I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Last Updated: 2026 – Kentucky FHA Loan Guidelines, Limits, and Requirements Reviewed for Accuracy

Kentucky FHA Loans in 2026: What Is an FHA Loan and Is It Right for You?

An FHA loan is a government-backed mortgage insured by the Federal Housing Administration. FHA loans in Kentucky remain one of the most flexible mortgage options for buyers who may not qualify for conventional financing due to credit challenges, limited savings, or higher debt-to-income ratios.

Because FHA loans are insured by the federal government, approved lenders can offer more forgiving qualification standards while still managing risk.

Mortgage insurance often lasts for the life of the loan

Pros and Cons of FHA Loans in Kentucky

Advantages include lower down payments, flexible credit requirements, and compatibility with Kentucky down payment assistance programs. Disadvantages include mandatory mortgage insurance and stricter property condition standards.

Applying for a Kentucky FHA Loan

You must work with an FHA-approved lender and provide documentation such as income verification, bank statements, and authorization to pull credit. Some documentation may be retrieved electronically by your lender.

There’s no universal minimum credit score needed for a mortgage, but a better credit score will give you more options.

If you’re trying to get a mortgage, your credit score matters. Mortgage lenders use credit scores — as well as other information — to assess your likelihood of repaying a loan on time.

Because credit scores are so important, lenders set minimum scores you must have in order to qualify for a mortgage with them. Minimum credit score varies by lender and mortgage type, but generally, a higher score means better loan terms for you.

Let’s look at which loan types are best for different credit scores.

How to qualify for a mortgage

The type of mortgage you’re applying for determines the minimum requirements you’ll have to meet for your down payment, credit score, and debt-to-income ratio.

Find out what type of loan you might qualify for or what aspects of your finances you’ll need to improve to get a better shot at qualifying for a mortgage.

Loan Type

Min. Down Payment

Min. Credit Score

Max DTI

Property Type

Conventional

3%

620

45%

Primary, secondary, investment

VA

0%

none

none

Primary

FHA

3.5%

500

50%

Primary

USDA

0%

none

41%

Primary

Keep in mind: The minimum down payment, minimum credit score, and maximum DTI shown in the table apply to mortgages used to purchase a primary residence. While you can use a conventional loan or a jumbo loan to purchase a home for another purpose, you might need a larger down payment, a higher credit score, more cash reserves, or all three.

Credit score needed to buy a house

Mortgage lending is risky, and lenders want a way to quantify that risk. They use your three-digit credit score to gauge the risk of loaning you money since your credit score helps predict your likelihood of paying back a loan on time. Lenders also consider other data, such as your income, employment, debts and assets to decide whether to offer you a loan.

Different lenders and loan types have different borrower requirements, loan terms and minimum credit scores. Here are the requirements for some of the most common types of mortgages.

Conventional loan

Minimum credit score: 620

A conventional loan is a mortgage that isn’t backed by a federal agency. Most mortgage lenders offer conventional loans, and many lenders sell these loans to Fannie Mae or Freddie Mac — two government-sponsored enterprises. Conventional loans can have either fixed or adjustable rates, and terms ranging from 10 to 30 years.

You can get a conventional loan with a down payment as low as 3% of the home’s purchase price, so this type of loan makes sense if you don’t have enough for a traditional down payment. However, if your down payment is less than 20%, you’re required to pay for private mortgage insurance (PMI), which is an insurance policy designed to protect the lender if you stop making payments. You can ask your servicer to cancel PMI once the principal balance of your mortgage falls below 80% of the original value of your home.

FHA loan

Minimum credit score (10% down): 500

Minimum credit score (3.5% down): 580

FHA loans are backed by the Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD). The FHA incentivizes lenders to make mortgage loans available to borrowers who might not otherwise qualify by guaranteeing the federal government will repay the mortgage if the borrower stops making payments. This makes an FHA loan a good option if you have a lower credit score.

FHA loans come in 15- or 30-year terms with fixed interest rates. Unlike conventional mortgages, which only require PMI for borrowers with less than 20% down, all FHA borrowers must pay an up-front mortgage insurance premium (MIP) and an annual MIP, as long as the loan is outstanding.

VA loan

Minimum credit score: N/A

VA loans are mortgages backed by the U.S. Department of Veterans Affairs (VA). The VA guarantees loans made by VA-approved lenders to qualifying veterans or service members of the U.S. armed forces, or their spouses. This type of loan is a great option for veterans and their spouses, especially if they don’t have the best credit and don’t have enough for a down payment.

