I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Kentucky First-Time Homebuyer Quiz | FHA • VA • USDA • KHC DPA | Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA/title>

<meta name="description" content="Interactive Kentucky First-Time Homebuyer Quiz — test your knowledge on credit scores, $0-down USDA & VA loans, KHC assistance, AUS findings, DTI ratios, and pre-approval steps. Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA, NMLS 57916, EVO Mortgage (NMLS 1738461)." />

<meta name="keywords" content="Kentucky first time home buyer, FHA Kentucky, VA mortgage Kentucky, USDA Rural Housing Kentucky, KHC down payment assistance, DPA Kentucky, Kentucky mortgage pre approval, FHA 580 credit score Kentucky, USDA GUS, Fannie Mae DU" />

<meta name="author" content="Joel Lobb" />

<meta name="robots" content="index,follow" />

<link rel="canonical" href="https://www.mylouisvillekentuckymortgage.com/2025/09/kentucky-firsttime-homebuyer-questions.html" />

<!-- Social -->

<meta property="og:type" content="website" />

<meta property="og:title" content="Kentucky First-Time Homebuyer Quiz | FHA • VA • USDA • KHC DPA" />

<meta property="og:description" content="Test your Kentucky homebuyer knowledge and get personalized next steps from Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA." />

<meta property="og:url" content="https://www.mylouisvillekentuckymortgage.com/2025/09/kentucky-firsttime-homebuyer-questions.html" />

<meta property="og:image" content="https://www.mylouisvillekentuckymortgage.com/images/kentucky-first-time-homebuyer-quiz.jpg" />

<meta name="twitter:card" content="summary_large_image" />

<style>

body{font-family:'Inter',system-ui,sans-serif;margin:0;background:linear-gradient(135deg,#fef2f2 0%,#fee2e2 50%,#fecaca 100%);color:#1f2937;line-height:1.7}

.wrap{max-width:1200px;margin:0 auto;padding:40px 20px}

header.hero{background:#fff;border:2px solid #fecaca;border-radius:20px;padding:40px;box-shadow:0 25px 50px -12px rgba(0,0,0,.15)}

.pill{display:inline-block;padding:10px 20px;background:linear-gradient(135deg,#dc2626,#b91c1c);color:#fff;font-weight:700;border-radius:50px;margin-bottom:16px;font-size:14px;letter-spacing:.5px}

h1{font-size:34px;font-weight:800;margin-top:0}

.sub{color:#4b5563;font-size:17px;margin-bottom:20px}

.cta a,.cta button{display:inline-block;padding:12px 24px;border-radius:50px;border:none;text-decoration:none;text-transform:uppercase;font-weight:600;background:linear-gradient(135deg,#dc2626,#b91c1c);color:white;box-shadow:0 4px 10px rgba(220,38,38,.2);margin-right:10px;transition:all .3s ease}

.cta a:hover,.cta button:hover{transform:translateY(-2px)}

.card{background:#fff;border:2px solid #fecaca;border-radius:16px;padding:24px;margin-top:24px;box-shadow:0 5px 15px rgba(0,0,0,.05)}

.q-title{font-size:22px;font-weight:700;margin-bottom:12px}

.opt{display:block;margin-bottom:10px;padding:10px 14px;border:1px solid #e5e7eb;border-radius:12px;background:#fafafa;cursor:pointer;transition:all .3s ease}

.opt:hover{background:#fef2f2}

.opt.correct{border-color:#059669;background:#d1fae5}

.opt.incorrect{border-color:#dc2626;background:#fee2e2}

.explain{background:#fef2f2;border-left:4px solid #dc2626;padding:12px 16px;border-radius:8px;margin-top:10px;font-size:15px}

.controls{display:flex;justify-content:space-between;margin-top:20px}

footer{border-top:2px solid #fecaca;padding-top:30px;margin-top:60px;color:#6b7280;font-size:14px}

details summary{font-weight:700;color:#b91c1c;cursor:pointer;margin-top:12px}

details p{margin-left:10px}

</style>

</head>

<body>

<div class="wrap">

<header class="hero">

<div class="pill">Kentucky First-Time Homebuyer • FHA • VA • USDA • KHC</div>

<h1>Kentucky First-Time Homebuyer Interactive Quiz</h1>

<p class="sub">Learn credit requirements, down-payment assistance, rate-locks, closing costs and approval timelines in Kentucky. Take this quiz and see how ready you are to buy a home in 2025.</p>

<div class="cta">

<a href="#quiz">Start Quiz</a>

<a href="#faq">View FAQs</a>

</div>

<p><strong>Joel Lobb</strong> • NMLS 57916 | EVO Mortgage NMLS 1738461 | Equal Housing Lender</p>

</header>

<!-- QUIZ -->

<section id="quiz" class="card">

<h2 class="q-title" id="qText"></h2>

<form id="answers"></form>

<div id="explain" class="explain" style="display:none;"></div>

<div class="controls">

<button type="button" id="prevBtn">Previous</button>

<button type="button" id="checkBtn">Check Answer</button>

<button type="button" id="nextBtn" style="display:none;">Next</button>

</div>

<p id="progressHint" style="font-size:14px;color:#6b7280;margin-top:10px">Your progress is saved automatically.</p>

</section>

<section id="result" class="card" style="display:none;text-align:center">

<h2>Your Results</h2>

<p id="scoreText" style="font-size:40px;font-weight:900;color:#dc2626">0/0</p>

<p id="recommendation"></p>

<div class="cta">

<button type="button" id="retakeBtn">Retake Quiz</button>

<a href="#faq">Review FAQs</a>

</div>

</section>

<!-- FAQ -->

<section id="faq" class="card">

<h2>Kentucky First-Time Homebuyer FAQs</h2>

<details open><summary>What credit score is needed to qualify?</summary>

<p>Most lenders want a 620–640 middle score for zero-down programs (USDA or KHC). FHA allows 580 with 3.5 % down. VA often requires 620 +, but rapid rescore can help.</p>

</details>

<details><summary>Does it cost to get pre-approved?</summary>

<p>Pre-approvals are usually free, though a credit report fee of around $50 may apply.</p>

