I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

FHA Gift Funds Kentucky 2025 | Gifts of Equity & Down Payment Guide

FHA Gift Funds Kentucky 2025: Complete Guide to Gifts of Equity & Down Payment Assistance

Last Updated: October 2025 — FHA loans remain one of the most accessible pathways to homeownership for Kentucky first-time buyers. If you've been told you can't afford a home because of down payment requirements, think again. Understanding how FHA gift funds and gifts of equity work could open the door to your dream home with as little as 3.5% down.

Kentucky first-time homebuyers with FHA gift funds make homeownership more affordable

Many Kentucky homebuyers don't realize they can receive financial help from family, friends, or even employers to cover their down payment and closing costs. This guide explains exactly how FHA gift funds work, who can provide them, and what documentation you'll need to get approved.

Who Can Give FHA Gift Funds in Kentucky?

The HUD 4000.1 Handbook outlines several acceptable sources for FHA gift funds. The key requirement: the funds must be a gift, not a loan.

FHA gift funds can come from family members, employers, charities, and government programs

Eligible donors include:

Family members — parents, grandparents, siblings, children, spouse, or in-laws

Employers or labor unions — who offer down payment assistance programs

Close friends — with documented proof of relationship

Government or public agencies — like KHC (Kentucky Housing Corporation) programs

💡 Important: Sellers, builders, and real estate agents cannot provide gift funds. FHA lenders verify this to prevent fraud and ensure true down payment assistance.

FHA Definition of "Family Member"

For FHA purposes, family includes parents, grandparents, children (including adopted or foster children), siblings, spouses, domestic partners, uncles, aunts, and all in-laws (mother-, father-, sister-, or brother-in-law). This broad definition means most relatives can provide gift funds.

FHA Gift Fund Rules for Kentucky Borrowers: What You Need to Know

Requirement

FHA Rule

Property Type

Primary residence (1–4 family units)

Minimum Down Payment

No minimum required (can be 100% gift)

Maximum LTV (Loan-to-Value)

Up to 96.5% with 3.5% down

Gift Fund Use

Down payment, closing costs, pre-paid expenses

Reserves

Gift funds cannot count toward reserve requirements

Cash on Hand

Not acceptable (funds must be traceable)

Repayment

Strictly prohibited — must be a gift, not a loan

Documentation Required for FHA Gift Funds

The most critical part of using gift funds is documentation. Lenders need proof that:

The donor has the funds available

The funds came from a legitimate source

No repayment is expected

The money actually transferred to you

Required Documents Checklist

Signed gift letter — states the amount, relationship, and that no repayment is expected

Donor's recent bank statements — typically last 2 months showing the gift fund withdrawal

Your bank statements — showing the deposit of gift funds

Wire receipt or cashier's check proof — if funds go directly to closing

Written explanation — if any gaps appear between withdrawal and deposit

Pro Tip: Have the donor wire funds directly to your account or the title company, or use a cashier's check. This creates a clear paper trail. Lenders want to see documented proof that doesn't raise red flags.

Understanding FHA Gifts of Equity in Kentucky

A gift of equity is a unique FHA program that helps when a family member sells you their home. Instead of paying full market value, you purchase the home at a lower price, and the difference becomes your down payment credit.

Real-World Example: Gift of Equity in Kentucky

Scenario: Your parent owns a home appraised at $200,000. They agree to sell it to you for $180,000. The $20,000 difference is the "gift of equity." You can use this $20,000 as your down payment on an FHA loan. Your loan would be for $180,000 (or less with additional down payment), and the $20,000 equity gift covers the difference.