VA loans are fixed-rate mortgages with 10-, 15-, 20- or 30-year terms.

Most VA loans don’t require a down payment or monthly mortgage insurance premiums. However, they do require a one-time VA funding fee, that ranges from 1.4% to 3.6% of the loan amount.

USDA loan

Minimum credit score: N/A

The U.S. Department of Agriculture guarantees loans for borrowers interested in buying homes in certain rural areas. USDA loans don’t require a minimum down payment, but you have to meet the USDA’s income eligibility limits, which vary by location.

All USDA mortgages have fixed interest rates and 30-year repayment terms.

USDA-approved lenders must pay an up-front guarantee fee of up to 3.5% of the purchase price to the USDA. That fee can be passed on to borrowers and financed into the home loan. If the home you want to buy is within an eligible rural area (defined by the USDA) and you meet the other requirements, this could be a great loan option for you.

What else do mortgage lenders consider?

Your credit score isn’t the only factor lenders consider when reviewing your loan application. Here are some of the other factors lenders use when deciding whether to give you a mortgage.

Debt-to-income ratio — Your debt-to-income (DTI) ratio is the amount of debt payments you make each month (including your mortgage payments) relative to your gross monthly income. For example, if your mortgage payments, car loan and credit card payments add up to $1,800 per month and you have a $6,000 monthly income, your debt-to-income ratio would be $1,800/$6,000, or 30%. Most conventional mortgages require a DTI ratio no greater than 36%. However, you may be approved with a DTI up to 45% if you meet other requirements.

Employment history — When you apply for a mortgage, lenders will ask for proof of employment — typically two years’ worth of W-2s and tax returns, as well as your two most recent pay stubs. Lenders prefer to work with people who have stable employment and consistent income.

Down payment — Putting money down to buy a home gives you immediate equity in the home and helps to ensure the lender recoups their loss if you stop making payments and they need to foreclose on the home. Most loans — other than VA and USDA loans — require a down payment of at least 3%, although a higher down payment could help you qualify for a lower interest rate or make up for other less-than-ideal aspects of your mortgage application.

The home’s value and condition — Lenders want to ensure the home collateralizing the loan is in good condition and worth what you’re paying for it. Typically, they’ll require an appraisal to determine the home’s value and may also require a home inspection to ensure there aren’t any unknown issues with the property.

How is your credit score calculated?

Most talk of credit scores makes it sound as if you have only one score. In fact, you have several credit scores, and they may be used by different lenders and for different purposes.

The three national credit bureaus — Experian, Equifax and TransUnion — collect information from banks, credit unions, lenders and public records to formulate your credit score. The most common and well-known scoring model is the FICO Score, which is based on the following five factors:

Payment history (35%) — A history of late payments will drag your score down, as will negative information from bankruptcies, foreclosures, repossessions or accounts referred to collections.

How much you owe (30%) — Your credit utilization ratio is the amount of revolving credit you’re using compared to your total available credit. For example, if you have one credit card with a $2,000 balance and a $4,000 credit limit, your credit utilization ratio is 50%. Credit scoring models view using a larger percentage of your available credit as risky behavior, so high balances and maxed-out credit cards will negatively impact your score.

Length of credit history (15%) — This factor considers the age of your oldest account, newest account and the average age of all your credit accounts. In general, the longer you’ve been using credit responsibly, the higher your score will be.

Types of accounts (10%) — Credit scoring models favor people who use a mix of credit cards, installment loans, mortgages and other types of credit.

Recent credit history (10%) — Lenders view applying for and opening several new credit accounts within a short period as a sign of financial trouble and it’ll negatively impact your score.

Ready to shop around for a mortgage?

Joel Lobb Mortgage Loan Officer Individual NMLS ID #57916

American Mortgage Solutions, Inc. 10602 Timberwood Circle Louisville, KY 40223 Company NMLS ID #1364

The Annual Mortgage Insurance Premium (MIP) will be reduced on all eligible FHA loans through Churchill Mortgage. This premium went from 0.85% to 0.55% for most borrowers with an FHA loan. This will allow borrowers to save an average of $800 each year!

In 2023 alone, this change could help almost 850,000 borrowers. Here’s the details:

Applies to single-family homes, condos, and manufactured homes.

All eligible loan-to-value ratios (LTV) will receive the reduction.

The reduction also works with all eligible base loan amounts.

