I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Select a loan type above to view inspection requirements.

Kentucky Well, Septic, Water, and Termite Requirements for FHA, VA, USDA, and Conventional Loans

When you're buying a home in Kentucky with a well or septic system, the lending requirements can vary dramatically depending on whether you're using Conventional, FHA, USDA, or VA financing. As a result, borrowers and Realtors routinely get blindsided during underwriting – especially with water tests, well–septic distance rules, and VA termite requirements.

Below is a streamlined guide that tells you exactly what is required for each loan program so you can eliminate surprises, keep your file moving, and get to the closing table without delays.

Water Test Requirements

Conventional: Only required if the appraiser calls for it.

FHA: Coliform, nitrites, nitrates. Add lead test if within 1/4 mile of farmland.

USDA: Total coliform test required.

VA: Coliform, nitrites, nitrates. Add lead if within 1/4 mile of farmland.

Septic Inspection

All loan types: Not required unless the appraiser specifically requests it.

Well & Septic Distance Requirements

For FHA and USDA, wells must meet these minimum distances:

75 ft from septic tank’s leach field

50 ft from septic tank

10 ft from property line

If state or local rules require greater distances, those take priority. Lower distances may be allowed with supporting documentation.

VA and Conventional: Must meet local health department requirements.

Pest / Termite Inspection

Conventional, FHA, USDA: Only required if the appraiser notes a concern.

VA: Required in most counties. Borrower cannot pay for the inspection.

Kentucky Takeaway

If a property uses well or septic and you're using FHA, USDA, or VA financing, expect additional scrutiny. These requirements aren’t difficult, but missing one can stop a loan cold. Align early with your lender, appraiser, and home inspector so nothing slips through the cracks.

Need help navigating a property with well or septic?

I specialize in FHA, VA, USDA, and KHC loans across the entire state of Kentucky. If you're buying a home with a private well or septic system and want the fastest path to a clear-to-close, reach out today.

Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA

Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA(NMLS #1738461) | Individual NMLS #57916

10602 Timberwood Cir. Suite 3, Louisville, KY 40223

Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA

Inspection & Testing Requirements for a Kentucky Mortgage

Each Kentucky Home loan program for Conventional, FHA, VA and USDA government mortgage loans has slightly different guidelines when it comes to water tests, septic inspections, and pest/termite inspections. Here's a quick comparison of the general guidelines for each program.

Kentucky USDA Rural Housing Eligibility Map and County List 2026 | Zero Down Homes

Kentucky USDA Rural Housing & Property Eligibility Guide for 2026

Kentucky homebuyers using the USDA Rural Housing program in 2026 need a fast and accurate way to verify whether a property is located in an eligible rural area.

This updated guide includes your Kentucky USDA map images, a full county eligibility list, income-limit guidance, and a simple tool to check property eligibility by address.

Check Kentucky USDA Property Eligibility for 2026

Enter the full property address below to instantly confirm whether the home is located in a USDA-eligible rural zone.

2026 USDA Property Eligibility County List for Kentucky

All non-hyperlinked counties are fully eligible.

Jefferson County (Louisville) and Fayette County (Lexington) remain completely ineligible for USDA Rural Housing in 2026 due to population size.

Adair

Allen

Anderson

Ballard

Barren

Bath

Bell

Boone

Bourbon

Boyd

Boyle

Bracken

Breathitt

Breckinridge

Bullitt

Butler

Caldwell

Calloway

Campbell

Carlisle

Carroll

Carter

Casey

Christian

Clark

Clay

Clinton

Crittenden

Cumberland

Daviess

Edmonson

Elliott

Estill

Fayette (ineligible)

Fleming

Floyd

Franklin

Fulton

Gallatin

Garrard

Grant

Graves

Grayson

Green

Greenup

Hancock

Hardin

Harlan

Harrison

Hart

Henderson

Henry

Hickman

Hopkins

Jackson

Jefferson (ineligible)

