house. Joel made this process seem so easy it was scary. We found our 23acre ranch and put a bid on it and Joel did the rest. He made this process easier than buying our truck. We were even out of state at the time of closing and it was still no problem for Joel. My wife and I both highly recommend Joel for your home buying, whether it is your first or retirement. Thank you Joel, we Love our first and retirement home. Dennis and Shannon Jackson

Joel is the best mortgage guru in town. My wife and I were first time homebuyers via VA loan moving from NY to KY. He made the process of buying a home smooth and streamlined. We had no worries and everything went flawless. Thank you Joel!

Absolutely Amazing!! I emailed Joel after I had just got a denial from a bank and just thought i would try to get some advice on what my next steps would be to get a house. I honestly didn't expect to even get a reply because my credit is not great. That was about a week and a half ago. I just signed a contract on a house last night. ONLY because of Joel Lobb. He even worked with us throughout the weekend, which shocked me. Best decision I have ever made. THANK YOU SO MUCH FOR WORKING WITH US THROUGHOUT THE ENTIRE PROCESS.

Contact Joel Lobb Today Army Veteran with 20 years Mortgage Loans in KY

Don't wait to start your journey to homeownership with a VA Mortgage. Contact Joel Lobb now:

Joel is ready to answer your questions, address your concerns, and guide you through the entire VA loan process. With his expertise, you can confidently take the next step towards owning your home in Kentucky.

Schedule your free VA loan consultation with Joel Lobb today and take the first step towards your new home!

VA mortgage loans Kentucky, Kentucky VA home loans, veteran homeownership Bluegrass State, no down payment mortgages Kentucky, VA loan benefits Kentucky, VA loan requirements, VA loan credit score, VA loan work history, VA second tier entitlement, VA loan debt ratio, VA loan appraisal Kentucky, Joel Lobb VA loan expert

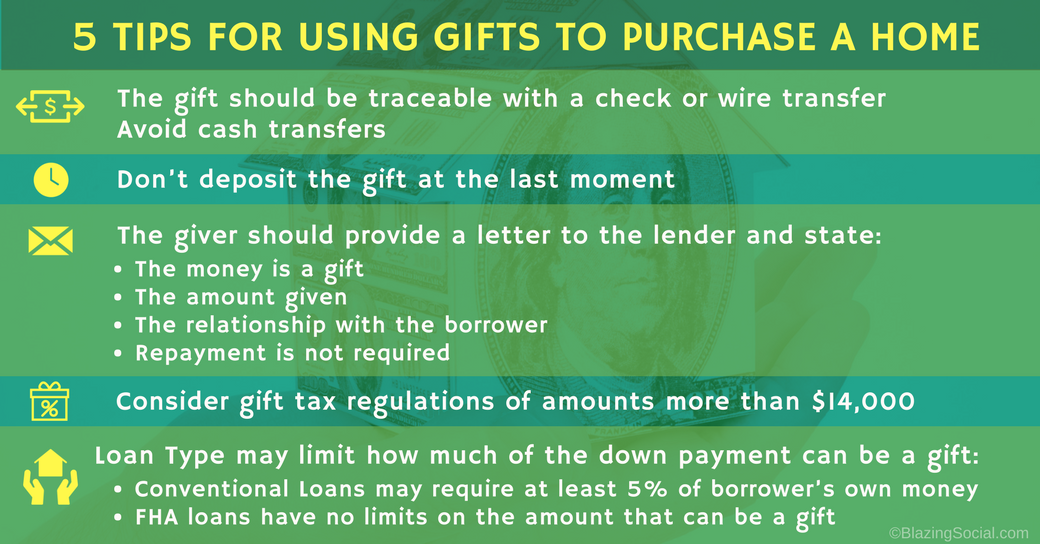

Using Gift Funds for a Down Payment in Kentucky (Updated 2025)

Many Kentucky homebuyers rely on financial help from family or close friends when buying a home. Gift funds can make the upfront investment far more manageable and can strengthen a buyer’s overall approval profile. Here is a clear breakdown of how gift money works across today’s loan programs and what documentation lenders require to use it.

Who Can Give a Down Payment Gift?

Eligible donors usually include parents, grandparents, children, siblings, fiancés, domestic partners, or other close family members. FHA and VA also allow gifts from close friends with a documented long-standing relationship. Gifts from sellers, builders, real estate agents, or anyone with a financial interest in the sale are not allowed unless structured as an approved credit through the contract.

How Gift Funds Help

Gift funds can reduce the cash needed to close and may help the loan qualify more easily. Lower borrower-funded contributions can improve reserves, reduce debt-to-income stress, and in some cases improve pricing. For first-time homebuyers in Kentucky using programs such as FHA, VA, USDA, or KHC, gift funds remain one of the most common tools to get to the closing table with minimal cash.

Conventional Loan Gift Rules (Fannie Mae vs. Freddie Mac)

Fannie Mae

100% of the down payment can be gifted on one-unit homes.

No minimum borrower funds required unless the property is a multi-unit or second home.

Freddie Mac

Often requires at least 5% of the purchase price from the borrower’s own funds if the down payment is under 20%.

Some lenders still follow this rule even when overlays vary.

Gift Documentation Requirements

Signed gift letter stating no repayment is expected.

Donor’s name, relationship, and contact information.

Proof of donor’s ability to give (bank statement or screenshot).

Proof the gift was transferred into the borrower’s account.

Gift Tax Considerations

Gift tax rules apply to the donor, not the buyer. The IRS allows an annual exclusion per donor, per recipient. Larger gifts may require a simple tax form from the donor, but this rarely affects the mortgage process. Underwriting only cares that the funds are a legitimate gift and are fully documented.

Using Gift Funds with Kentucky Housing Corporation (KHC)

Kentucky Housing Corporation allows gift funds with Regular DPA and SmartBuy DPA programs. These can be applied to minimum investment, closing costs, or prepaid expenses. For buyers aiming to bring little to no money to closing, combining gift funds with KHC assistance and seller credits can be a strong structure.

Avoid cash deposits; always use traceable transfers.

Have donors coordinate with your loan officer before sending funds.

Keep all statements, screenshots, and receipts.

Notify your lender early so the gift is structured properly.

Final Thoughts

Gift funds are a powerful way to reduce or eliminate upfront cash requirements. FHA, VA, USDA, and most Conventional programs allow them with proper documentation. Combined with Kentucky Housing Corporation assistance, many borrowers can reach the closing table with minimal or even zero out-of-pocket cost.

For help structuring your loan with gift funds or Kentucky first-time buyer programs, contact:

Joel Lobb, Mortgage Loan Officer

Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA

NMLS 57916 | Company NMLS 1738461

Call or Text: 502-905-3708

kentuckyloan@gmail.com

www.mylouisvillekentuckymortgage.com

Using Gift Funds for a Down Payment in Kentucky (Updated 2025)

Many Kentucky homebuyers rely on financial help from family or close friends when buying a home. Gift funds can make the upfront investment far more manageable and can strengthen a buyer’s overall approval profile. Here is a clear breakdown of how gift money works across today’s loan programs and what documentation lenders require to use it.

Last Updated: September 2025 | By Joel Lobb, Kentucky Mortgage Expert | NMLS #57916

Think a 580 credit score means you can’t buy a home in Kentucky? You can. This guide shows how FHA, VA, and USDA approvals work for fair-credit borrowers.

Quick answer: A 580 credit score can be approved in Kentucky through FHA, VA, or USDA. We do these approvals across the state every month.

Understanding your 580 credit score in Kentucky

A 580 score is in the fair range. While conventional loans and KHC down payment assistance typically want 620+, FHA, VA, and USDA were built to help modest credit histories become homeowners.

Where 580 sits — and why government-backed loans still work.