</details>

<details><summary>How long does a pre-approval take?</summary>

<p>With documents ready, AUS findings (Desktop Underwriter or GUS) often return within 24 hours.</p>

</details>

<details><summary>Which programs offer no money down?</summary>

<p>USDA and VA offer true zero-down options. KHC assistance and city grants can also cover down payment for FHA or Conventional loans.</p>

</details>

<details><summary>When can I lock my interest rate?</summary>

<p>After you have a signed contract on a property. Most lenders allow a 60–90 day lock with extensions available.</p>

</details>

<details><summary>How much do I need for closing costs?</summary>

<p>Plan for earnest money (~$500), appraisal ($500–650), optional inspection ($300–400), and termite report ($50 for VA). Seller/lender credits can offset these costs.</p>

</details>

</section>

<footer>

<p>JJoel Lobb, Mortgage Broker FHA, VA, KHC, USDA |</p>

<p>Email: <a href="mailto:kentuckyloan@gmail.com">kentuckyloan@gmail.com</a> | Text/Call: <a href="tel:+15029053708">502-905-3708</a></p>

<p>Not endorsed by or affiliated with FHA, VA, USDA, or any government agency. Information subject to change.</p>

</footer>

</div>

<!-- QUIZ SCRIPT -->

<script>

const QUESTIONS=[{q:"For zero-down paths in Kentucky, what credit score do many lenders look for on USDA or KHC with DPA?",options:["580-600","620-640","700 +","No minimum"],correct:1,explain:"Lenders often require a 620–640 middle score for zero-down programs in Kentucky."},{q:"What does it typically cost to get pre-approved for a mortgage in Kentucky?",options:["Always $200 +","Free – maybe $50 for credit report","$500 application fee","$300 processing fee"],correct:1,explain:"Pre-approvals are free except for a small credit report fee around $50."},{q:"How quickly can AUS findings return with docs ready?",options:["3-5 days","24 hours","1 week","2 weeks"],correct:1,explain:"Automated Underwriting System results usually within 24 hours when docs are ready."},{q:"Which programs offer true $0-down financing?",options:["FHA and HomeReady","USDA and VA","Conventional 97 %","Private only"],correct:1,explain:"USDA and VA are true zero-down programs for qualified Kentucky buyers."},{q:"What do you need to lock your interest rate?",options:["Pre-approval letter","Property address","Pay stub","Appraisal"],correct:1,explain:"A property address is required to lock a rate on a loan."},{q:"How long is a pre-approval valid?",options:["60 days","90 days","120 days","180 days"],correct:2,explain:"Pre-approvals are valid around 120 days before update needed."}];

const qText=document.getElementById("qText");

const answersEl=document.getElementById("answers");

const explain=document.getElementById("explain");

const prevBtn=document.getElementById("prevBtn");

const checkBtn=document.getElementById("checkBtn");

const nextBtn=document.getElementById("nextBtn");

const resultSec=document.getElementById("result");

const scoreText=document.getElementById("scoreText");

const recommendation=document.getElementById("recommendation");

const retakeBtn=document.getElementById("retakeBtn");

let state={i:0,answers:Array(QUESTIONS.length).fill(null)};

function render(){const q=QUESTIONS[state.i];qText.textContent=q.q;answersEl.innerHTML="";q.options.forEach((opt,idx)=>{const lbl=document.createElement("label");lbl.className="opt";lbl.innerHTML=`<input type='radio' name='ans' value='${idx}'> ${opt}`;answersEl.appendChild(lbl)});explain.style.display="none";nextBtn.style.display="none";checkBtn.style.display="inline-block";prevBtn.disabled=state.i===0;}

function currentChoice(){const c=answersEl.querySelector("input[name='ans']:checked");return c?Number(c.value):null;}

checkBtn.onclick=()=>{const choice=currentChoice();if(choice===null){alert("Please select an answer.");return;}const q=QUESTIONS[state.i];const opts=answersEl.querySelectorAll(".opt");opts.forEach((o,idx)=>{o.classList.remove("correct","incorrect");if(idx===q.correct)o.classList.add("correct");if(choice!==q.correct&&idx===choice)o.classList.add("incorrect");});explain.style.display="block";explain.textContent=q.explain;nextBtn.style.display="inline-block";checkBtn.style.display="none";};

nextBtn.onclick=()=>{if(state.i<QUESTIONS.length-1){state.i++;render();}else{finish();}};

prevBtn.onclick=()=>{if(state.i>0){state.i--;render();}};

function finish(){const correct=state.answers.reduce((a,v,i)=>a+(v===QUESTIONS[i].correct?1:0),0);document.getElementById("quiz").style.display="none";resultSec.style.display="block";scoreText.textContent=`${correct}/${QUESTIONS.length}`;const pct=Math.round(correct/QUESTIONS.length*100);if(pct>=80){recommendation.textContent="Excellent — you understand Kentucky mortgage basics! You're ready to get pre-approved.";}else if(pct>=60){recommendation.textContent="Good foundation! Let's fine-tune your knowledge and get you home-ready.";}else{recommendation.textContent="No worries — we can walk you through the process step by step.";}}

retakeBtn.onclick=()=>{state={i:0,answers:Array(QUESTIONS.length).fill(null)};document.getElementById("quiz").style.display="block";resultSec.style.display="none";render();};

render();

</script>

<!-- STRUCTURED DATA -->

<script type="application/ld+json">

{

"@context":"https://schema.org",

"@graph":[

{

"@type":"WebPage",

"name":"Kentucky First-Time Homebuyer Quiz",

"url":"https://www.mylouisvillekentuckymortgage.com/2025/09/kentucky-firsttime-homebuyer-questions.html",

"description":"Interactive quiz and FAQ guide for Kentucky first-time buyers on FHA, VA, USDA, and KHC mortgage programs.",

"inLanguage":"en-US",

"author":{"@type":"Person","name":"Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA","jobTitle":"Mortgage Loan Officer","email":"kentuckyloan@gmail.com","telephone":"+1-502-905-3708","identifier":"NMLS 57916","worksFor":{"@type":"Organization","name":"Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA","identifier":"NMLS 1738461"}},

"publisher":{"@type":"Organization","name":"Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA"}

