Closing Costs Kentucky Mortgage

How Much Are Closing Costs in Kentucky? (FHA, VA, USDA, KHC Programs)

By Joel Lobb, Mortgage Broker FHA • VA • KHC • USDA

NMLS #57916 | Company NMLS #1738461 | Equal Housing Lender

Buying a home in Kentucky? Understanding your closing costs is one of the most important parts of your mortgage journey. Whether you’re purchasing through an FHA, VA, USDA, or KHC loan program, knowing the fees and how to reduce them can save you thousands at the closing table.

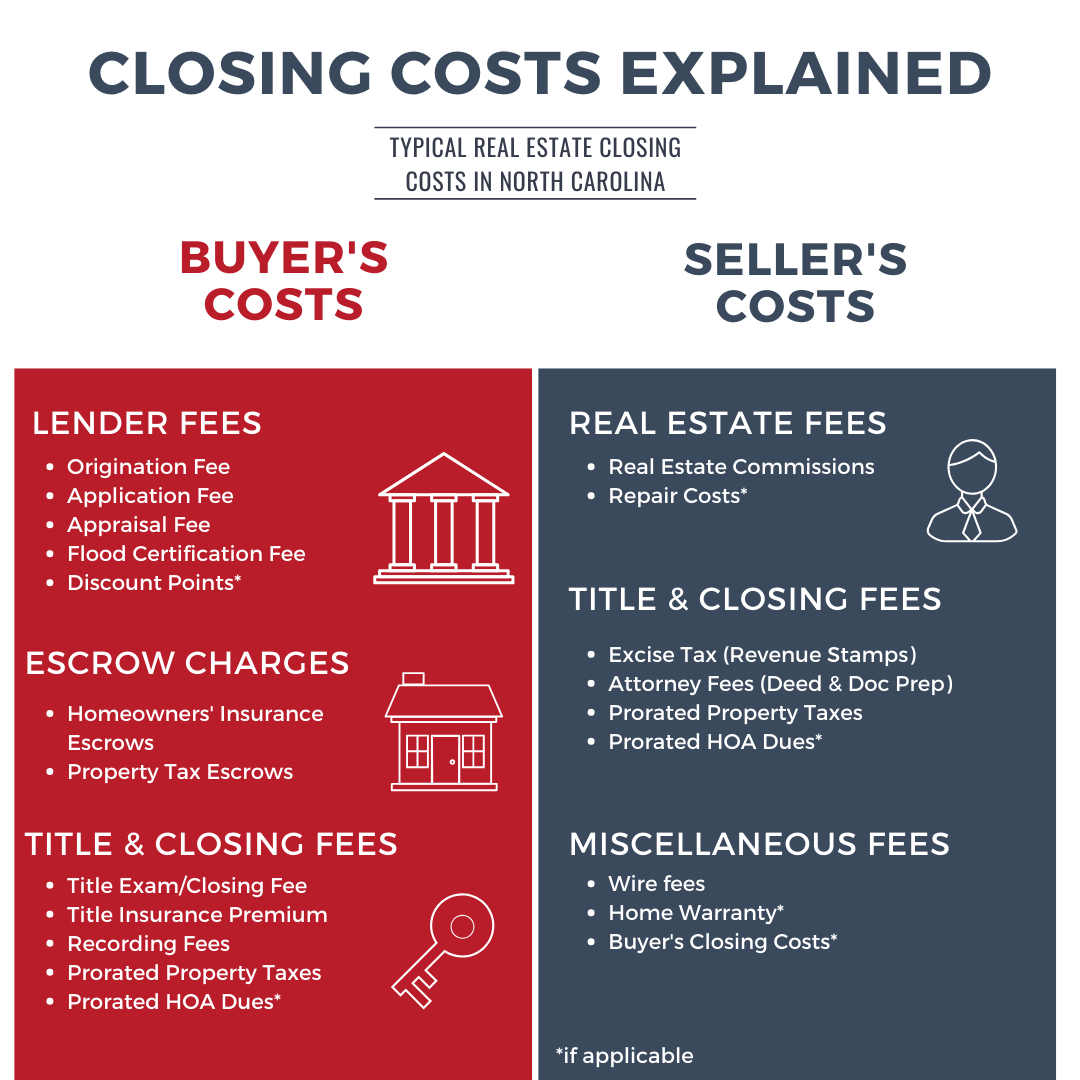

What Are Closing Costs?

Closing costs are the additional fees you pay when finalizing your Kentucky mortgage. These cover loan origination, title work, taxes, insurance, and recording costs. Most buyers pay between 2% and 5% of the purchase price in total closing costs.

Average Closing Costs in Kentucky (2025)

- Typical range: 2%–5% of the home price

- Example: $7,000–$15,000 on a $300,000 home

- Includes: lender fees, title charges, appraisal, and prepaid taxes/insurance

According to Bankrate and Redfin, average Kentucky buyer costs are around 1.4%–2.5% depending on loan type, credit, and county. FHA, VA, and USDA loans each have unique cost structures, while KHC programs can reduce cash to close.