Here’s a look at the base loan amounts for an FHA loan in 2023:

This reduction in MIP is just another reason it may be time to look into homeownership. The money you’ll be saving can go straight toward a mortgage payment.

Owning a home is considered a secure way to build lasting wealth, even in an uncertain economy. Look at it this way…when you pay rent, you’re paying your landlord’s bills. When you own a home, you’re building equity for YOUR future.

Kentucky FHA Mortgage Facts:

Requires a down payment of at least 3.5%.

With a down payment of at least 10%, MIP can be canceled after 11 years.

A down payment of less than 10% will require MIP for the lifetime of the loan.

The minimum credit score for an FHA loan is 580 to qualify for the 3.5% down payment.

A positive rental history of 12 months of on-time payments can be used as part of your mortgage assessment when applying.

Have Questions or Need Expert Advice? Text, email, or call me below:

Joel Lobb Mortgage Loan Officer Individual NMLS ID #57916

American Mortgage Solutions, Inc. 10602 Timberwood Circle Louisville, KY 40223 Company NMLS ID #1364

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).

FHA vs. Conventional Loans – What is the Difference?: pOne of the most common questions from first-time buyers pertains to the difference between an FHA and a conventional loan, and which one is best for them. We'll clearly define each one and go into further detail about which one might be best for you in your pursuit of purchasing a home./p

There are various types of down payment assistance to buy a home in Kentucky with little or no money down!

Here are a few:

Kentucky FHA loans- federal loan through the Federal Housing Authority-Credit scores low as 620 and gifts can be used or down payment assistance from government agency to meet the 3.5% down payment investment. No income limits but max loan currently is $356,000 in Kentucky for 2021

Kentucky USDA loans- zero down mortgages for rural and suburban homeowners-640 credit score needed currently for most loans and has income limits and property location restrictions

Kentucky VA loans - if military service or active duty, can buy a home with zero down with a 620 minimum credit score. No income restrictions and can buy a house anywhere as long as VA appraisal supports the purchase price. No max loan limits but must meet residual income requirements and Eligibility based off Certification of Eligibly Entitlement. Amount.

Kentucky Housing Down Payment Assistance of $6000 can be used for FHA, VA, USDA or Conventional mortgage loans for their down payment requirements or to help with closing costs. Max income limits and loan limits for this program.

KHC recognizes that down payments, closing costs, and prepaids are stumbling blocks for many potential home buyers. Here are several loan programs to help. Your KHC-approved lender can help you apply for the program that meets your need.

Regular DAP

Purchase price up to $346,644 with Secondary Market.

Assistance in the form of a loan up to $6,000 in $100 increments.

Repayable over a ten-year term at 5.50 percent.

Available to all KHC first-mortgage loan recipients.

Affordable DAP

Purchase price up to $346,644 with Secondary Market.

Credit score tracking is all the rage for personal finance-savvy consumers. With websites like Credit Karma, you can monitor your current score and keep an eye on irregularities in your line of credit.

But those aren’t the numbers used to gauge your credit-worthiness for a loan. Instead, banks rely on what’s known as the FICO score, an amalgamation of information about your ability to pay back credit cards, student loans, car debt and other forms of debt on time.

Here’s why you need a good credit score to buy a home: Credit scores impact the interest rate of your mortgage and could factor into whether you receive a conventional home loan (meaning that they are available/guaranteed through private financial institutions, or one of two government-backed entities, Fannie Mae or Freddie Mac).

You can visit annualcreditreport.com and get a report from one of the three major credit bureaus, Experian, TransUnion and Equifax. This check will not hurt your score, but it will give you an idea of how trustworthy you look to lenders.

If you think your credit is in good enough shape to begin working with a lender, you can ask the financial institution to check your credit. All hard credit checks from mortgage lenders within a 45-day-window are treated like one inquiry. That’ll allow you to compare two to three lenders to see who will offer a more competitive mortgage rate. FICO advises taking advantage of this by shopping around for rates within a 30-day-window.

FICO has updated its scoring method, and new scores will be out in the summer of 2020. But while those new numbers might be a shock, they won’t have much impact on home loans because mortgage lenders prefer to use older FICO scoring models to determine a borrower’s eligibility, NPR reported.