},

{

"@type":"LocalBusiness",

"name":"Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA",

"image":"https://www.mylouisvillekentuckymortgage.com/images/joel-lobb-evo-mortgage.jpg",

"telephone":"+1-502-905-3708",

"email":"kentuckyloan@gmail.com",

"url":"https://www.mylouisvillekentuckymortgage.com/",

"address":{"@type":"PostalAddress","streetAddress":"Louisville, KY","addressLocality":"Louisville","addressRegion":"KY","postalCode":"40299","addressCountry":"US"},

"openingHours":"Mo-Sa 09:00-20:00",

"priceRange":"$$",

"sameAs":["https://www.facebook.com/joellobbnmls57916","https://www.linkedin.com/in/joellobb/","https://www.youtube.com/@joellobbmortgage"]

},

{

"@type":"FAQPage",

"mainEntity":[

{"@type":"Question","name":"What credit score do I need for Kentucky first-time buyer loans?","acceptedAnswer":{"@type":"Answer","text":"Most lenders require 620 for zero-down USDA or KHC loans government backed loans. FHA allows 580 with 3.5% down, though lenders may require higher scores."}},

{"@type":"Question","name":"Does it cost anything to get pre-approved?","acceptedAnswer":{"@type":"Answer","text":"Pre-approvals are typically free, but some lenders charge a small credit report fee under $100 give or take."}},

{"@type":"Question","name":"How long does it take to get pre-approved?","acceptedAnswer":{"@type":"Answer","text":"Automated systems like DU or GUS can return approvals in about 24 hours if documents are complete."}},

{"@type":"Question","name":"Which programs help with down payment?","acceptedAnswer":{"@type":"Answer","text":"USDA and VA offer true zero-down financing, while KHC, FHA, and city grants provide down payment help."}},

{"@type":"Question","name":"When can I lock my interest rate?","acceptedAnswer":{"@type":"Answer","text":"You can lock your rate once you have a signed purchase contract. Most lenders offer 15,30,60, 45 and day locks for free."}},

{"@type":"Question","name":"How much will I need for closing costs?","acceptedAnswer":{"@type":"Answer","text":"Budget for appraisal ($500–650), inspection ($300–400), termite report ($50 for VA), and earnest money (~$500 typically). Seller or lender credits can offset costs."}}

]

}

]

}

</script>

</body>

</html>

<div style='clear: both;'></div>

</div>

<div class='post-footer'>

<div class='post-footer-line post-footer-line-1'>

<span class='post-author vcard'>

</span>

<span class='post-timestamp'>

</span>

<span class='post-comment-link'>

</span>

<span class='post-icons'>

<span class='item-action'>

<a href='https://www.blogger.com/email-post/2083715272801756161/7754210932663606369' title='Email Post'>

<img alt='' class='icon-action' height='13' src='https://resources.blogblog.com/img/icon18_email.gif' width='18'/>

</a>

</span>

</span>

<div class='post-share-buttons goog-inline-block'>

<a class='goog-inline-block share-button sb-email' href='https://www.blogger.com/share-post.g?blogID=2083715272801756161&postID=7754210932663606369&target=email' target='_blank' title='Email This'><span class='share-button-link-text'>Email This</span></a><a class='goog-inline-block share-button sb-blog' href='https://www.blogger.com/share-post.g?blogID=2083715272801756161&postID=7754210932663606369&target=blog' onclick='window.open(this.href, "_blank", "height=270,width=475"); return false;' target='_blank' title='BlogThis!'><span class='share-button-link-text'>BlogThis!</span></a><a class='goog-inline-block share-button sb-twitter' href='https://www.blogger.com/share-post.g?blogID=2083715272801756161&postID=7754210932663606369&target=twitter' target='_blank' title='Share to X'><span class='share-button-link-text'>Share to X</span></a><a class='goog-inline-block share-button sb-facebook' href='https://www.blogger.com/share-post.g?blogID=2083715272801756161&postID=7754210932663606369&target=facebook' onclick='window.open(this.href, "_blank", "height=430,width=640"); return false;' target='_blank' title='Share to Facebook'><span class='share-button-link-text'>Share to Facebook</span></a><a class='goog-inline-block share-button sb-pinterest' href='https://www.blogger.com/share-post.g?blogID=2083715272801756161&postID=7754210932663606369&target=pinterest' target='_blank' title='Share to Pinterest'><span class='share-button-link-text'>Share to Pinterest</span></a>

</div>

</div>

<div class='post-footer-line post-footer-line-2'>

<span class='post-labels'>

Labels:

<a href='https://www.mylouisvillekentuckymortgage.com/search/label/faq' rel='tag'>faq</a>,

<a href='https://www.mylouisvillekentuckymortgage.com/search/label/Kentucky%20Mortgage%20Refinance%20Questions%20to%20ask' rel='tag'>Kentucky Mortgage Refinance Questions to ask</a>,

<a href='https://www.mylouisvillekentuckymortgage.com/search/label/Most%20frequently%20asked%20Kentucky%20Mortgage%20and%20Home%20buying%20questions' rel='tag'>Most frequently asked Kentucky Mortgage and Home buying questions</a>,

<a href='https://www.mylouisvillekentuckymortgage.com/search/label/VA%20Mortgage%20Loan%20FAQ' rel='tag'>VA Mortgage Loan FAQ</a>

</span>

</div>

<div class='post-footer-line post-footer-line-3'>

<span class='post-location'>

</span>

</div>

<div class='author-profile' itemprop='author' itemscope='itemscope' itemtype='http://schema.org/Person'>

<img itemprop='image' src='//blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEi_KANOsvWnE_Ahhu8GrkPMTBkgtD_vuwLoePRBNtw7kMJQcjharuqey8eVnxw95waBWnKchYT_6X46Rnvka8S0m2dLbe84FVJCCdEqjPeEdnYTaXxVcqWx72h3GSkmqw/s113/yz0telhnami60j51263n_400x400.jpeg' width='50px'/>

<div>

<a class='g-profile' href='https://www.blogger.com/profile/14742291613632757087' itemprop='url' rel='author' title='author profile'>

<span itemprop='name'>Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA</span>

</a>

</div>

<span itemprop='description'>Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.</span>

