Qualifying For a Kentucky Mortgage, Mortgage Rates, Down Payment

A basic truth: A loan holds your house and land as collateral; it's not

pound of flesh, but the loss can seem just as life-threatening.

In most cases, a lender does not really want to end up with your house. They want you to succeed and make those monthly payments that make the world (or at least the U.S. world) go 'round. So when you apply for a loan, the lender will scrutinize your financial situation to make sure you are worth the risk.

You need to get your paperwork in order before you

find a Kentucky Mortgage lender, but first you should understand the basic facts.

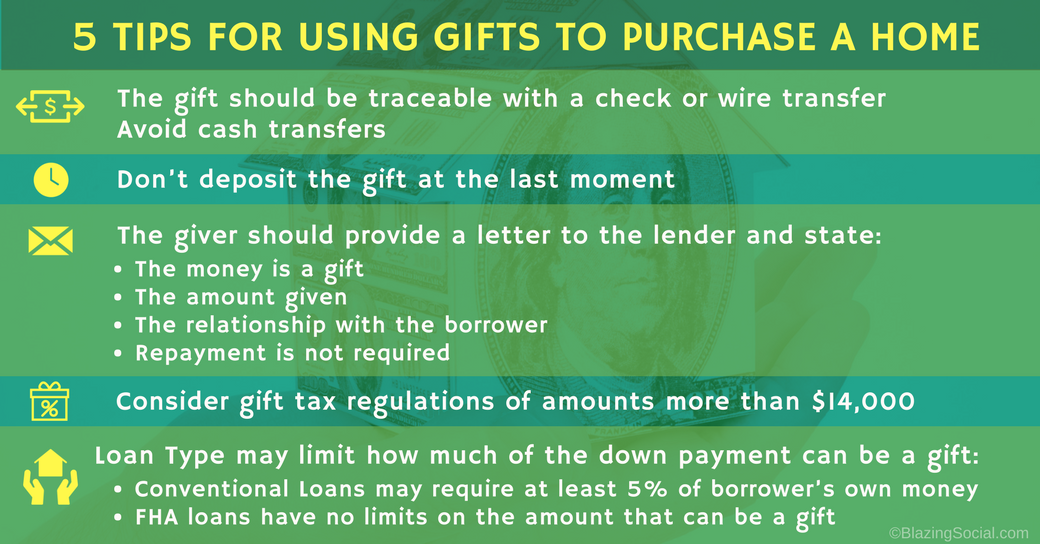

- Down payment. Traditionally, lenders like a down payment that is 20 percent of the value of the home. However, there are many types of Kentucky mortgages that require less. Beware, though: If you are putting less down, your lender will scrutinize you even more. Why? Because the less you have invested in the home, the less you have to lose by just walking away from the loan. If you cannot put 20 percent down, your lender will require private mortgage insurance (PMI) to protect himself from losses. (However, if you can only afford, for example, 5 percent down, but have good credit, you can still get a loan, and even avoid paying PMI. Ask your lender about an 80/15/5 loan — an 80 percent first mortgage, followed by a 15 percent second mortgage, and 5 percent down. This gives the lender more security, while saving you the cost of insurance.)

- LTV. Lenders look at the Loan to Value (LTV) when underwriting the loan. Divide your loan amount by the home's appraised value to come up with the LTV. For example, if your loan is $70,000, and the home you are buying is appraised at $100,000, your LTV is 70%. The 30 percent down payment makes that a fairly low LTV. But even if your LTV is 95 percent you can still get a loan, most likely for a higher interest rate.

- Debt ratios. There are two debt-to-income ratios that you need to consider. First, look at your housing ratio (sometimes called the "front-end ratio"); this is your anticipated monthly house payment plus other costs of homeownership (e.g., condo fees, etc.). Divide that amount by your gross monthly income. That gives you one part of what you need. The other is the debt ratio (or "back-end ratio"). Take all your monthly installment or revolving debt (e.g., credit cards, student loans, alimony, child support) in addition to your housing expenses. Divide that by your gross income as well. Now you have your debt ratios: Generally, it should be no more than 28 percent of your gross monthly income for the front ratio, and 36 percent for the back, but the guidelines vary widely. A high income borrower might be able to have ratios closer to 40 percent and 50 percent.