Jessamine

Johnson

Kenton

Knott

Knox

Larue

Laurel

Lawrence

Lee

Leslie

Letcher

Lewis

Lincoln

Livingston

Logan

Lyon

McCracken

McCreary

McLean

Madison

Magoffin

Marion

Marshall

Martin

Mason

Meade

Menifee

Mercer

Metcalfe

Monroe

Montgomery

Morgan

Muhlenberg

Nelson

Nicholas

Ohio

Oldham

Owen

Owsley

Pendleton

Perry

Pike

Powell

Pulaski

Robertson

Rockcastle

Rowan

Russell

Scott

Shelby

Simpson

Spencer

Taylor

Todd

Trigg

Trimble

Union

Warren

Washington

Wayne

Webster

Whitley

Wolfe

Woodford

Kentucky USDA Rural Housing Property Eligibility County List Map for Eligible Properties

USDA Property Eligibility Text Description County List for Kentucky

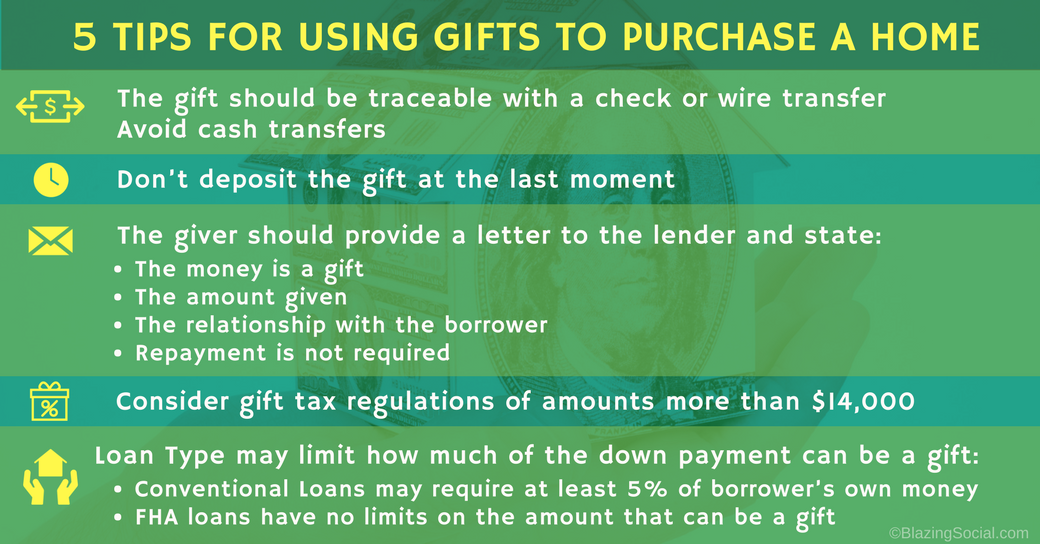

Using Gift Funds for a Down Payment in Kentucky (Updated 2025)

Many Kentucky homebuyers rely on financial help from family or close friends when buying a home. Gift funds can make the upfront investment far more manageable and can strengthen a buyer’s overall approval profile. Here is a clear breakdown of how gift money works across today’s loan programs and what documentation lenders require to use it.

Who Can Give a Down Payment Gift?

Eligible donors usually include parents, grandparents, children, siblings, fiancés, domestic partners, or other close family members. FHA and VA also allow gifts from close friends with a documented long-standing relationship. Gifts from sellers, builders, real estate agents, or anyone with a financial interest in the sale are not allowed unless structured as an approved credit through the contract.

How Gift Funds Help

Gift funds can reduce the cash needed to close and may help the loan qualify more easily. Lower borrower-funded contributions can improve reserves, reduce debt-to-income stress, and in some cases improve pricing. For first-time homebuyers in Kentucky using programs such as FHA, VA, USDA, or KHC, gift funds remain one of the most common tools to get to the closing table with minimal cash.

Conventional Loan Gift Rules (Fannie Mae vs. Freddie Mac)

Fannie Mae

100% of the down payment can be gifted on one-unit homes.

No minimum borrower funds required unless the property is a multi-unit or second home.

Freddie Mac

Often requires at least 5% of the purchase price from the borrower’s own funds if the down payment is under 20%.

Some lenders still follow this rule even when overlays vary.