</div>

</div>

</div>

</div>

</div></div>

<div class="date-outer">

<div class="date-posts">

<div class='post-outer'>

<div class='post hentry uncustomized-post-template' itemprop='blogPost' itemscope='itemscope' itemtype='http://schema.org/BlogPosting'>

<meta content='2083715272801756161' itemprop='blogId'/>

<meta content='8468023301645146107' itemprop='postId'/>

<a name='8468023301645146107'></a>

<h3 class='post-title entry-title' itemprop='name'>

<a href='https://www.mylouisvillekentuckymortgage.com/2025/11/kentucky-mortgage-loan-approval.html'>Kentucky Mortgage Loan Approval Checklist | Documents Needed for FHA, VA & USDA Loans</a>

</h3>

<div class='post-header'>

<div class='post-header-line-1'></div>

</div>

<div class='post-body entry-content' id='post-body-8468023301645146107' itemprop='articleBody'>

<!--DOCTYPE html-->

<html lang="en">

<head>

<meta charset="UTF-8" />

<meta name="viewport" content="width=device-width, initial-scale=1.0" />

<title>Kentucky Mortgage Loan Approval Checklist 2025 | Documents Needed for FHA, VA & USDA Loans

🏡 How to Get Approved for a Kentucky Mortgage Loan (2025 Guide)

Author: Joel Lobb, Mortgage Loan Officer NMLS 57916 | EVO Mortgage NMLS 1738461 Serving: Louisville • Lexington • Bowling Green • Owensboro • Northern Kentucky Equal Housing Lender

✅ Step-by-Step: Getting Approved for a Mortgage in Kentucky

Getting approved for a Kentucky mortgage loan starts with one thing — having your paperwork ready.

Lenders use four key factors to determine your approval:

Income & Employment Stability

Assets & Down Payment Verification

Credit History & Score

Appraisal / Collateral Review

This guide is designed for FHA, VA, USDA, KHC, and Conventional loans and helps Kentucky homebuyers and refinancers prepare efficiently.

📋 Documents Required for All Kentucky Mortgage Applicants

W-2 forms for the past 2 years

Recent pay stubs covering 30 days of income

Bank statements for checking/savings accounts (all pages, last 60–90 days)

Asset statements for 401(k), IRA, or investment accounts

Driver’s license and Social Security card

Two-year residence history (landlord or mortgage company contact info)

Purchase contract (if under contract)

Earnest-money check copy or proof of cleared funds

Employment history covering 24 months, including any gaps

Funds for credit report & appraisal fees

Proof of funds used for down payment and closing costs

Pro Tip: Keep every page — even the blank ones. Kentucky lenders must review complete statements for compliance.

🧾 If You’re Self-Employed or a 1099 Contractor

Personal federal tax returns (all pages and schedules) — last 2 years

Business returns for any entity where you own ≥ 25%

Year-to-date profit & loss statement and balance sheet

1099 forms if applicable

🎖️ FHA, VA & USDA Loan-Specific Requirements in Kentucky

FHA Loans

Copy of driver’s license + Social Security card

Minimum 580 credit score for 3.5% down (10% down below 580)

2-year job history + consistent income documentation

VA Loans

Certificate of Eligibility (COE)

DD-214 (discharge paperwork)

Nearest living relative information (required by VA)

No down payment + no monthly PMI if qualified

USDA Rural Housing Loans

Property must be eligible by county (use USDA map)

Household income limits apply — varies by county and household size

Zero down payment available if approved under USDA guidelines

💡 Common Mistakes That Delay Kentucky Loan Approvals

Missing bank pages or statements

Large unverified deposits without documentation

Credit disputes or recent late payments

Job changes without updated VOE (Verification of Employment)

Unfiled tax returns or IRS payment plans not verified

🧠 Work With a Local Kentucky Mortgage Expert

Most loan delays come from incomplete files. Working with a local lender who understands Kentucky underwriting standards — FHA, VA, USDA, and KHC — can save weeks.

VA Loans for qualified veterans and surviving spouses

FHA Loans for credit scores 580+

Conventional Loans with as little as 3% down

🎥 Watch: How to Get Approved for a Kentucky Mortgage Loan

Watch this short 10-minute walkthrough where Joel Lobb breaks down how Kentucky homebuyers can get pre-approved faster, what lenders look for, and how to avoid common mistakes.

" title="How to Get Approved for a Kentucky Mortgage Loan" allowfullscreen loading="lazy">

🎬 Subscribe to Joel Lobb on YouTube for Kentucky mortgage tips, FHA/VA/USDA updates, and credit-improvement strategies.

👉 Subscribe Now

❓Frequently Asked Questions (FAQ)

What’s the minimum credit score to get approved for a Kentucky mortgage?

FHA = 580 (3.5% down); VA & USDA typically 620+; Conventional 620+; KHC may allow lower with compensating factors.

Can I get approved if I’m self-employed?

Yes, with two years of filed returns showing consistent income and proof of business stability.

How long does approval take?

Pre-approval within 24 hours once documents are received; full loan approval in about 30 days depending on property type and program.

What’s the fastest way to get approved?

Submit all documents at once, avoid new credit inquiries, and respond quickly to lender requests.

Kentucky Closing Costs Explained | No Jargon Guide for Homebuyers 2025

Kentucky Closing Costs Explained

No jargon – just real numbers. Watch Joel Lobb break down everything you need to know about closing costs in Kentucky and how to save thousands before you close.

Summary: Closing costs in Kentucky typically range 2 – 5 % of the loan amount. FHA, VA, USDA and Conventional loans all handle these costs differently. 2025 KHC programs may cover part or all of them for qualified buyers.

Buying a home in Kentucky comes with one final step before you get your keys — closing costs. These are the fees and services required to finalize your mortgage, covering everything from the appraisal to title insurance. Whether you're purchasing with an FHA loan, VA loan, USDA Rural Housing loan, KHC program, or a Conventional mortgage, understanding these costs will help you budget and avoid surprises at the closing table.

Quick Answer: Kentucky homebuyers can expect closing costs ranging from 1% to 3% of the loan amount. For a $300,000 home, that means $3000–$9000 depending on loan type and lender.