Who Pays the Closing Costs?

Both buyers and sellers share closing costs in Kentucky. Buyers cover lender, appraisal, and title fees. Sellers pay transfer taxes, real estate commissions, and may offer seller-paid credits to help offset the buyer’s costs.

| Party | Typical Costs Covered |

|---|---|

| Buyer | Appraisal, loan origination, credit report, title insurance, recording fees, prepaid taxes/insurance |

| Seller | Realtor commissions, transfer taxes, title preparation, possible closing cost assistance to buyer |

Ways to Reduce Your Kentucky Closing Costs

- Ask your lender about KHC Down Payment Assistance to help cover closing expenses.

- Negotiate seller credits or lender-paid fees when making an offer.

- Shop around for title and insurance providers for competitive pricing.

- Use a VA or USDA 0% down loan to minimize your upfront cash requirements.

Kentucky Loan Programs That Can Help

- KHC Down Payment Assistance: Offers $10,000–$12,500 toward down payment and closing costs.

- USDA Loans: True 0% down program; allows seller concessions to cover closing costs.

- VA Loans: No down payment and no monthly MI; closing costs can be reduced or paid by seller.

- FHA Loans: 3.5% down option; may pair with KHC to reduce total cash to close.

FAQs: Kentucky Mortgage Closing Costs

How much are closing costs in Kentucky?

Closing costs usually range between 2% and 5% of your home’s price, depending on the loan type and location.

Who pays the closing costs?

Buyers typically cover most costs, but sellers often contribute through negotiated credits or KHC assistance.

Can I get help with closing costs?

Yes. KHC Down Payment Assistance and USDA/VA programs allow you to finance or offset some or all closing expenses.

What’s included in the fees?

Appraisal, title insurance, loan origination, prepaid taxes/insurance, and county recording charges.

Ready to Estimate Your Closing Costs?

Start your free pre-approval and see a full closing cost breakdown for your Kentucky home loan. I’ll help you compare FHA, VA, USDA, and KHC options side-by-side.

📝 Get Pre-Approved 📞 Call/Text (502) 905-3708 ✉️ Email JoelNMLS #57916 | Company NMLS #1738461 | Equal Housing Lender

A Complete Guide to Closing Costs

Types of Closing Costs

Let’s talk briefly about the types of closing costs you might encounter and how much those costs tend to run. Understand that closing costs, especially tax-related costs, will vary widely depending on where you live. But some costs can be estimated based on national averages.

Also, you should know that with fluctuations in the real estate market, closing costs are also fluctuating. A 2012 US News article pointed out that closing costs dropped 7 percent over 2011-2012 to an average of about $3,754.

The drops are, in part, because of 2010 regulations that were put in place by the government to shield homebuyers from “closing cost sticker shock.” Now that lenders are better at estimating final closing costs, those costs are dropping naturally.

Still, the national average for closing costs is nearly $4,000, which isn’t pocket change for your average homebuyer. So where’s all that money going? Here are some of the closing costs you might have to pay, along with average costs, based on the Allstate Home Buyers Closing Cost Worksheet.

Mortgage Application Fee:

Appraisal Fee: This fee can sometimes be paid by the seller but is normally paid by the buyer. Basically, the fee goes to a professional appraiser who will ensure that the bank isn’t lending you more money than a property is worth. It’ll cost $100-$400.

Building Inspection: If you need to hire a home, pest or other specialized inspector, you’ll have to pay the fee. Some lenders will require an inspection to make sure the property is in good condition. This fee runs $150-$400 on average.

Survey: This is a fee you’re likely to skip, though it’s required by commercial lenders. It is for a surveyor to check out the lot and the structures on it to ensure the boundaries are properly noted. It can cost $300-$450.

Legal Fees: Although attorney fees will add extra to your bill, you may want to pay a professional to ensure that all the documentation for your home is in order. Some lenders will bring along their own attorney, but yours will ensure that your personal interests are protected. Legal fees can run $300-$600, depending on your attorney and what you’re requiring of him or her.

Title Search and Insurance: A title insurance company will ensure that the title to the home is free and clear — that no one else will have claims on it. Sometimes a title search is separate from title insurance and will cost $150-$200. Title insurance varies but is usually about 1 percent of the home price.

Private Mortgage Insurance (PMI): If you put less than 20 percent down on your home, you’ll likely have to pay PMI. The average PMI premium is 2.5 percent of the mortgage, though your premium will vary depending on the value of your home, your credit score and your down payment. If you need PMI, you’ll likely have to pay a portion of the premium at closing. (Note: If you’re getting an FHA, VA or RHS government-backed loan, you’ll pay something like PMI, but it will be paid to the guarantor.)

Homeowners Insurance: All lenders will require that you carry homeowners insurance on a property as long as it’s mortgaged. Typically, you’ll have to pay the first year’s property insurance premium in advance. Sometimes you’ll pay the insurer directly, but other times you’ll pay at closing.