FHA Gift of Equity Requirements

Only family members can provide a gift of equity

Maximum LTV = 85% (loan amount ÷ appraised value) unless:

The seller's home is their primary residence, OR

You rented the property for at least six months before the sales contract date

Must be documented in the purchase agreement and appraisal

Documentation for Gift of Equity

Signed gift letter — from the seller acknowledging the equity gift

Current appraisal — showing the true market value

Sales contract — identifying the purchase price and equity gift amount

Proof of relationship — birth certificate, marriage license, or family documents

FHA Gift Letter Template for Kentucky Borrowers

Your FHA gift letter must include specific language. Here's a template you can use:

Sample FHA Gift Letter:

"I, [Donor Full Name], am giving [Borrower Full Name] a gift of $[Amount] for use toward the down payment on the property located at [Property Address]. This gift represents no obligation for repayment. I expect nothing in return for this gift. [Donor Signature] [Date]"

Make sure your lender approves the exact wording before having it signed.

Does Kentucky's KHC Program Accept Gift Funds?

Yes. Kentucky Housing Corporation (KHC) and other down payment assistance programs often work alongside FHA gift funds. Many Kentucky first-time homebuyers combine KHC grants with family gifts to minimize out-of-pocket costs.

Yes. You can receive gifts from multiple family members or organizations. Each gift requires its own gift letter and documentation.

Is there a limit to how much I can receive as a gift?

No. FHA has no maximum on gift amounts, but the full down payment and closing costs can be covered by gifts if properly documented.

Can a gift fund be used for closing costs?

Absolutely. FHA gift funds can cover down payment, closing costs, appraisal fees, inspection costs, and other homebuying expenses.

What if the donor and I live in different states?

That's fine. The donor's location doesn't matter — only that they have a legitimate relationship to you and the funds are properly documented.

Why Work With a Kentucky FHA Loan Expert?

Understanding FHA gift fund rules is complex, and mistakes can delay your approval or derail your loan entirely. Working with a knowledgeable Kentucky mortgage specialist ensures:

Proper documentation — all gifts are verified and approved upfront

No delays — we catch issues before they become problems

Maximum benefits — we identify all programs you qualify for (FHA, KHC, VA, USDA)

Peace of mind — you have expert guidance every step of the way

Ready to Buy Your Kentucky Home With FHA Gift Funds?

Let me help you navigate FHA gift fund requirements and get approved quickly. Whether you're receiving a family gift, a gift of equity, or KHC assistance, I'll ensure everything is documented correctly for a smooth, fast approval.

This is why it's possible to get a little help in the form of a down payment gift from a family member or relative, close friend, or even a charitable organization. And it’s actually becoming more popular, especially among millennials. In the National Association of REALTORS® 2020 Generational Trends Report, 13 percent of home buyers (and 27 percent for ages 22 to 29) indicated their source of down payment to be a gift from their relative or friend.

So if you’re lucky enough to find down payment fund as one of your gifts under the Christmas tree this year (or maybe you’re the one who wants to give it), it may not be as simple as opening your cash gift (or handing someone a wad of cash) and going straight to the lender to use it to buy a home.

Down payment gift funds, whether you’re giving or receiving it, are closely regulated by lenders and must meet certain requirements. Here are certain rules that the gift giver and recipient should know to avoid trouble down the road.

While we may automatically consider a family member, like parents or siblings, when thinking about who can give a mortgage down payment gift, there are other entities who could also be eligible gift sources. But because cash can come with strings attached, and lenders want to make sure that the gift money is nothing but a gift (which will be discussed later on), there are restrictions on who can give money (or who you can give money to) to help purchase a home.

For conventional loans

If you are getting a loan through Fannie Mae or Freddie Mac, gifts can only be from a family member or relative. This may be your spouse, child, siblings, parents, grandparents, or anyone related by blood, marriage, adoption, or legal guardianship. Soon-to-be family members such as your domestic partner, fiancé, or even future in-laws are also eligible to give funds for a down payment.

For FHA loans

The Federal Housing Administration (FHA) has its own set of rules when it comes to giving or receiving down payment gifts, although they offer a broader eligibility range. If you are getting an FHA loan, you can receive down payment funds from family members, friends who have a clearly defined and documented interest in your life, employers, labor unions, government agencies, and even charitable organizations.

For USDA and VA home loans

VA loans (backed by the U.S. Department of Veterans Affairs) and USDA mortgages (given by the U.S. Department of Agriculture)may have fewer restrictions, but the down payment gift funds cannot come from anyone who would benefit from the proceeds of the purchase, such as the seller, developer, builder, your real estate agent, and some other entity.

There are no limits on the amount of money someone can give you for a down payment or to cover closing costs. However, rules still apply depending on the type of loan and property you're purchasing. Some types of loans may need you to contribute a certain amount of the down. The key is to check with your lender for the latest regulations on how much you can really use.

Likewise, there can be tax implications on the person giving the gift funds. They may be liable if the amount exceeds the gift tax exclusion limit. As of 2020, for instance, any individual can give funds up to $15,000 without a tax penalty. On the other hand, parents who are married and are filing jointly can give up to $30,000 per child for a mortgage down payment (or any other purpose), without incurring the gift tax. For a down payment gift that exceeds the said amounts, the donor must file a gift tax return to disclose the gift.

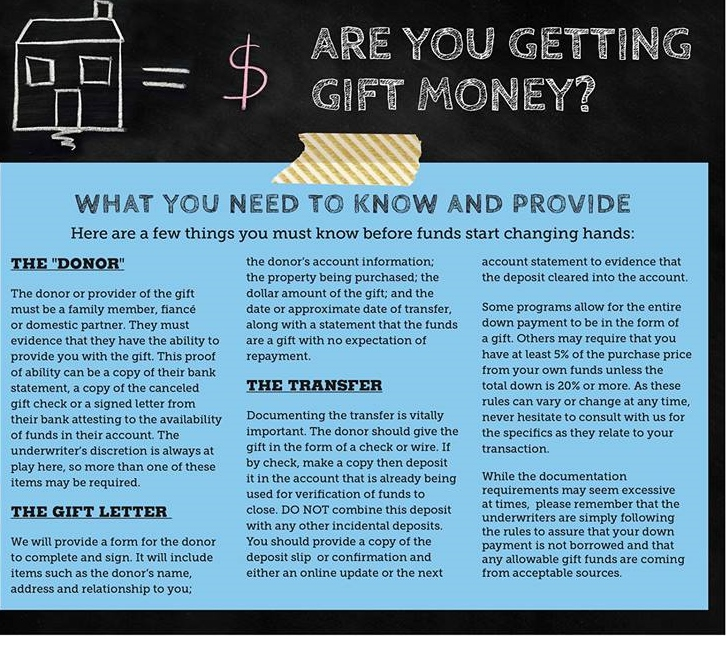

You need to confirm the relationship between you and the giver and provide the right paperwork.

If you're fortunate enough to have a family member or any eligible entity who can give you funds towards your home’s down payment, you’ll need to confirm your relationship with the gift-giver and provide your mortgage underwriter more information about where the funds came from.

For lenders to confirm that the new money isn’t a loan, you’ll need these things:

1. A down payment gift letter - If your lender has a template letter for this purpose, you will need to send it to the funds’ donor. If there isn’t a template, you might want to ask what information should be included so you can draft your own.

The letter typically includes details about the gift-giver, such as the name, address, contact phone, relationship to the borrower, and address of the property to be purchased. The date when the gift was transferred and the amount of funds given to the borrower must also be indicated. The donor should also write a sentence explaining that the fund is a gift and that there isn’t any expectation of repayment. The letter must be signed by both the gift-giver and the borrower.

2. The gift-giver’s bank statements - This is to show they have the funds to give the buyer as much money as promised.

3. A bank slip from the buyer’s account - This is to indicate when the money was transferred, to verify that the cash is from a legitimate source and that the borrower has an appropriate relationship with the donor, and to confirm the information provided in the letter.

Remember: you can't pay back the gift.