- Credit report. A lender will run a credit report on you; this record of your credit history will result in a score. Your lender will probably look at three credit scoring models (one for home equity loans or lines of credit) and then average them to arrive at your score. The higher the score, the better the chance the borrower will pay off the loan. What's a good score? Well, FICO (acronym for Fair Isaac Corporation, the company that invented the model) is usually the standard; scores range from 350-850. FICO's median score is 723, and 680 and over is generally the minimum score for getting "A" credit loans. Lenders treat the scores in different ways, but in general the higher the score, the better interest rate you'll be offered. The minimum credit score a Kentucky USDA loan is 640 and for a Kentucky VA loan it is 620 credit score. The minimum credit score for a Kentucky FHA loan is 640

- Automated Underwriting System. The days when a lender would sit down with you to go over your loan are over. Today you can find out if you qualify for a loan quickly via an automated underwriting system, a software program that looks at things like your credit score and debt ratios. Most lenders use an AUS to pre-approve a borrower. You still need to provide some information, but the system takes your word for most of it. Later on, you'll have to provide more proof that what you gave the AUS is correct.

Can Your Afford a Kentucky Mortgage Loan?

Whether you're a

Kentucky first-time buyer looking for the perfect starter house, or a seasoned pro trading up to your waterfront dream home, you are probably asking the same questions: Can I afford this? And is this the

right move at the

right time?

Of course, you can use a

mortgage calculator and ask the experts — lenders, agents, and mom — but the reality is that you are the only one who truly knows whether you can afford to buy right now. And, painful as it is, what you need to start with is a detailed expense breakdown. Analyze what you spend — at least get a full month's snapshot. You'll see where you may have wiggle room in your budget and what you can afford for housing. (Be sure to count all those little incidental expenses like dry cleaning and yes, those mid-afternoon Starbucks lattes count in the budget, too!)

Sample Budget

This sample budget belongs to a single, 35-year-old woman making $68,000 per year, renting a two-bedroom apartment. Her monthly pre-tax income is $5,667.

Monthly expenses:

| Rent | $1,600 |

| Car payment | $225 |

| Credit card payments | $200 |

| Car insurance | $75 |

| Groceries | $400 |

| Health insurance/renters insurance | $208 |

| Electricity | $40 |

| Natural gas | $70 |

| Cell phone | $49 |

| Home phone + Internet access | $72 |

| Cable TV | $50 |

| Gas, dining, clothes, dry cleaning, gifts, other expenses | $800 |

| Memberships (gym, professional, etc.) | $100 |

| Water/sewer/garbage | $0 |

| Property tax/homeowners insurance/condo fees | $0 |

| Alarm company | $0 |

| Lawn | $0 |

| Total | $3,889 |

The sample budget may not look like your expense snapshot, but by adding and subtracting your personal budget items with an eye toward true monthly out-of-pocket totals, you get a pretty good picture. Now, add in all of the expenses where the zeros are as well as the increased cost of your monthly mortgage payment (formerly rent). Maintenance costs like condo fees, utilities, the leaky bathroom sink that defies a simple trip to Home Depot to fix, property taxes,

closing costs, and furniture for your new home all add to the bottom line.

Debt-to-Income Ratios

If you figure out that you can afford your projected budget, chances are you'll qualify for a mortgage in your range. Lenders will determine how much loan you can afford by using something called your debt-to-income ratio, which is the ratio of a borrower's total debt as a percentage of their total gross income. Basically, they will look at what's left in your budget after your monthly bills are paid. These include credit card payments, car payments, child support, etc.

- Housing ratio (or "front-end ratio"): Lenders want your total mortgage debt (called PITI — an acronym for Principal, Interest, Taxes, and Insurance) and condo fees to be no more than 30 percent of your gross monthly income; 28 percent is standard.

- Overall debt ratio (or "back-end ratio"): These are revolving monthly payments, such as credit card, car lease, or loan payments, student loans, child support, alimony, monthly utilities. (They do not include those lattes, but you might want to plug in your lifestyle expenses for your own sake.) The ratio should not be more than 36 percent.

Debt-to-income ratio standards differ from lender to lender, and vary based on your loan program, but most lenders will give more weight to your credit history as a factor in determining your particular situation. Here is a typical ratio for a first-time buyer:

- Monthly gross household income:

- $5,700

- Mortgage debt ratio:

- 28% $1,596.0

- Expenses and overall debt:

- 36% $2,052.0

The mortgage debt of $1,596 is right in line with the current monthly rent payment in the example above. As long as the monthly debt obligations and household expenses are no higher than $2,000-2,300, this borrower should have no problem qualifying.

If your credit is stellar, you will be rewarded. Lenders may stretch these ratios to 38/45, allowing you to purchase more home and take advantage of more lending programs. And if you are a

Kentucky first-time home-buyer applying for an Kentucky

FHA or VA loan, you may also be able to qualify with a higher back-end ratio — up to 41 percent of your monthly gross income — and get approved for these federally-insured loans.

How It Works

So, back to the question: How much home can I afford?

Keeping in mind the variables on debt-to-income ratios and the many lending programs available, here is a sample breakdown for a mid-range home.

| Monthly gross household income (pre-tax): | $7,000 | |

| Mortgage debt ratio | 28% | $1,960 |

| Home price | $350,000 | |

| 20% down payment | $70,000 | |

| Mortgage | $280,000 | |

| Interest rate on 30-year mortgage | 6.33% | |

| Mortgage payment (principle and interest) | $1,739 | |

Here is an example of a lower price-range home, purchased with the same loan terms and interest rate:

| Monthly gross household income (pre-tax): | $3,600 | |

| Mortgage debt ratio | 28% | $1,008 |

| Home price | $150,000 | |

| Mortgage payment (principle and interest) | $1,739 | |

| 10% down payment | $15,000 | |

| Mortgage | $135,000 | |

| Interest rate on 30-year mortgage | 6.33% | |

| Mortgage payment (P&I) | $838 | |

And the Other Costs...

In addition to the monthly mortgage payment, remember to factor in the added costs of home purchase and ownership. Since this buyer above did not put 20 percent down, he will need to add mortgage insurance, also known as PMI, to his monthly payment. PMI protects lenders against losses that can occur when a borrower defaults on a loan, and is required for borrowers with a down payment of less than 20 percent of the purchase price. Buyers also incur closing costs of 2.5 to 3 percent of the total loan amount. This covers the cost of title searches, appraisals, legal fees, etc.

So what's left to apply to the down payment? Using the example above, our first-time buyer has $15,000 for the down payment on a $150,000 home, and the closing costs may come to $4,500. The mortgage total just increased to $139,500. Over the 30-year loan period, this brings the mortgage payment to approximately $866 per month. If your head is not already spinning, now tack on mortgage insurance (fees vary based on the loan), homeowners' taxes and condo fees (if applicable), bringing the total monthly payment to approximately $1,038. The good news is this is still well in the range of the acceptable debt ratio.

Keep Some Money in Reserve

Many buyers invest every red cent they have into their new purchase, but it's a good idea to keep some emergency cash, or "leaky faucet money," aside in the event of emergency repairs or a job loss. So don't completely raid your savings; with home ownership, expect the unexpected.

Joel Lobb

(NMLS#57916)Senior Loan Officer

502-905-3708 cell

502-813-2795 fax

jlobb@keyfinllc.comKey Financial Mortgage Co. (NMLS #1800)*

107 South Hurstbourne Parkway*

Louisville, KY 40222*