Gift Documentation Requirements

Signed gift letter stating no repayment is expected.

Donor’s name, relationship, and contact information.

Proof of donor’s ability to give (bank statement or screenshot).

Proof the gift was transferred into the borrower’s account.

Gift Tax Considerations

Gift tax rules apply to the donor, not the buyer. The IRS allows an annual exclusion per donor, per recipient. Larger gifts may require a simple tax form from the donor, but this rarely affects the mortgage process. Underwriting only cares that the funds are a legitimate gift and are fully documented.

Using Gift Funds with Kentucky Housing Corporation (KHC)

Kentucky Housing Corporation allows gift funds with Regular DPA and SmartBuy DPA programs. These can be applied to minimum investment, closing costs, or prepaid expenses. For buyers aiming to bring little to no money to closing, combining gift funds with KHC assistance and seller credits can be a strong structure.

Avoid cash deposits; always use traceable transfers.

Have donors coordinate with your loan officer before sending funds.

Keep all statements, screenshots, and receipts.

Notify your lender early so the gift is structured properly.

Final Thoughts

Gift funds are a powerful way to reduce or eliminate upfront cash requirements. FHA, VA, USDA, and most Conventional programs allow them with proper documentation. Combined with Kentucky Housing Corporation assistance, many borrowers can reach the closing table with minimal or even zero out-of-pocket cost.

For help structuring your loan with gift funds or Kentucky first-time buyer programs, contact:

Joel Lobb, Mortgage Loan Officer

Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA

NMLS 57916 | Company NMLS 1738461

Call or Text: 502-905-3708

kentuckyloan@gmail.com

www.mylouisvillekentuckymortgage.com

Using Gift Funds for a Down Payment in Kentucky (Updated 2025)

Many Kentucky homebuyers rely on financial help from family or close friends when buying a home. Gift funds can make the upfront investment far more manageable and can strengthen a buyer’s overall approval profile. Here is a clear breakdown of how gift money works across today’s loan programs and what documentation lenders require to use it.

Last Updated: September 2025 | By Joel Lobb, Kentucky Mortgage Expert | NMLS #57916

Think a 580 credit score means you can’t buy a home in Kentucky? You can. This guide shows how FHA, VA, and USDA approvals work for fair-credit borrowers.

Quick answer: A 580 credit score can be approved in Kentucky through FHA, VA, or USDA. We do these approvals across the state every month.

Understanding your 580 credit score in Kentucky

A 580 score is in the fair range. While conventional loans and KHC down payment assistance typically want 620+, FHA, VA, and USDA were built to help modest credit histories become homeowners.

Where 580 sits — and why government-backed loans still work.

FHA loans for 580 credit scores in Kentucky

Why FHA fits: 3.5% minimum down payment at 580, available statewide, gifts and seller credits allowed, flexible underwriting, assumable for resale value.

Credit score: 580 qualifies for 3.5% down

DTI target: 45.99 on front end and 56.99 on a AUS approval and on manual underwriting approvals can do go 40% to 50% with compensating factors % or lower when possible

Credit improvement strategies to get your score above 580

Pay down credit cards under 30% utilization

Dispute errors; remove active disputes before underwriting

Document rental history; add a secured card if file is thin

Avoid new credit until after closing

Quick wins that can move a 580 into better pricing or KHC eligibility with a 620 score

Real Kentucky success stories

Jennifer (Lexington): 583 score → FHA 3.5% down; seller-paid costs → closed on $175k home

David (Warren County): 589 score → USDA zero down in eligible area → ownership on a teacher’s salary

Maria (Louisville): 584 score veteran → VA zero down, no MI → competitive monthly payment

Frequently asked questions

Can I really get approved with a 580 credit score in Kentucky?

Yes. We close 580-score FHA/VA/USDA approvals every month. Government-backed programs are designed for fair-credit borrowers with stable income.

What is the minimum down payment at 580?

FHA: 3.5% down. VA: $0 down for eligible borrowers. USDA: $0 down in eligible rural areas.

How long does approval take?

Pre-approval: same day. Clear-to-close typically 18–30 days after contract; total 30–45 days.

Will my rate be higher at 580?

Usually modestly higher than prime-credit, but FHA/VA/USDA pricing is often competitive. You can refinance later as credit improves.

Should I wait to improve credit before applying?

If you’re ready to buy and income is stable, apply now. We can pair approval with a credit plan and revisit refinancing later.

Your next step: get pre-approved so you can shop with confidence.

Joel Lobb is a licensed Kentucky Mortgage Loan Officer (NMLS #57916) with 20+ years of experience. He specializes in government-backed mortgages for fair-credit borrowers and has helped more than 1,300 Kentucky families buy homes.

Educational only; not financial advice. Programs, rates, and requirements change. Not all borrowers qualify. Not endorsed by FHA, VA, USDA, or any government agency. Joel Lobb is licensed to originate mortgages in Kentucky only.

2026 Kentucky VA Home Loan Guide: How to Qualify for a VA Mortgage in Kentucky

Updated for 2026. If you are a veteran, active-duty service member, or eligible surviving spouse looking to buy a home in Kentucky, the VA loan program is still one of the most powerful mortgage options available.

This guide walks you through exactly how Kentucky VA mortgage qualifying really works in 2026 – including credit scores, income, debt-to-income (DTI) ratios, residual income requirements, entitlement and loan limits, plus real-world examples of how lenders underwrite VA loans in Kentucky today.

As a local mortgage broker focused on Kentucky FHA, VA, USDA, KHC and Fannie Mae loans, my role is to translate the rules and overlays into a clear plan so you can see what it takes to qualify, where you stand today, and what needs to happen next to get you into a home.

Why VA Loans Are So Powerful for Kentucky Buyers in 2026

$0 down payment in most cases – no minimum down when entitlement and income qualify.

No monthly mortgage insurance (PMI) – a big monthly savings vs. FHA or low-down conventional.

Flexible credit – VA itself does not set a minimum credit score; lender overlays do.

Competitive interest rates compared to many other loan types.

Reusable benefit – you can use your VA eligibility more than once.

Assumable loans – in some cases, another qualified buyer can assume your VA loan later.

When structured correctly, a VA loan can put you into a Kentucky home with no money down, no PMI, and a fixed 30-year payment that is competitive with rent in many counties.

Step 1: VA Eligibility – Who Qualifies for a VA Loan?

Before we talk about credit scores and income, we have to make sure you meet the VA eligibility requirements and can obtain a Certificate of Eligibility (COE).

Typical VA Service Requirements (High-Level)

Active Duty: Generally 90 days of continuous active service during wartime or 181 days during peacetime.

National Guard / Reserves: Typically 6 years of service, or 90 days of active-duty service under certain call-ups.

Surviving Spouses: Certain un-remarried surviving spouses of veterans who died in service or from a service-connected disability may be eligible.

You do not have to memorize these rules. When we pull your COE, it will show:

Whether you’re eligible

Whether you have full entitlement or partial entitlement

Any notes about prior VA loans or disability benefits

Action step: If you’re not sure about your eligibility, I can help you pull your COE electronically as part of your pre-approval.

2026 Credit Score Guidelines for Kentucky VA Loans

This is one of the biggest areas of confusion, so let’s separate VA rules from lender overlays.

VA’s Rule vs. Lender Overlays

VA itself: The VA does not set a minimum credit score in its handbook.

Lenders in 2026: Most Kentucky lenders and investors expect at least a 620 middle score for standard VA approvals.

That means:

If your credit score is 620 or higher, we’re usually working inside normal AUS (automated underwriting system) approvals.

If your score is between 580–619, approvals are still possible, but you’re more likely to need:

Strong compensating factors and/or

A manual underwrite with tighter DTI and stronger residual income.

Below 580 is case-by-case and heavily dependent on recent credit behavior, late payments, collections, and how the rest of the file looks.

A borderline credit score does not automatically kill a VA loan – but it does change how tight we have to be on DTI, residual income, reserves, payment shock, and other risk factors.