Down payment gift funds need to be just like that—a gift and not a loan that is expected to be paid. You need to make it clear with your mortgage lender that the money you received was entirely gifted and not something that you need to pay back eventually, because by then it will be considered mortgage or loan fraud. Besides, it can also put your loan qualification at risk since your debt-to-income ratio will be factored when you get a mortgage.

Try to make it a “seasoned” gift money.

It might make more sense to try and make your gift money “seasoned”, especially if you know that someone is going to help you buy a home (often in the case of parents or other relatives). Lenders refer to it as seasoned money when it has been sitting in your bank account for some time, at least for two months. When the gifted money is given in advance, you often don't have to worry about writing gift letter documentation.

Bottom Line

Down payment gift funds make it easier for first-time home buyers to afford a home. If you anticipate accepting help, remember to consider the rules above so you can accept such a gift in a proper manner. Be upfront with your mortgage lender if you plan on using gift funds for the down payment. Don't forget to also talk to the individual or entities who are planning to give you money about the tax implications and other considerations.

Gift Funds for Kentucky Home Buyers | FHA, VA, USDA Mortgage Rules 2025

Kentucky Mortgage Guide

Gift Funds for Kentucky Homebuyers: FHA, VA, USDA & Conventional Rules (2025)

Buying a home in Kentucky with little or no money down is more achievable than you might think. When structured correctly with proper documentation, gift funds can cover your entire down payment and closing costs—making homeownership accessible to families who don't have substantial savings. This guide walks you through exactly how gift funds work across FHA, VA, USDA, and Conventional loans, who can legally give you a gift, and how to avoid the documentation mistakes that slow files in underwriting.

Quick Reference: Gift Funds by Program

Program

Down Payment

Borrower Contribution Required?

Primary Residence

Second Home

FHA

3.5% (up to 96.5% LTV)

No

✓ Allowed

✗ Not Allowed

VA

0% (up to 100% LTV)

No

✓ Allowed

✗ Not Allowed

USDA

0% (up to 100% LTV)

No

✓ Allowed (rural only)

✗ Not Allowed

Conventional

3–20%

No (primary)

✓ Allowed

✓ Allowed*

*Conventional second homes: if LTV exceeds 80%, you'll typically need at least 5% of your own funds.

Who Can Give You a Mortgage Gift? Eligible vs. Ineligible Donors

Not every donation counts as a legitimate gift for mortgage purposes. Lenders distinguish between true gifts (freely given with no expectation of repayment) and other financial arrangements. Here's who can and cannot give you money for your home purchase in Kentucky:

✅ Eligible Gift Donors

Parents, grandparents, siblings, and other blood relatives

In-laws, aunts, uncles, cousins, and legal family

Fiancé or domestic partner (Conventional only)

Employer or labor union

Nonprofit organizations and religious institutions

Government programs like Kentucky Housing Corporation (KHC)

🚫 Ineligible Donors & Sources

The home seller or builder

Your real estate agent or any party to the transaction

Your lender or loan officer

Credit card cash advances or payday loans

Unverifiable cash deposits ("under the table" money)

Any funds expecting repayment (loans, not gifts)

Gift Fund Documentation: What You Must Provide

The most common reason gift-funded deals stall in underwriting is poor or missing documentation. Lenders must create a complete paper trail showing where the money came from, that it's truly a gift, and that it's now in your possession. Here's your checklist:

Required Documentation

Signed Gift Letter – A written letter from the donor that includes:

Donor's full name, relationship to you, and contact information

Amount of the gift

Property address being purchased

Clear statement: "This is a gift with no expectation of repayment"

Signatures from both donor and borrower

Proof of Transfer – Documentation showing the money moved from donor to you:

Bank wire confirmation with sender and recipient info

Cashier's check stub or canceled check

Donor's bank statement showing withdrawal

Your bank statement showing deposit

Source Verification – For gifts over $10,000, lenders may request:

Donor's recent bank statements (60 days)

Verification the funds weren't borrowed from someone else

Pay stubs or investment statements if needed

Pro Tip: Have your donor wire money directly to your escrow or title company when possible. This creates the clearest paper trail and avoids multiple transfers that raise underwriting questions.

