Kentucky FHA appraisals can take home buyers by surprise. That’s why we've put together some good-to-know info about the process. Feel free to use this to help educate your clients.

Your Kentucky FHA Home Appraisal Checklist

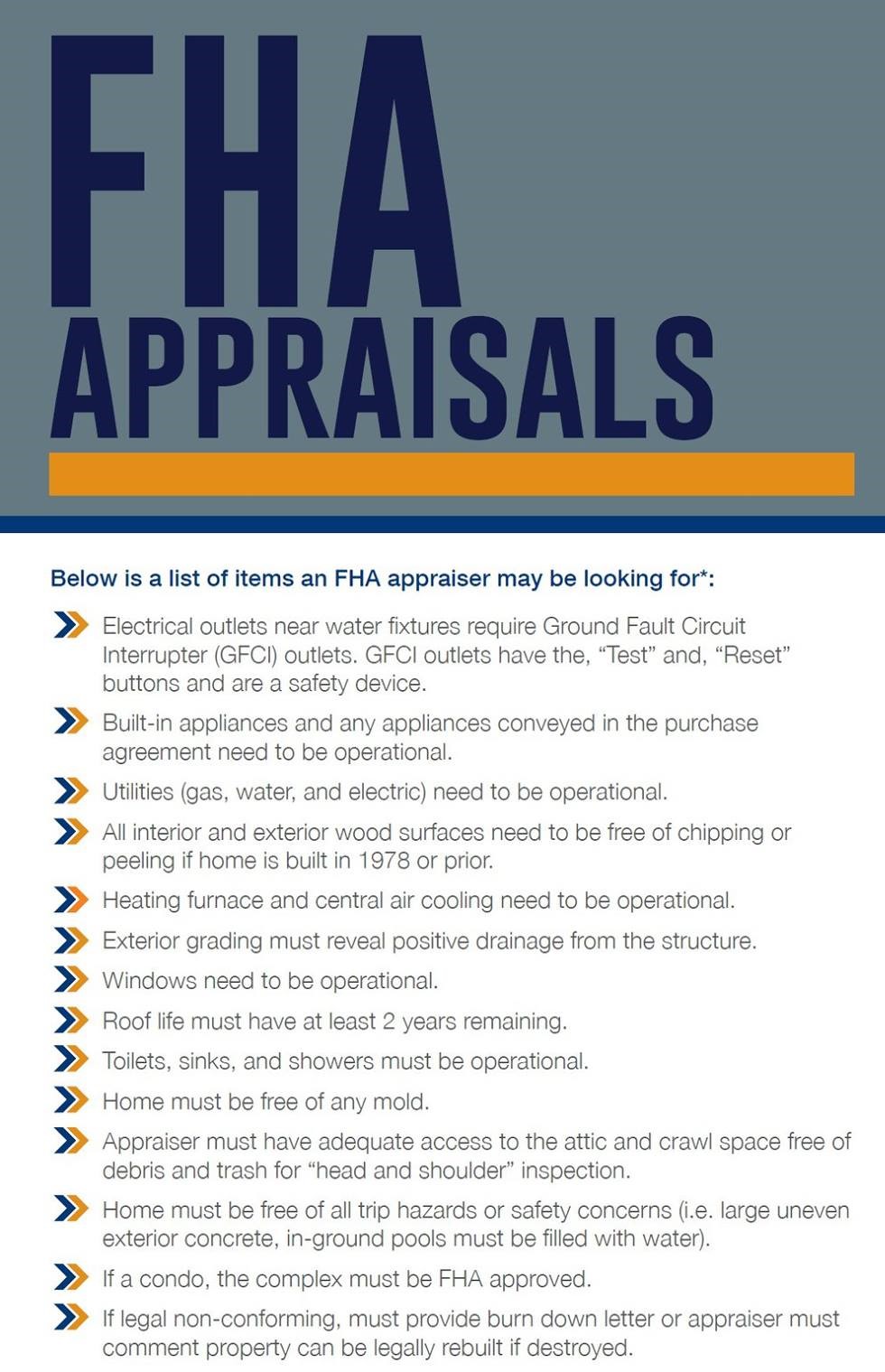

If you’re using an Kentucky FHA loan to buy a home (or selling to FHA borrowers), the property must pass an FHA appraisal, which determines the current market value and makes sure the house meets certain safety standards. Here is a list of items an FHA appraiser may look for:

General Health and Safety

- Foundation or structural defects

- Whether the utilities (water, sewage, heat, and electricity) all work

- Chipped or peeling paint in homes built before 1978

- Incomplete renovations

- Water damage

- If the property is accessible to vehicles, especially emergency vehicles

- Exposed wiring and uncovered junction boxes

- Whether the house is too close to outside hazards, such as a leaking oil tank or a waste dump

- Excessive noise, such as being close to an airport

- Missing handrails

Exterior

- Leaky or defective roof and holes in the siding

- Leaning or broken fencing

- Doors that don’t properly open or close

- Condition of gutters, chimney, stairs, railings, and porches

- If swimming pools are up to code

Every Room

- Whether each room has electricity

- Whether each room has a window or door to the exterior to be used as a fire escape

Kitchen

- Missing or broken appliances usually sold with a home, including stove and refrigerator

- Broken or leaking sink

Bathrooms

- Broken or leaking toilet, sink, or tub/shower

- No ventilation (either an exhaust fan or window)

Crawl space or basement

- Basement moisture

- Evidence of past or present standing water

Heating and Plumbing

- Inoperable HVAC

- Major plumbing issues and leaks

These are some common items an FHA appraiser looks for, but other issues that might make a house unsafe could keep it from passing. An FHA appraisal is not the same as an independent home inspection. It’s still a good idea to get a separate home inspection to make sure you’re making a wise investment!

Updated FHA Info Letter Sent July 12, 2022 for Kentucky FHA Appraisal Reports

✨Applies to case numbers assigned on or after June 1, 2022

✨Updates the initial appraisal validity period from 120 days to 180 days from the effective date of the appraisal report;

🙌🏼Extends the appraisal update validity period from 240 days to one year from the effective date of the initial appraisal report;

✨Allows the appraisal update to be ordered AFTER an appraisal expires; and

👊🏼Eliminates the optional 30-day extension.

✨This is big news for FHA ✨

The guideline change also puts FHA appraisal expirations on par with conventional loan expiration dates.🥊

.jpg "Applies to case numbers assigned on or after June 1, 2022 Updates the initial appraisal validity period from 120 days to 180 days from the effective date of the appraisal report; Extends the appraisal update validity period from 240 days to one year from the effective date of the initial appraisal report; Allows the appraisal update to be ordered AFTER an appraisal expires; and Eliminates the optional 30-day extension. ✨This is big news for FHA ✨ The guideline change also puts FHA appraisal expirations on par with conventional loan expiration dates.")

List of Kentucky FHA Appraisers below:

👇

{kind=link}