Income, DTI & Residual Income – How VA Underwriting Really Works in 2026

VA loans look at both your Debt-to-Income (DTI) ratio and your residual income (the money left over after paying taxes, housing, and debts). In 2026, most Kentucky lenders are operating roughly like this:

Automated Underwriting (AUS) – More Flexibility

With a strong file and 620+ scores, DTI can go into the 55–65% range or even higher with AUS approval and solid compensating factors.

AUS considers:

Credit history (late payments, collections, public records)

Verified income stability

Verified rent history

Reserves (money left in the bank after closing)

Residual income compared to VA guidelines

Manual Underwriting – 41% DTI Guideline

If the file cannot get an AUS approval and has to be manually underwritten:

Back-end DTI guideline is 41% (total debts including new house payment ÷ gross income).

Underwriters are required to document compensating factors when DTI exceeds 41% and/or when residual income is just over the threshold.

If residual income exceeds VA’s guideline by 20% or more, it can support approval even with a higher DTI in some cases.

Key Compensating Factors Kentucky Underwriters Look For

Strong residual income compared to the required minimum

Verified on-time rent or mortgage history

Significant cash reserves after closing

Limited use of revolving credit; low balances vs. limits

Low payment shock (new payment not far above current rent)

Stable employment or long-term income in the same line of work

Residual Income Requirements for Kentucky VA Loans

Residual income is the amount of money you have left over each month after paying:

Taxes and withholdings

New VA mortgage (principal, interest, taxes, insurance, HOA if applicable)

All other monthly debts (car loans, credit cards, student loans, child support, etc.)

Kentucky is in the South Region for VA residual income. The VA publishes minimum residual income tables by region, family size, and loan amount. For most VA buyers in Kentucky with loan amounts over $80,000, the 2025 tables (which 2026 is expected to closely resemble) show minimums around:

Family of 1: around $441 per month

Family of 2: around $738 per month

Family of 3: around $889 per month

Family of 4: around $1,003 per month

Family of 5: around $1,039 per month

For families larger than 5, VA typically adds around $80 per additional household member. Always refer to the latest published VA tables for exact figures.

Helpful reference: You can review a current VA residual income chart for the South region (which includes Kentucky) here:

Example: Kentucky Family of Four – Residual Income

Let’s say:

Gross monthly income: $6,000

Estimated total taxes/withholding: $1,200

New VA house payment (PITI + HOA): $1,600

Other monthly debts: $600

Calculation:

$6,000 (gross income)

– $1,200 (taxes/withholding)

– $1,600 (new VA payment)

– $600 (other debts)

= $2,600 residual income

If the required residual income for a family of four in the South region is roughly $1,003 and you have $2,600 left over, you are significantly above the minimum – a strong positive for underwriting, especially if your DTI is on the high side.

Full vs. Partial VA Entitlement and Loan Limits in 2026

Full Entitlement – No VA Loan Limit

If your COE shows that you have full entitlement (often described as “This veteran’s basic entitlement is $36,000” with no reductions), then:

You do not have a formal VA loan limit.

You can often buy a home in Kentucky with zero down as long as:

The lender approves the loan based on credit, income and debts.

The VA appraisal supports the value.

In other words, with full entitlement, the true “limit” is what you can qualify for and what the property will appraise for – not an arbitrary VA cap.

Partial Entitlement – Tied to Conforming Loan Limits

If you still have a VA loan outstanding or lost some entitlement due to a prior foreclosure or short sale, you may have partial entitlement. In those cases, your maximum zero-down amount is tied to the FHFA conforming loan limit for the year.

For 2025, the baseline conforming loan limit for a 1-unit property is $806,500 in most U.S. counties.

Each year, FHFA may adjust these limits based on home prices. The VA then uses those numbers to calculate how much entitlement you have left for a no-down-payment purchase.

For 2026, you will want to look up the current conforming limit for your Kentucky county and then have your lender calculate how much zero-down purchasing power you have based on remaining entitlement.

Action step: If you’ve used a VA loan before, we’ll pull your COE, review any outstanding VA loans, and walk through an entitlement calculation so you know your maximum zero-down price range.

Property & Occupancy Rules for Kentucky VA Loans

VA loans are meant for owner-occupied primary residences. In Kentucky, that usually means:

1–4 unit properties (you must occupy one of the units as your primary residence).