How Gift Funds Work by Loan Program in Kentucky

FHA Loans (3.5% Down Payment)

FHA's 3.5% Minimum Required Investment can be 100% gift-funded. Combined with seller closing cost contributions (up to 6%) and lender credits, you can close with zero out of pocket. KHC's Down Payment Assistance Program also works seamlessly with FHA for eligible first-time buyers.

Key Point: No minimum borrower contribution required if gifts or DPA cover the 3.5% plus your closing costs.

VA Loans (0% Down Payment)

VA is the most flexible program for gift funds. There is no minimum borrower contribution—gifts can cover your entire down payment (if any), earnest money deposit, and closing costs. Your VA funding fee (1.25–3.3% depending on disability status and down payment) is typically financed into the loan.

Key Point: Watch the 4% seller concession cap. If seller covers 4% in closing costs, you'll need gifts or lender credits for any remaining costs.

USDA Loans (0% Down Payment)

USDA is 100% financing in eligible rural Kentucky counties. Gift funds cover closing costs and prepaids only—not down payment (since there isn't one). The USDA guarantee fee (1–2%) is financed. Maintain a clear trail: donor → your account → title company or escrow.

Key Point: USDA is strict about source verification. If your gift is large, expect the lender to request donor statements proving the funds are legitimate and not borrowed.

Conventional Loans (3–20% Down Payment)

Primary Residences: Gifts can fund 100% of your down payment and closing costs with no borrower contribution required, up to 97% LTV (Fannie Mae).

Second Homes: Gifts are allowed, but if your LTV exceeds 80%, you must contribute at least 5% of your own funds. For example, on a $300,000 second home with 80%+ LTV, you need $15,000 from your own savings; gifts can cover the remainder.

Key Point: Investment properties cannot use gift funds at all.

Real-World Zero-Down-Payment Scenarios

✓ Scenarios That Work

📋

FHA + Gift + DPA: Family gift for 3.5% down, KHC covers closing costs, seller helps with remaining prepaids.

🎖️

VA + Gift: Full gift from parents covers earnest money and prepaids; VA funding fee financed; seller credits cover remaining costs (capped at 4%).

🌾

USDA + Gift: Small family gift covers property taxes and insurance escrows; seller assists with remaining closing costs.

🏠

Conventional (Primary): Parental gift covers 3% down + closing costs, lender credits cover remainder.

✗ Red Flags That Cause Delays

⚠️

Gifts from interested parties: Gifts from seller, builder, agent, or lender create conflicts of interest.

⚠️

Un-sourced cash deposits: Large deposits appearing suddenly in your account right before closing invite scrutiny.

⚠️

Second home + high LTV: Trying to use 100% gifts on a second home with LTV over 80% violates Conventional guidelines.

⚠️

Missing gift letters: Even with perfect documentation, a missing or vague gift letter can hold up closing.

Pro Tips: How to Use Gift Funds Smoothly

1.Plan Early: Talk to your lender before making an offer. They'll tell you exactly what gift structure works for your program and down payment goal.

2.Wire or Cashier's Check: Have donors wire money directly to escrow, or provide a cashier's check. Avoid cash and personal checks when possible.

3.Get Gift Letters Early: Request signed gift letters at the same time you gather financial documents. Having them ready speeds underwriting.

4.Disclose All Gifts Upfront: Don't surprise your lender with gifts during underwriting. Full transparency prevents last-minute delays.

5.Verify Eligibility: On FHA, VA, and USDA, confirm donors meet relationship requirements. Your lender has a checklist—use it.

More Kentucky Mortgage Resources

Learn more about specific loan programs and down payment assistance:

Ready to Use Gift Funds to Buy Your Kentucky Home?