💰 What Are Mortgage Closing Costs?

Mortgage closing costs are the final fees and charges due at settlement for a home purchase or refinance. These costs cover third-party services like appraisals, title searches, insurance, inspections, and lender processing fees. Unlike your down payment, closing costs are separate — and they can add up quickly.

In Kentucky, the total amount varies based on several factors:

Loan type (FHA, VA, USDA, Conventional, KHC)

Home price and location

Down payment percentage

Credit score and loan approval timeline

County and local recording fees

Lender and service provider choices

📋 Common Closing Costs in Kentucky (2025)

Here's a breakdown of typical closing costs you'll encounter as a Kentucky homebuyer:

Fee Type

Typical Cost Range

Who Pays?

Appraisal Fee

$500–$800

Borrower (upfront)

Home Inspection

$300–$700

Borrower (optional but recommended)

Credit Report Fee

$50–$150

Borrower

Loan Origination Fee

0.5–3% of loan

Borrower

Title Search & Insurance

0.5–1% of home price

Borrower (varies by county)

Recording Fees

$40–$200

Borrower

Prepaid Taxes & Insurance

6-12 months escrow

Borrower

FHA/VA/USDA Funding Fees

0%–3.6% of loan

Borrower (can be financed)

Homeowners Insurance (1st year)

$800–$3000

Borrower

HOA Fees (if applicable)

$100–$500

Borrower

🏡 Who Pays Closing Costs in Kentucky?

While most closing costs are paid by the buyer, there are several ways to reduce your out-of-pocket expenses. Here's how it works:

Buyer Pays (Standard)

As the borrower, you're responsible for most closing costs. However, you have options to reduce the burden.

Seller Concessions

The seller can contribute to your closing costs through what's called a "seller concession" or "seller credit." The maximum amount varies by loan type:

FHA Loans: Up to 6% of the home purchase price

VA Loans: Up to 4% of the home purchase price

USDA Loans: Up to 6% of the home purchase price

Conventional Loans: 3–9% depending on down payment (typically 3% with 25% down, up to 9% with 3% down)

KHC Programs: Often allows up to 3-6% seller contribution

💡 Pro Tip: If you're pre-approved for a home, ask your real estate agent to negotiate seller concessions during the offer phase. Sellers are often willing to contribute if it means a smoother sale!

Lender Credits

Another way to reduce closing costs is through a lender credit. This works like this: you accept a slightly higher interest rate in exchange for the lender paying some or all of your closing costs. This is particularly helpful if you don't have enough cash at closing but plan to stay in the home for many years.

Financing Costs Into the Loan

With FHA, VA, and USDA loans, you can roll certain upfront fees (like FHA mortgage insurance or VA funding fees) directly into your loan amount. This reduces the cash you need at closing, though it does increase your monthly payment slightly.

🔍 Understanding Your Loan Estimate & Closing Disclosure

The federal government requires lenders to provide clear, standardized disclosures about your loan costs. Here's what you need to know:

Loan Estimate (Due Within 3 Business Days)

After you submit your mortgage application, your lender must provide a Loan Estimate within three business days. This document outlines:

Loan terms and interest rate

Monthly principal and interest payment

Estimated closing costs (broken down by fee)

Comparison of different loan options

Review this carefully and compare it with estimates from other lenders. Under RESPA (Real Estate Settlement Procedures Act), many of your closing costs cannot increase by more than 10% from the Loan Estimate to your final closing.

Closing Disclosure (Due 3 Days Before Closing)

Before your closing appointment, you'll receive a Closing Disclosure listing your final costs. This is your chance to verify that everything matches your Loan Estimate. You have the right to review this document for at least three business days before signing.

⚠️ Important: Don't skip reviewing the Closing Disclosure. Errors happen. If you spot a discrepancy between your Loan Estimate and Closing Disclosure, contact your lender immediately to resolve it before closing day.

🎯 Kentucky Closing Costs by Loan Type

FHA Loans (First-Time Homebuyers)

FHA loans are popular with Kentucky first-time homebuyers because they allow lower down payments (3.5%) and more flexible credit requirements. However, FHA comes with upfront and annual mortgage insurance premiums:

Upfront FHA Mortgage Insurance: 1.75% of loan amount (can be financed)

Annual Mortgage Insurance: 0.45–0.80% annually (added to monthly payment)

Total FHA Closing Costs: 1–7% of loan amount

VA Loans (Veterans & Active Duty)

VA loans offer excellent benefits for military members and veterans, with no down payment required and no mortgage insurance. Instead, there's a VA funding fee:

VA Funding Fee: 2.3% of loan (first-time use, no down payment) — can vary based on service and down payment

Total VA Closing Costs: 1-4% of loan amount

USDA Rural Housing Loans (Rural Kentucky)

USDA loans are designed for rural Kentucky properties with zero down payment required:

USDA Guarantee Fee: 1% of loan (upfront, can be financed)

Annual Mortgage Insurance: 0.35% annually

Total USDA Closing Costs: 1–6% of loan amount

Conventional Loans

Conventional loans don't have government insurance fees, making them attractive once you have a higher down payment and good credit:

Total Conventional Closing Costs: 1–5% of loan amount

Kentucky Housing Corporation (KHC) Loans

KHC programs offer first-time homebuyers down payment and closing cost assistance:

Down Payment Assistance: Up to $12,500

Closing Cost Assistance: Often available

Interest Rate: Competitive rates

Total KHC Closing Costs: Can be significantly reduced with assistance programs

💡 How to Reduce Closing Costs in Kentucky

Here are proven strategies to minimize your closing costs:

1. Compare Multiple Lenders

Don't just accept the first offer. Get Loan Estimates from at least 3 lenders. Even small differences in origination fees and closing costs can save you hundreds or thousands of dollars. Under federal law, many costs have a 10% limit on increases from estimate to final, so comparing early pays off.

2. Negotiate Seller Concessions

In today's market, sellers are often motivated to negotiate. Work with your real estate agent to request seller concessions to cover your closing costs. Remember the limits for each loan type (FHA: 6%, VA: 4%, USDA: 6%, Conventional: varies).

KHC closing cost assistance programs can cover $0 to 100% of your closing costs depending on your income, credit, and the specific program. As a Kentucky first-time homebuyer, you may qualify for up to $12,500 in down payment assistance plus closing cost help.

4. Ask About Lender Credits

Some lenders will absorb closing costs in exchange for a slightly higher interest rate. Calculate whether this makes sense long-term. If you plan to stay in the home for 5+ years, a lower rate usually outweighs the higher closing costs.

5. Roll Fees Into the Loan

With FHA, VA, and USDA loans, you can finance certain upfront fees (funding fees, mortgage insurance). This reduces cash needed at closing but increases your loan amount and monthly payment.

6. Shop for Services

Your lender cannot force you to use specific appraisers, inspectors, or title companies. Get competitive quotes and choose the best value.

7. Close Before Month-End

Closing late in the month can reduce your prepaid taxes and insurance (escrow), which lowers immediate out-of-pocket costs.

📊 Closing Costs Breakdown Example

Scenario: $300,000 home purchase with FHA loan, 3.5% down payment ($10,500), $289,500 loan amount, 6.5% interest rate

Item

Cost

Appraisal

$650

Credit Report

$40

Loan Origination (0.75%)

$2,171

Title Search & Insurance

$1,200

Recording & Transfer Fees

$120

Upfront FHA Mortgage Insurance (1.75%)

$5,067

Homeowners Insurance (1 year)

$1,200

Property Taxes (prepaid, 2 months)

$1,500

TOTAL CLOSING COSTS

$11,948

With seller concessions up to 6% ($18,000), the seller could help pay a significant portion of these costs.

Ready to Get Started?

Get a personalized closing cost estimate and explore loan options that fit your budget.

Contact Joel Lobb, Kentucky Mortgage Broker

Specializing in FHA, VA, USDA & KHC Loans for Kentucky Homebuyers

Yes. You can negotiate with sellers through your real estate agent, ask lenders for credits or better terms, and shop around for services like appraisals and title insurance. Every dollar saved adds up.

Can I pay closing costs from my down payment savings?

No. Down payment and closing costs are separate. However, sellers can help via concessions, and lenders can offer credits. Additionally, FHA, VA, and USDA programs allow financing certain fees into the loan.

Are there any Kentucky-specific closing cost fees?

Kentucky counties have varying recording and transfer fees. Jefferson County (Louisville) fees differ from rural counties. Your lender will break these down in your Loan Estimate.

Can closing costs be rolled into my mortgage?

Yes, depending on your loan type. FHA, VA, and USDA loans allow you to finance upfront mortgage insurance and funding fees. Conventional loans typically don't allow this, but lender credits can help reduce upfront costs.

What if closing costs exceed my Loan Estimate?

Under RESPA, many closing costs cannot increase by more than 10% from your Loan Estimate to your Closing Disclosure. If you see major discrepancies, contact your lender immediately.

Does Kentucky have first-time homebuyer assistance?

Yes! The Kentucky Housing Corporation (KHC) offers closing cost assistance, down payment programs, and favorable rates for first-time buyers. You may qualify for $0 to $30,000+ depending on the program.

How to Buy a HUD Home in Kentucky for Just $100 Down: Complete 2025 Guide

How to Buy a HUD Home in Kentucky for Just $100 Down: Complete 2025 Guide

Buying a home in Kentucky just became more affordable than ever. With the FHA $100 Down Payment Program, eligible buyers can purchase HUD-owned homes with only $100 down — a fraction of the standard 3.5% FHA down payment. This guide walks you through everything you need to know to make it happen in 2025.

What Are HUD Homes and Why Are They So Affordable?

HUD homes are properties previously financed through FHA loans that have gone through foreclosure. The U.S. Department of Housing and Urban Development (HUD) takes ownership of these homes and sells them to the public through registered agents and contractors.

These homes are often priced below market value to encourage homeownership and stabilize neighborhoods. Kentucky has a wide selection of HUD homes across the state — from Louisville and Lexington to Bowling Green and Elizabethtown.

Understanding the FHA $100 Down Payment Program

This special program allows Kentucky buyers to purchase eligible HUD-owned homes with just $100 down when using FHA financing. It’s designed to reduce barriers for homeownership and help families build equity faster.

Minimum 580 credit score (500–579 may qualify with 10% down)

To qualify for the $100 down payment incentive, buyers must:

Be owner-occupants (must live in the home as their primary residence).

Submit offers during the exclusive owner-occupant period (typically first 30 days of listing).

Meet FHA credit, income, and debt-to-income ratio standards.

Work with a HUD-registered real estate agent and FHA-approved lender.

The 5-Step Process to Buy a HUD Home in Kentucky

Search for Homes: Visit HUDHomeStore.com, select Kentucky, and filter for “$100 Down Eligible.”

Get Pre-Approved: Apply with an FHA-approved lender to receive your pre-approval letter.

Submit an Offer: Your HUD agent submits your bid online with your pre-approval attached.

HUD Review: HUD reviews bids and prioritizes owner-occupant buyers.

Close & Move In: Bring your $100 down payment, finalize closing, and get your keys.

Closing Costs and Seller Concessions

Typical closing costs range between 2%–5% of the home price. HUD may pay up to 3% of your closing costs. You can also roll some costs into your mortgage depending on FHA eligibility and lender approval.

Condition of HUD Homes

HUD homes are sold “as-is.” Always order a professional home inspection before closing. FHA appraisers will confirm the property meets minimum safety and structural requirements before loan approval.

Why This Program Works So Well in Kentucky

Kentucky’s moderate home prices, stable economy, and low property taxes make the FHA $100 Down Program ideal for first-time buyers and families wanting to stop renting and start building wealth. Many buyers pair it with Kentucky Housing Corporation (KHC) down payment assistance for added support.

FHA Gift Funds Kentucky 2025 | Gifts of Equity & Down Payment Guide

FHA Gift Funds Kentucky 2025: Complete Guide to Gifts of Equity & Down Payment Assistance

Last Updated: October 2025 — FHA loans remain one of the most accessible pathways to homeownership for Kentucky first-time buyers. If you've been told you can't afford a home because of down payment requirements, think again. Understanding how FHA gift funds and gifts of equity work could open the door to your dream home with as little as 3.5% down.

Kentucky first-time homebuyers with FHA gift funds make homeownership more affordable

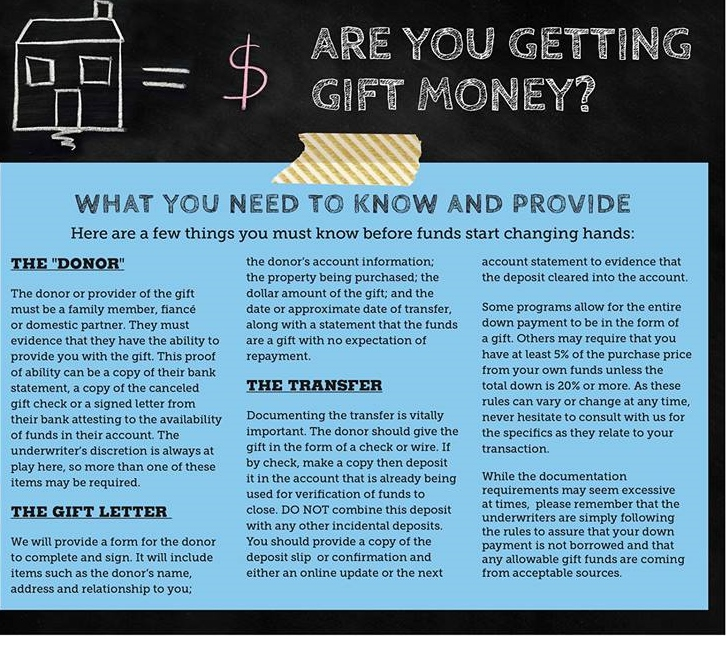

Many Kentucky homebuyers don't realize they can receive financial help from family, friends, or even employers to cover their down payment and closing costs. This guide explains exactly how FHA gift funds work, who can provide them, and what documentation you'll need to get approved.

Who Can Give FHA Gift Funds in Kentucky?

The HUD 4000.1 Handbook outlines several acceptable sources for FHA gift funds. The key requirement: the funds must be a gift, not a loan.

FHA gift funds can come from family members, employers, charities, and government programs

Eligible donors include:

Family members — parents, grandparents, siblings, children, spouse, or in-laws

Employers or labor unions — who offer down payment assistance programs

Close friends — with documented proof of relationship

Government or public agencies — like KHC (Kentucky Housing Corporation) programs

💡 Important: Sellers, builders, and real estate agents cannot provide gift funds. FHA lenders verify this to prevent fraud and ensure true down payment assistance.

FHA Definition of "Family Member"

For FHA purposes, family includes parents, grandparents, children (including adopted or foster children), siblings, spouses, domestic partners, uncles, aunts, and all in-laws (mother-, father-, sister-, or brother-in-law). This broad definition means most relatives can provide gift funds.

FHA Gift Fund Rules for Kentucky Borrowers: What You Need to Know

Requirement

FHA Rule

Property Type

Primary residence (1–4 family units)

Minimum Down Payment

No minimum required (can be 100% gift)

Maximum LTV (Loan-to-Value)

Up to 96.5% with 3.5% down

Gift Fund Use

Down payment, closing costs, pre-paid expenses

Reserves

Gift funds cannot count toward reserve requirements

Cash on Hand

Not acceptable (funds must be traceable)

Repayment

Strictly prohibited — must be a gift, not a loan

Documentation Required for FHA Gift Funds

The most critical part of using gift funds is documentation. Lenders need proof that:

The donor has the funds available

The funds came from a legitimate source

No repayment is expected

The money actually transferred to you

Required Documents Checklist

Signed gift letter — states the amount, relationship, and that no repayment is expected

Donor's recent bank statements — typically last 2 months showing the gift fund withdrawal

Your bank statements — showing the deposit of gift funds

Wire receipt or cashier's check proof — if funds go directly to closing

Written explanation — if any gaps appear between withdrawal and deposit

Pro Tip: Have the donor wire funds directly to your account or the title company, or use a cashier's check. This creates a clear paper trail. Lenders want to see documented proof that doesn't raise red flags.

Understanding FHA Gifts of Equity in Kentucky

A gift of equity is a unique FHA program that helps when a family member sells you their home. Instead of paying full market value, you purchase the home at a lower price, and the difference becomes your down payment credit.

Real-World Example: Gift of Equity in Kentucky

Scenario: Your parent owns a home appraised at $200,000. They agree to sell it to you for $180,000. The $20,000 difference is the "gift of equity." You can use this $20,000 as your down payment on an FHA loan. Your loan would be for $180,000 (or less with additional down payment), and the $20,000 equity gift covers the difference.

FHA Gift of Equity Requirements

Only family members can provide a gift of equity

Maximum LTV = 85% (loan amount ÷ appraised value) unless:

The seller's home is their primary residence, OR

You rented the property for at least six months before the sales contract date

Must be documented in the purchase agreement and appraisal

Documentation for Gift of Equity

Signed gift letter — from the seller acknowledging the equity gift

Current appraisal — showing the true market value

Sales contract — identifying the purchase price and equity gift amount

Proof of relationship — birth certificate, marriage license, or family documents

FHA Gift Letter Template for Kentucky Borrowers

Your FHA gift letter must include specific language. Here's a template you can use:

Sample FHA Gift Letter:

"I, [Donor Full Name], am giving [Borrower Full Name] a gift of $[Amount] for use toward the down payment on the property located at [Property Address]. This gift represents no obligation for repayment. I expect nothing in return for this gift. [Donor Signature] [Date]"

Make sure your lender approves the exact wording before having it signed.

Does Kentucky's KHC Program Accept Gift Funds?

Yes. Kentucky Housing Corporation (KHC) and other down payment assistance programs often work alongside FHA gift funds. Many Kentucky first-time homebuyers combine KHC grants with family gifts to minimize out-of-pocket costs.

Yes. You can receive gifts from multiple family members or organizations. Each gift requires its own gift letter and documentation.

Is there a limit to how much I can receive as a gift?

No. FHA has no maximum on gift amounts, but the full down payment and closing costs can be covered by gifts if properly documented.