Prepaid Interest: This one can get a little complicated. Let’s say your mortgage payment is due on the 1st of every month, but you close on your new home on the 15th. If this is the case, the lender will calculate the interest you owe for those 15-16 days remaining in the month, and that interest payment will be due at closing. Sometimes the seller reimburses these costs, since it’s often in his or her best interest to close as soon as possible — before your first mortgage payment is due. These costs will depend on your mortgage amount, interest rate and the time between closing and your first payment coming due.

Points: Points are another form of prepaid interest, but they’re generally not required. You can pay, usually, from 0-4 points on your mortgage. One point equals 1 percent of the total mortgage principal. (If you’re taking out a $100,000 loan, a point is $1,000, for instance.) One point usually reduces your interest rate by 1/8 percent. If you choose to pay points (rather than increasing your down payment), you’ll do so at closing.

Escrow Fees: The majority of homeowners use an escrow system for paying real estate taxes, fire and flood insurance, homeowners insurance and PMI. The escrow account is held either by a third party or by your lender, depending on your circumstances, and it’s used to pay all of the annual or monthly premiums for these important homeownership-related items. When you close on your home, you’ll generally need to put around three months’ worth of escrowed fees in the account.

Realty Transfer Tax: The taxes you pay on transferring a property are similar to the taxes you pay when you buy a new (or new-to-you) vehicle. Taxes vary by your state and municipality.

Recording Fees: Your local government will have to record the purchase transaction of your new home, which will cost $40-$60, on average.

Prorated Expenses: Some of the lump-sum costs associated with your home — water bills, homeowner association fees, condominium fees, etc. — could be split between you and the seller during your transaction. If you buy a home midway through the year, for instance, you may need to pay 50 percent of these fees. These expenses will depend on when you buy your home and are often negotiable with the seller

Ways to Pay Closing Costs

The easiest way to pay closing costs, of course, is cash. If you have enough money in savings to pay for your down payment and your closing costs and to have cash in reserves, this is often the best option.

Paying more closing costs keeps you from taking out a bigger loan and can save you money on mortgage interest, which may save you a fortune over the life of your loan.

Roll it into the mortgage

If you don’t have plenty of cash on hand, you can roll your closing costs into your mortgage. Because closing costs are generally a small amount of money compared with your overall mortgage, most lenders don’t mind rolling part or all of the closing costs into the loan.

However, you do have to be careful because rolling your closing costs into your mortgage may mean you can’t spend as much money on a house. For instance, if, based on your credit, your lender agrees to finance up to 90 percent of the value of a $150,000 home, they may not go over that loan-to-value ratio, even to roll in closing costs.

In this scenario, say you’ve agreed to put $15,000 (10 percent) down on a home worth $150,000. Your lender agrees to finance 90 percent of the home’s value, leaving a $135,000 mortgage. If you don’t have cash for the $5,000 in closing costs, you could ask the lender to roll that into your loan, making your mortgage $140,000.

But if the lender isn’t comfortable financing 95 percent of the home’s value (a very high loan-to-value ratio in the world of home lending), you may be out of luck. In this case, you might have to find a cheaper home so that you can pay a smaller down payment and have money left for closing costs.

One thing to note: many government-backed loans, like the FHA and VA loans, are set up specifically for first-time or lower-income home buyers, who often have trouble saving for a down payment and closing costs. Because of this, it’s common for these loans to roll closing costs into the mortgage and to finance even above 95 percent of the home’s value.

Ask the seller to pay some costs

This is easier to accomplish in a sluggish housing market, or any time the seller is ready to get out of the home ASAP. In some cases, the seller will take part of the closing costs out of the money they’re getting when they sell the home.

If you don’t have money to pay closing costs, this is a good way to save money without increasing your loan (and, thus, your monthly mortgage payments). And what’s the worst that can happen? The seller may just say no.

Ask the lender to pay closing costs

Sometimes a lender will pay your closing costs, even if they don’t roll them into your mortgage. For instance, your lender might just outright pay $4,000 toward your closing costs but then raise the interest rate on your loan by 0.25 percent or more. (They’re not in the habit of giving away free money, after all.)

You’ll need to make sure this doesn’t come back to bite you. Figure out how much that extra interest will cost you over the life of your loan, or at least the length of time you plan to be in the home, and see if this is a reasonable approach for you.

Borrow for your closing costs

Taking out a separate loan for a down payment is usually a no-no. Your main lender wants to be the only one to have a claim on your home if you should default.

However, you could take out an unsecured loan to cover closing costs. Just be careful here, as interest rates could really bite on a personal unsecured loan.

Find Out How Much to Expect in Closing Costs

That’s a lot of information, and, unfortunately, it doesn’t tell you exactly how much you’ll pay in closing costs. You may not know exact closing costs until you’re ready to close on your home, but you can get a good idea of these costs online by using these resources: