Kentucky FHA Gift of Equity and Gift Funds for Down Payment Requirements

Gifts may be provided by:

• Borrower's family member*;

• the borrower's employer or labor union;

• a close friend with a clearly defined and documented interest in the borrower;

• a charitable organization;

• a governmental agency or public entity that has a program providing homeownership assistance to:

• low or moderate income families; or

• first-time homebuyers.

*Family member defined as:• child, foster child, parent, or grandparent; spouse or domestic partner;

• legally adopted son or daughter, including a child who is placed with the borrower by an

authorized agency for legal adoption;

• brother, stepbrother, sister, stepsister;

• uncle or aunt

• son-in-law, daughter-in law, father-in-law, mother in-law, brother-in-law, or sister-in-law of

the borrower.

Guidelines - Personal Gift Funds

• Primary residence 1-4 unit only

• Funds may not be used to fulfill mandatory reserve requirements for manually underwritten

files.

• No borrower funds are required for down payment.

• Cash on hand is not an acceptable source of donor funds.

Documentation - Personal Gift Funds

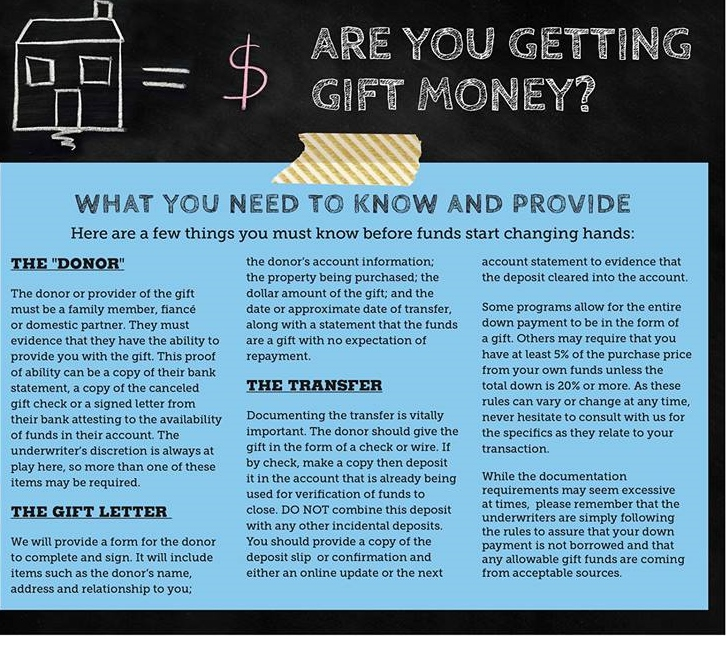

• Gift letter - See Requirements in "Notable Agency Differences" Above

• If the gift funds have been verified in the borrower's account, obtain the donor's bank

statement showing the withdrawal and evidence of the deposit into the borrower's account.

• If the gift funds are not verified in the borrower's account, obtain the certified check or

money order or cashier's check or wire transfer or other official check, and a bank statement

showing the withdrawal from the donor's account.

• If the gift funds are paid directly to the settlement agent, verify that the settlement

agent received the funds from the donor for the amount of the gift, and that the funds were from an

acceptable source.

• If the gift funds are being borrowed by the donor and documentation from the bank or other

savings account is not available, have the donor provide written evidence that the funds were

borrowed from an acceptable source, not from a party to the transaction.

Regardless of when gift funds are made available to a borrower, the lender must be able to make a

reasonable determination that the gift funds were not provided by an unacceptable source. This

usually requires a copy of the donor's bank statement.

Guidelines - Gift of Equity

• Family member is ONLY eligible donor for gifts of equity

• Limited to 85% LTV unless:

o residence is currently selling-family member's primary residence or

purchasing family member has been renting residence 6 months prior to sales contract date.

Documentation - Gift of Equity

Gift Letter - See Requirements in "Notable Agency Differences" Above

Call/Text - 502-905-3708

Call/Text - 502-905-3708

FHA gift funds can come from family members, employers, charities, and government programs

FHA gift funds can come from family members, employers, charities, and government programs