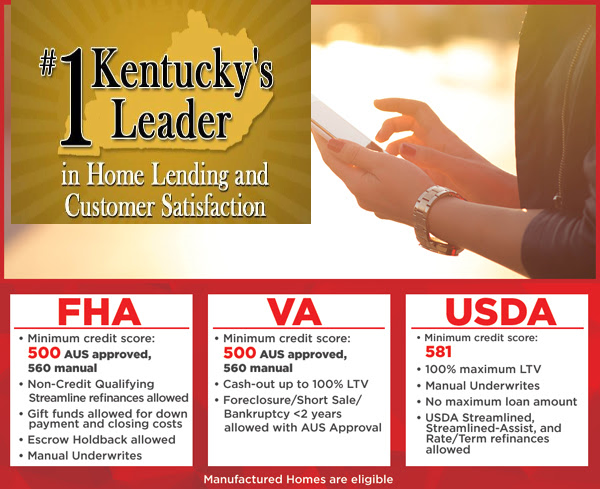

The minimum credit score is 500 for Kentucky FHA loans. However please keep in mind these two things: 1. Lenders credit their own overlays to increase the credit score threshold, most being 620, and secondly, if your credit score is below 580, you would need 10% minimum down payment, and if the credit score is over 580, then you can go with the minimum 3.5% down payment.

Obviously, if you have a higher credit score, this will increase your chances of getting approved for a Kentucky FHA Mortgage and possibly better rates and closing costs options.

Kentucky VA Mortgage loans requirements :

VA does not have a minimum credit score requirement, but if the credit score is below 620 few lenders will do the loan, but I am set up with several Kentucky VA lenders where I have closed them down to a 560 credit score, but the borrower had good compensating factors such as large down payment, low dti ratios, good job history and good residual income with no previous bankruptcies or foreclosures.

I would suggest if your credit scores are below 580, I would suggest on working on getting the scores up before you applied for a VA mortgage loan.

A lot of lenders will do a rapid rescore which in some cases can increase your credit scores in as little as 7-10 working days.

The federal Department of Veterans Affairs (VA) guarantees loans for current and former members of the military and their families. VA loans provide very favorable terms to eligible borrowers and have limited qualifying requirements.

You can get a VA loan with no down payment so long as the home isn’t worth more than you pay for it, and there’s no minimum credit score to qualify. You also don’t have to pay for mortgage insurance, although you do have to pay an up-front funding fee of between .5% and 3.3% of the loan amount unless you fall within an exception for disabled vets or military widows or widowers.

Kentucky USDA Mortgage credit score requirements:

According to their guidelines, USDA will go down to a 580 credit score, but most lenders will want a 640 credit score. USDA uses an online system to underwrite the risk of the loan, and scores under 640 are very difficult to get approved.

Validating the Credit Score. Two or more eligible tradelines are necessary to validate an applicant’s credit report score. Eligible tradelines consist of credit accounts (revolving, installment etc.) with at least 12 months of repayment history reported on the credit report. At least one applicant whose income or assets are used for qualification must have a valid credit report score

The Rural Housing Service (RHS) operates under the federal Department of Agriculture to guarantee loans for rural home-buyers with limited income who can’t obtain conventional financing. The upside is that Kentucky USDA loans require no down payment. The downside is that they charge a steep up-front fee of 1% of the loan amount (which can be paid off over the entire loan term) and an annual fee of 0.35%.

Kentucky Fannie Mae and Freddie Mac Conventional Credit Score Requirements

These are considered “conventional loans’ that can be often be obtained with a 3% to 5% down payment. Of course, there are higher standards for conventional home financing. The most common minimum credit score requirement to get approved today is a 620 FICO.

This type of score is typical for people that have high credit card balances or a few delinquent payments in their past. The general consensus on Freddie Mac and Fannie Mae loans in Kentucky is that a 620 score is the entry-point to qualify, but you will need thorough documentation of income with credit scores in the 620 to 640 range. You will have a better shot to be approved for a mortgage-backed by Fannie or Freddie with a 680-credit score and less strenuous underwriting.

Competitive Mortgage Rates and Fees

Monthly Mortgage Insurance Is Not Always Required

Ideal for First Time Home Buyers with Good Credit

Down Payments For Mortgage Loan Approval

Down payments are fairly straightforward: it’s the amount you pay out initially when agreeing to buy a home, and the more you put down, the less you have to borrow from a mortgage lender to continue gaining equity in a home.

The minimum down payment to get a mortgage is 3.5 percent of the home’s cost, although unless you put down 20 or more percent on a conventional loan (more on that later) or get a mortgage backed by a federal agency, you’ll be subject to paying for mortgage insurance, according to the Consumer Financial Protection Bureau.