Single-family homes in cities, suburbs, and rural areas.

VA-approved condos or townhomes.

Some manufactured homes (case-by-case, depending on foundation, age, and lender overlays).

You cannot use a VA loan to buy an investment property that you do not intend to occupy. However, you can buy a multi-unit property (like a duplex) and live in one unit while renting the other.

Step-by-Step: How to Get Approved for a Kentucky VA Mortgage in 2026

Initial call or online inquiry – We talk through your goals, service history, income, and main questions.

Pull COE and credit – We confirm your VA eligibility and pull a tri-merge credit report.

Income and asset review – You send recent paystubs, W-2s, tax returns (if needed), and bank statements.

AUS run (or manual pre-underwrite) – We run your file through VA’s automated system or line it up for manual underwriting.

Pre-approval letter – Once we have a strong approval, you and your Realtor know your price range.

Find a home and make an offer – Your pre-approval and VA benefit often strengthen your offer.

Appraisal, title, and final underwriting – We order the VA appraisal, clear conditions, and finalize your approval.

Closing – You sign final documents, get your keys, and move into your new Kentucky home.

When Does a Kentucky VA Loan Need a Manual Underwrite?

Not every file will get an AUS “Accept.” Some common reasons for a manual underwrite include:

Limited or “thin” credit history

Recent late payments, collections, or charge-offs

Prior bankruptcy, foreclosure, or short sale

Non-traditional credit (no credit scores, but documented rent and alternative accounts)

Borderline residual income or higher DTI

Manual underwrites in 2026 still get approved every day – but they require:

Stronger documentation

Clear compensating factors

Better residual income relative to the VA table

More conservative DTI (targeting the 41% back-end guideline)

If I see early in the process that your file is likely to be manual, we’ll plan the documentation and structure upfront so there are fewer surprises in underwriting.

How VA Loans Compare to FHA, USDA & Conventional in Kentucky

If you qualify for VA, it is almost always worth putting at the top of the list because you get no PMI and $0 down in many cases. That said, there are times when we still compare VA to other programs:

FHA Loans in Kentucky – Popular with first-time buyers who don’t have VA eligibility or have lower scores. FHA has a minimum 3.5% down payment and monthly mortgage insurance.

Learn more about Kentucky FHA mortgage loans

USDA Rural Housing Loans – Zero-down loans for eligible rural areas and income limits. Great for buyers in qualifying Kentucky counties who don’t have VA eligibility.

Explore Kentucky USDA rural housing loans

Conventional (Fannie Mae) Loans – Strong option for higher scores and buyers with larger down payments. Sometimes used when borrowing above certain VA thresholds or when a borrower wants a different structure.

Compare Kentucky FHA vs. Conventional loans

Kentucky Housing Corporation (KHC) Programs – State programs that can help with down payment and closing costs, often paired with FHA or Conventional and sometimes with VA where guidelines allow.

Kentucky first-time homebuyer and KHC programs

During your consultation, we’ll run side-by-side numbers so you can see whether VA, FHA, USDA, KHC, or Conventional gives you the best payment and the strongest approval path.

Real-World 2026 Kentucky VA Loan Scenarios

Scenario 1 – First-Time Buyer, 620 Score, Strong Income

First-time Kentucky homebuyer, veteran with full entitlement.

620–640 score, stable W-2 income, low other debts.

DTI at 45–50%, residual income comfortably above the South region table.

Result: Likely AUS approval, $0 down, no PMI, very straightforward VA loan.

Scenario 2 – Higher DTI, Strong Residual Income

Veteran buying move-up home; DTI around 60% after including new payment.

Family of 4 with strong income and significant residual income above the guideline.

Good payment history and several months of reserves left after closing.

Result: AUS may still approve despite high DTI because residual income, credit history and reserves offset the risk.

Scenario 3 – Manual Underwrite After a Credit Event

Veteran with a past bankruptcy or foreclosure that is now seasoned.

Scores in the high 500s/low 600s with recent on-time payments.