FHA loans for 580 credit scores in Kentucky

Why FHA fits: 3.5% minimum down payment at 580, available statewide, gifts and seller credits allowed, flexible underwriting, assumable for resale value.

Credit score: 580 qualifies for 3.5% down

DTI target: 45.99 on front end and 56.99 on a AUS approval and on manual underwriting approvals can do go 40% to 50% with compensating factors % or lower when possible

Credit improvement strategies to get your score above 580

Pay down credit cards under 30% utilization

Dispute errors; remove active disputes before underwriting

Document rental history; add a secured card if file is thin

Avoid new credit until after closing

Quick wins that can move a 580 into better pricing or KHC eligibility with a 620 score

Real Kentucky success stories

Jennifer (Lexington): 583 score → FHA 3.5% down; seller-paid costs → closed on $175k home

David (Warren County): 589 score → USDA zero down in eligible area → ownership on a teacher’s salary

Maria (Louisville): 584 score veteran → VA zero down, no MI → competitive monthly payment

Frequently asked questions

Can I really get approved with a 580 credit score in Kentucky?

Yes. We close 580-score FHA/VA/USDA approvals every month. Government-backed programs are designed for fair-credit borrowers with stable income.

What is the minimum down payment at 580?

FHA: 3.5% down. VA: $0 down for eligible borrowers. USDA: $0 down in eligible rural areas.

How long does approval take?

Pre-approval: same day. Clear-to-close typically 18–30 days after contract; total 30–45 days.

Will my rate be higher at 580?

Usually modestly higher than prime-credit, but FHA/VA/USDA pricing is often competitive. You can refinance later as credit improves.

Should I wait to improve credit before applying?

If you’re ready to buy and income is stable, apply now. We can pair approval with a credit plan and revisit refinancing later.

Your next step: get pre-approved so you can shop with confidence.

Joel Lobb is a licensed Kentucky Mortgage Loan Officer (NMLS #57916) with 20+ years of experience. He specializes in government-backed mortgages for fair-credit borrowers and has helped more than 1,300 Kentucky families buy homes.

Educational only; not financial advice. Programs, rates, and requirements change. Not all borrowers qualify. Not endorsed by FHA, VA, USDA, or any government agency. Joel Lobb is licensed to originate mortgages in Kentucky only.

Kentucky Mortgage Credit Score Requirements for First-Time Homebuyers (2025 Guide)

Obtaining a mortgage pre-approval is one of the most important first steps for Kentucky first-time homebuyers. Your credit score is a key factor lenders use to determine which loan programs you qualify for, your interest rate, and your monthly payment.

Conventional loans are offered by private lenders and are usually a better fit for buyers with stronger credit profiles.

Minimum credit score: Typically 620

Minimum down payment: Often 3% for first-time homebuyers

Other factors: Tighter debt-to-income (DTI) and reserve requirements compared to government-backed loans

As credit scores rise above 680 and especially above 700, borrowers may see improved interest rates and lower mortgage insurance costs.

Kentucky FHA Loans

Kentucky FHA loans are insured by the Federal Housing Administration and are popular among first-time homebuyers because of their flexible credit and down payment requirements.

580+ credit score: Eligible for a 3.5% down payment

500–579 credit score: Requires a 10% down payment

More flexible on: Past credit issues and higher DTIs when supported by compensating factors

Example: A buyer with a 575 credit score may still qualify for FHA financing with a 10% down payment, making homeownership possible even with imperfect credit.

Kentucky VA Loans (For Eligible Veterans & Service Members)

Kentucky VA loans are designed for eligible active-duty military, veterans, and some surviving spouses. They are one of the strongest options for those who qualify.

Official VA guideline:No minimum credit score set by the VA itself

Lender overlays: Many Kentucky lenders use internal minimums, often around 600–620

Benefits:0% down payment, no monthly mortgage insurance, and competitive interest rates

Even when scores are under 620, approvals may still be possible with strong income, clean recent payment history, and adequate residual income.