I'll structure your FHA, VA, USDA, or Conventional loan to maximize your gift funds, create a clean paper trail, and get you to underwriting approval fast.

Joel Lobb, NMLS #57916

EVO Mortgage (NMLS #1738461)

📞 502-905-3708 | ✉ kentuckyloan@gmail.com

Frequently Asked Questions About Gift Funds

Can I receive multiple gifts from different people?

Yes. You can receive gifts from multiple eligible donors. For example, your parents might give $5,000, grandparents $5,000, and an employer might provide $3,000. Each donor needs their own gift letter, but there's no limit on total gifts received.

Do gift funds count toward my debt-to-income ratio?

No. Gift funds do not increase your debt-to-income ratio because they're not a loan. Your lender looks at your income and existing debts (credit cards, auto loans, student loans, etc.) but ignores gift funds when calculating DTI. This can help you qualify for a larger loan amount.

What if my donor doesn't have a bank account?

This is uncommon but possible. If your donor uses cash, they'll need to deposit it into a bank account at least 30–60 days before closing so you can document the source. A large cash deposit right before closing raises red flags and will likely delay your file. Plan ahead.

Can I use a gift for earnest money and down payment?

Absolutely. Gifts can cover earnest money (the deposit you make when making an offer), down payment, and closing costs. Just make sure your lender knows the gift is funding multiple parts of the transaction and documents it clearly.

Will my lender contact my donor?

In most cases, no. Your lender will verify the gift letter and request donor bank statements as needed, but they typically won't call your donor directly. However, they may contact the donor if there are red flags (missing documentation, unclear relationship, etc.). Stay transparent to avoid issues.

Can I use KHC Down Payment Assistance along with a family gift?

Yes. Many Kentucky first-time buyers combine family gifts with KHC down payment assistance programs. For example, a $3,000 family gift might cover your 3.5% FHA down payment, while KHC assists with closing costs. This is one of the most powerful ways to close with minimal out-of-pocket funds.

What if I receive a gift but my loan is denied?

If your loan application is denied, the gift funds remain yours—there's no obligation to repay them (that's what makes it a gift). However, discuss this risk with your donor beforehand. Some donors may want to wait until final approval before providing the money.

Is there a maximum gift I can receive?

There is no maximum limit on the dollar amount of gifts you can receive for mortgage purposes. However, your total down payment cannot exceed program limits. For example, on an FHA loan, your total gift funds cannot exceed the value needed for 100% of your 3.5% down payment and closing costs.

Important Disclosures & Compliance

Equal Housing Lender. All loans are subject to credit, income, and collateral approval. Loan programs, terms, rates, guidelines (FHA, VA, USDA, Conventional, KHC), and down payment assistance are subject to change without notice. Financing availability may vary by property type, occupancy status, credit score, debt-to-income ratio, and location. This information is not an offer to lend and does not constitute loan approval.

Licensing & NMLS: Licensed to originate mortgage loans in the state of Kentucky only. Joel Lobb, NMLS Personal ID #57916. EVO Mortgage, NMLS Company ID #1738461. Verify license status at www.nmlsconsumeraccess.org.

Not Government Endorsed: This website and the information provided are not endorsed, sponsored, or affiliated with HUD, the Federal Housing Administration (FHA), the U.S. Department of Veterans Affairs (VA), the U.S. Department of Agriculture (USDA), the Kentucky Housing Corporation (KHC), Fannie Mae, or any government agency. This is an independent educational and informational resource created to assist Kentucky homebuyers.

Regulatory Authority: The Kentucky Department of Financial Institutions (DFI) oversees mortgage lending in Kentucky. For complaints or inquiries, visit dfi.ky.gov.

External Resources for Gift Funds & Mortgage Guidelines

Call/Text - 502-905-3708

Call/Text - 502-905-3708

FHA gift funds can come from family members, employers, charities, and government programs

FHA gift funds can come from family members, employers, charities, and government programs