DTI tightened to stay around or under 41%, with residual income above the table.

Result: Manual underwrite with thorough documentation and clear compensating factors; still very possible to close if the rest of the file is strong.

FAQ: 2026 Kentucky VA Mortgage Qualifying

What credit score do I need for a Kentucky VA loan in 2026?

VA does not publish a minimum score, but most lenders in 2026 want to see around a 620 middle score. Below that, approvals are still possible but are more likely to need strong compensating factors and, in some cases, manual underwriting.

How high can my DTI be and still get approved?

On AUS approvals, we sometimes see DTI in the mid-50s to low-60s qualify when the rest of the file is strong. Manual underwrites are typically capped near the 41% back-end ratio, unless residual income and other factors justify an exception.

What is residual income and why does it matter?

Residual income is what’s left over after you pay taxes, the new VA mortgage, and all other monthly debts. VA has regional tables for minimum residual income. For Kentucky (South region), meeting or exceeding that number is a key part of getting approved – especially if your DTI is high.

Can I use my VA loan benefit more than once?

Yes. You can reuse your VA benefit multiple times as long as you restore or have remaining entitlement. We review your COE, any existing VA loans, and help you understand your remaining eligibility.

Can I buy a duplex or multi-unit with a VA loan in Kentucky?

Yes, VA allows 1–4 unit properties as long as you occupy one of the units as your primary residence. Rental income from the additional units may help qualify in some cases.

Can I roll closing costs into my VA loan?

In many cases, yes. You can use seller credits, lender credits, or in some cases a slightly higher rate to offset costs. We’ll structure your purchase to minimize cash to close while keeping your payment affordable.

Get a 2026 Kentucky VA Loan Game Plan

If you’re a veteran, active-duty service member, or eligible surviving spouse in Kentucky, you’ve earned this benefit. The next step is simply getting a clear, honest look at where you stand and what it will take to qualify.

Here’s what I’ll do for you:

Review your COE, credit, income, and debts.

Lay out your maximum price range, estimated payment, and closing cost options.

Show you whether VA, FHA, USDA, KHC, or Conventional gives you the best structure.

Build a step-by-step roadmap if you’re a few moves away from qualifying today.

Serving veterans and homebuyers in all 120 counties across Kentucky.

Legal & Compliance:

This article is for educational purposes only and does not constitute a commitment to lend or an offer of credit. All loan programs, terms, and guidelines are subject to change without notice. Final approval is based on underwriting review of your complete application, credit, income, assets, property, and applicable program guidelines. VA loans are offered through approved lenders; this website is not endorsed or sponsored by the U.S. Department of Veterans Affairs or any government agency.

Kentucky New Construction Loans with 3.5% Down Payment Assistance

By Joel Lobb, Mortgage Broker – FHA, VA, USDA, KHC, Fannie Mae

NMLS #57916 | Company NMLS #1738461

3.5% Down Payment Assistance for Completed New Construction Homes in Kentucky.

3.5% Down Payment Assistance for Completed Construction Homes

If you are building or buying a completed new construction home in Kentucky, coming up with the cash for

down payment and closing costs can slow everything down. This 3.5% down payment assistance (DPA) program

pairs a competitive 5/1 ARM first mortgage with a repayable 3.5% DPA second to help

buyers close with less money out of pocket.

The goal is simple: make Kentucky new construction loans more affordable for buyers

while giving builders a clean way to move inventory without cutting price. For buyers who want to compare this

to other Kentucky down payment assistance options through KHC,

this program can be part of a larger strategy, not a one-size-fits-all answer.

How This Kentucky New Construction DPA Program Works

The structure is straightforward. Buyers receive:

A 5/1 ARM first mortgage at a competitive rate.

A 3.5% down payment assistance second lien that is repayable.

The assistance can be used toward several upfront costs that usually keep buyers on the sidelines. When we look

at your file, we also compare this structure to

Kentucky USDA zero-down home loans

and KHC loan programs

so you can see which option actually delivers the best fit.

What the 3.5% Down Payment Assistance Can Be Used For

Down payment on a completed new construction home.

Prepaid items such as taxes and insurance.

Closing costs charged by the lender, title company, and other parties.

Temporary or permanent interest rate buydowns to lower the monthly payment.

Used correctly, this Kentucky down payment assistance program can reduce the buyer’s cash to close and

create a more comfortable payment from day one. If you are also researching your

credit score needed for a Kentucky mortgage,

it’s important to know that both the first mortgage and DPA second have minimum credit and underwriting guidelines.

Benefits for Kentucky Homebuyers

Buyers looking online for Kentucky new construction loans are usually focused on three

things: monthly payment, cash to close, and long-term flexibility. This 3.5% DPA option helps in all three areas.

Lower cash to close: Assistance can cover part of the down payment and closing costs.

Payment relief: Funds can be structured toward rate buydowns to help manage the payment in the early years.

Flexible structure: Buyers can combine this with other incentives, gifts, or seller credits where allowed.

Benefits for Builders and Developers in Louisville and Across Kentucky

For builders, this program is a clean Louisville builder financing solution that helps

buyers say “yes” without forcing deep price cuts or heavy concessions.

No price reduction required: Use financing instead of discounting the list price.

Move standing inventory: Turn qualified traffic into real contracts.

Helps more buyers qualify: By assisting with upfront costs, more buyers can make the numbers work.

Works with completed construction: Ideal for finished homes that are ready to close.

If you are a builder or listing agent with completed homes in Louisville, Lexington, Bowling Green, or other

Kentucky markets, this down payment assistance option can become part of your standard financing toolkit alongside

USDA, FHA, VA, and KHC down payment assistance.

Who Is a Good Fit for This Kentucky New Construction Program?

Buyers purchasing a completed new construction home in Kentucky.

Clients who have stable income but limited cash for down payment and closing costs.

First-time buyers and repeat buyers who want to preserve savings.

Builders with move-in ready homes who want a structured financing solution for their buyers.

Full underwriting guidelines will apply, including credit score, debt-to-income, income documentation, and

property eligibility. Not all borrowers or properties will qualify. If you’re unsure whether your current profile fits,

review the credit score and approval guide for Kentucky mortgages

and then reach out for a tailored scenario.

How the 5/1 ARM Works with the 3.5% DPA

The first mortgage is a 5/1 ARM, which means the interest rate is fixed for the first

five years and can adjust annually after that based on the terms of the note.

Years 1–5: Fixed introductory rate, often lower than a comparable 30-year fixed rate.

After year 5: Rate can adjust annually up or down within specified caps.

DPA second: The 3.5% assistance is structured as a second lien that is repayable based on program terms.

For many buyers, this structure can be a smart option if they plan to refinance in the future, move, or expect

income growth before the first adjustment period. We’ll compare this alongside fixed-rate products, USDA, KHC,

and other Kentucky down payment assistance programs

to make sure the ARM structure actually makes sense for your timeline.

Comparing This Program to Other Kentucky Down Payment Assistance Options

I have helped Kentucky homebuyers since 2001 with FHA, VA, USDA, KHC, and conventional mortgage programs.

My focus is on providing clear, honest guidance so you understand your options and choose the loan that fits

your budget and long-term plan.

Whether you are a first-time buyer, a move-up buyer, or a builder looking for reliable

Louisville builder financing support, I am available to walk you through every step. That includes reviewing

USDA Rural Housing loans,

KHC down payment assistance,

and other structures side-by-side with this new construction DPA option.

Every buyer and property are different. The best way to see if this Kentucky new construction DPA program is

right for you is to run a custom quote based on your credit, income, and the specific home you are building or buying.

Next Step: Call or text 502-905-3708, or use the contact form on my website to get started.

Important Disclosures

This is not a commitment to lend or an offer to extend credit. All loans are subject to credit approval,

underwriting guidelines, and program availability. Interest rates, program terms, and eligibility guidelines

may change without notice. Not all borrowers will qualify for all programs described. The 5/1 ARM and 3.5% down

payment assistance program described on this page is for completed new construction homes only and may not be

available in all areas of Kentucky.

Please contact Joel Lobb for the most current information and to receive a customized quote based on your

specific situation.

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204