Kentucky USDA Rural Housing Loans

USDA Rural Housing loans are designed for eligible rural areas and qualified borrowers who meet income limits.

Typical minimum credit score: Around 620 for most lenders

Down payment:0% down (no down payment required)

Location requirement: Property must be in a USDA-eligible rural area

Some lenders may consider scores below 620 with strong compensating factors, but automated underwriting approvals are more common with scores at or above 620.

Kentucky Housing Corporation (KHC) offers state-level assistance such as down payment and closing cost help, often paired with FHA, VA, USDA, or conventional first mortgage programs.

KHC FHA/VA/USDA minimum score: Typically around 620

KHC Conventional minimum score: Often around 660

Benefits: Down payment assistance, potentially lower upfront cash-to-close, and programs tailored to first-time homebuyers

KHC programs can be layered with federal loan options, making them a powerful tool for Kentucky buyers who need help with down payment or closing costs.

Comparative Credit Score Table for Kentucky Mortgage Programs

Loan Program

Minimum Credit Score

Key Notes

FHA

580+ (3.5% down)

500–579 requires 10% down payment

VA

No official VA minimum

Most lenders use internal overlays around 600–620

USDA

Typically around 620

0% down, property must be in an eligible rural area

Conventional

620

3% down for first-time buyers; stricter guidelines

KHC FHA/VA/USDA

620

Can include down payment assistance and closing cost help

KHC Conventional

660

Higher score required; competitive rate and MI options

What These Credit Scores Mean for Kentucky Buyers

1. FHA – Most Flexible for Lower Credit Scores

For buyers in the 500–620 range, FHA is often the most realistic starting point. FHA’s flexible guidelines on credit history, debt-to-income ratios, and past issues (like collections or late payments) make it a strong option for rebuilding or recovering credit.

2. VA – Best Value for Eligible Veterans and Service Members

VA loans offer some of the lowest total monthly payments due to no monthly mortgage insurance and competitive rates. Even though there is no official VA minimum credit score, most lenders prefer higher scores for smoother approvals. However, approvals with scores under 620 are still possible with the right profile.

3. USDA – Great for Rural Kentucky Buyers

USDA loans help buyers in designated rural areas purchase with no money down. Most lenders look for at least a 620 score to receive a favorable automated underwriting result. Manual underwrites can be done with lower scores, but the guidelines become tighter.

4. Conventional – Strong Scores Rewarded with Better Pricing

Conventional loans reward stronger scores with better pricing and cheaper mortgage insurance. At 620, many buyers will qualify, but at 680+ and especially 740+, mortgage insurance and rate options usually improve noticeably.

5. KHC – State Support for Kentucky First-Time Buyers

KHC programs combined with FHA, VA, USDA, or conventional loans can significantly reduce the cash needed to close. For many first-time buyers, KHC’s assistance is what makes the purchase possible, especially when savings are limited.

Next Steps for Kentucky First-Time Homebuyers

Even a modest credit score improvement of 20–40 points can sometimes result in:

Lower interest rates

Cheaper mortgage insurance

Stronger approval chances

Higher maximum qualifying purchase prices

If you are unsure which program fits you best, a tailored pre-approval review can compare FHA, VA, USDA, KHC, and conventional loan options side-by-side based on your income, credit, and goals.

I work with Kentucky first-time homebuyers every day and can help you understand where your credit stands today, what you qualify for now, and what small changes might help you qualify for better terms.

Contact Joel Lobb for a Kentucky Mortgage Pre-Approval

Joel Lobb

Mortgage Loan Officer – FHA, VA, USDA, KHC, Conventional NMLS #57916 | Company NMLS #1738461

Serving Kentucky first-time homebuyers with FHA, VA, USDA, and KHC mortgage options, plus conventional loan programs tailored to your credit score and budget.

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204

Email -

Email - Call/Text -

Call/Text -