Can a gift fund be used for closing costs?

Absolutely. FHA gift funds can cover down payment, closing costs, appraisal fees, inspection costs, and other homebuying expenses.

What if the donor and I live in different states?

That's fine. The donor's location doesn't matter — only that they have a legitimate relationship to you and the funds are properly documented.

Why Work With a Kentucky FHA Loan Expert?

Understanding FHA gift fund rules is complex, and mistakes can delay your approval or derail your loan entirely. Working with a knowledgeable Kentucky mortgage specialist ensures:

Proper documentation — all gifts are verified and approved upfront

No delays — we catch issues before they become problems

Maximum benefits — we identify all programs you qualify for (FHA, KHC, VA, USDA)

Peace of mind — you have expert guidance every step of the way

Ready to Buy Your Kentucky Home With FHA Gift Funds?

Let me help you navigate FHA gift fund requirements and get approved quickly. Whether you're receiving a family gift, a gift of equity, or KHC assistance, I'll ensure everything is documented correctly for a smooth, fast approval.

This is why it's possible to get a little help in the form of a down payment gift from a family member or relative, close friend, or even a charitable organization. And it’s actually becoming more popular, especially among millennials. In the National Association of REALTORS® 2020 Generational Trends Report, 13 percent of home buyers (and 27 percent for ages 22 to 29) indicated their source of down payment to be a gift from their relative or friend.

So if you’re lucky enough to find down payment fund as one of your gifts under the Christmas tree this year (or maybe you’re the one who wants to give it), it may not be as simple as opening your cash gift (or handing someone a wad of cash) and going straight to the lender to use it to buy a home.

Down payment gift funds, whether you’re giving or receiving it, are closely regulated by lenders and must meet certain requirements. Here are certain rules that the gift giver and recipient should know to avoid trouble down the road.

While we may automatically consider a family member, like parents or siblings, when thinking about who can give a mortgage down payment gift, there are other entities who could also be eligible gift sources. But because cash can come with strings attached, and lenders want to make sure that the gift money is nothing but a gift (which will be discussed later on), there are restrictions on who can give money (or who you can give money to) to help purchase a home.

For conventional loans

If you are getting a loan through Fannie Mae or Freddie Mac, gifts can only be from a family member or relative. This may be your spouse, child, siblings, parents, grandparents, or anyone related by blood, marriage, adoption, or legal guardianship. Soon-to-be family members such as your domestic partner, fiancé, or even future in-laws are also eligible to give funds for a down payment.

For FHA loans

The Federal Housing Administration (FHA) has its own set of rules when it comes to giving or receiving down payment gifts, although they offer a broader eligibility range. If you are getting an FHA loan, you can receive down payment funds from family members, friends who have a clearly defined and documented interest in your life, employers, labor unions, government agencies, and even charitable organizations.

For USDA and VA home loans

VA loans (backed by the U.S. Department of Veterans Affairs) and USDA mortgages (given by the U.S. Department of Agriculture)may have fewer restrictions, but the down payment gift funds cannot come from anyone who would benefit from the proceeds of the purchase, such as the seller, developer, builder, your real estate agent, and some other entity.

There are no limits on the amount of money someone can give you for a down payment or to cover closing costs. However, rules still apply depending on the type of loan and property you're purchasing. Some types of loans may need you to contribute a certain amount of the down. The key is to check with your lender for the latest regulations on how much you can really use.

Likewise, there can be tax implications on the person giving the gift funds. They may be liable if the amount exceeds the gift tax exclusion limit. As of 2020, for instance, any individual can give funds up to $15,000 without a tax penalty. On the other hand, parents who are married and are filing jointly can give up to $30,000 per child for a mortgage down payment (or any other purpose), without incurring the gift tax. For a down payment gift that exceeds the said amounts, the donor must file a gift tax return to disclose the gift.

You need to confirm the relationship between you and the giver and provide the right paperwork.

If you're fortunate enough to have a family member or any eligible entity who can give you funds towards your home’s down payment, you’ll need to confirm your relationship with the gift-giver and provide your mortgage underwriter more information about where the funds came from.

For lenders to confirm that the new money isn’t a loan, you’ll need these things:

1. A down payment gift letter - If your lender has a template letter for this purpose, you will need to send it to the funds’ donor. If there isn’t a template, you might want to ask what information should be included so you can draft your own.

The letter typically includes details about the gift-giver, such as the name, address, contact phone, relationship to the borrower, and address of the property to be purchased. The date when the gift was transferred and the amount of funds given to the borrower must also be indicated. The donor should also write a sentence explaining that the fund is a gift and that there isn’t any expectation of repayment. The letter must be signed by both the gift-giver and the borrower.

2. The gift-giver’s bank statements - This is to show they have the funds to give the buyer as much money as promised.

3. A bank slip from the buyer’s account - This is to indicate when the money was transferred, to verify that the cash is from a legitimate source and that the borrower has an appropriate relationship with the donor, and to confirm the information provided in the letter.

Remember: you can't pay back the gift.

Down payment gift funds need to be just like that—a gift and not a loan that is expected to be paid. You need to make it clear with your mortgage lender that the money you received was entirely gifted and not something that you need to pay back eventually, because by then it will be considered mortgage or loan fraud. Besides, it can also put your loan qualification at risk since your debt-to-income ratio will be factored when you get a mortgage.

Try to make it a “seasoned” gift money.

It might make more sense to try and make your gift money “seasoned”, especially if you know that someone is going to help you buy a home (often in the case of parents or other relatives). Lenders refer to it as seasoned money when it has been sitting in your bank account for some time, at least for two months. When the gifted money is given in advance, you often don't have to worry about writing gift letter documentation.

Bottom Line

Down payment gift funds make it easier for first-time home buyers to afford a home. If you anticipate accepting help, remember to consider the rules above so you can accept such a gift in a proper manner. Be upfront with your mortgage lender if you plan on using gift funds for the down payment. Don't forget to also talk to the individual or entities who are planning to give you money about the tax implications and other considerations.

Call/Text -

Call/Text -

FHA gift funds can come from family members, employers, charities, and government programs

FHA gift funds can come from family members, employers, charities, and government programs