Down Payment Closing Cost Assistance

KHC recognizes that down payments, closing costs, and prepaids are stumbling blocks for many potential home buyers. Here are several loan programs to help. Your KHC-approved lender can help you apply for the program that meets your need.

Regular DAP

Purchase price up to $314,827 with Secondary Market.

Assistance in the form of a loan up to $6,000 in $100 increments.

Repayable over a ten-year term at 5.50 percent.

Available to all KHC first-mortgage loan recipients.

Affordable DAP

Purchase price up to $314,827 with Secondary Market.

Assistance up to $6,000.

Repayable over a ten-year term at 1.00 percent.

Borrowers must meet Affordable DAP income limits.

KHC is used for mostly applicants in urban areas of Kentucky that don’t have access to USDA or other government agencies to buy a home with no down payment.

A minimum of 3.5% down payment is required with this loan. Down payment assistance loans are available from $4500-$6,000, and are paid back over a period of ten years. They are typically offered to buyers with limited cash reserves and carry an interest rate of 1 to 5.5%. These loans can make a critical difference to buyers for whom the down payment is an obstacle. Buyers whose 3.5% down payment is less than the $6000 limit may choose to use the remainder of a down payment loan to pay closing costs, further reducing the amount needed to bring to closing.

The Federal Home Loan Bank of Cincinnati (FHLB Cincinnati) has established a set-aside of Affordable Housing Program (AHP) funds to help create homeownership through a program called the Welcome Home Program. Welcome Home funds are available to Members as grants to assist homebuyers.

Welcome Home grants are limited to $5,000 per household, households are eligible only if the total household income is at or below 80% of Mortgage Revenue Bond (MRB) income limits, and funds are offered on a “first-come, first-served” basis. Other program requirements are identified below.

The debt-to-income (DTI) ratio is particularly key for lenders.

Debt consists of how much you currently owe such as student loans, car payments and credit card payments, compared to your gross monthly income (before taxes are taken out).

Fannie Mae, a federally backed company that purchases and guarantees mortgages for borrowers, allows a debt-to-income ratio of up to 45 percent, although it may be as high as 50 percent for people with phenomenal credit scores and incomes.

How lenders use your DTI for a Kentucky Mortgage Loan Approval

Kentucky Mortgage lenders typically use DTI (along with other variables) to determine whether or not you qualify for a loan, and to help determine your Kentucky mortgage rate. A high front-end DTI raises red flags with lenders because it is commonly associated with borrower default. In fact, reducing front-end DTI to reduce the risk of homeowner default was one of the main objectives of the loan modification programs introduced by the government in 2009.

There are specific limits for DTI that are used as cut-off points when evaluating borrowers. Current DTI limits for conventional conforming mortgage loans are typically 28% on the front end and 36% on the back end, though these limits are slightly higher for government subsidized Kentucky FHA loans.

While there are certainly other factors to consider when determining our eligibility for financing (e.g., credit score, etc.), your DTI is an important determinant that you should be aware of. By working to improve it, you can make yourself a better credit risk, and thus get more favorable treatment from lenders.

Two obvious ways to improve DTI are to increase your income and/or decrease your debt. Both are solid goals.

Call us today for a free pre-qualification for your next mortgage loan in Kentucky. We are available 7 days a week to take your call..502-905-3780 or email us at kentuckyloan@gmail.com

Here’s what’s happening: For several years, FHA has insured loans to buyers who previously would have been considered too risky or marginal at best. Those applicants often carried crushing monthly personal debts — for credit cards, auto loans, student loans and other obligations — totaling more than half of their monthly incomes. Many also had histories of credit problems that lowered their credit scores. Combined with skimpy down payments of 3.5 percent and minimal bank reserves, these borrowers have a high statistical probability of defaulting on their loans.

To prevent big losses to FHA’s insurance fund, the agency recently informed lenders nationwide that from March 18 onward, it would be applying more stringent standards to applications from high-risk home-buyers. In its letter, FHA documented its reasons for the crackdown. According to FHA Commissioner Brian Montgomery, the agency has been seeing disturbing trends in the quality of loans lenders have been delivering to it:

— Nearly one of every four approved home purchasers had a debt-to-income (DTI) ratio exceeding 50 percent, the worst since 2000. In January, 28 percent of buyers were in that category.

— FICO credit scores are tanking. They’ve fallen to the lowest level since 2008 — an industry-low average of 670. In the first quarter of fiscal 2019, more than 28 percent of all new purchase loans had FICOs below 640. In the same quarter, more than 13 percent of new loans had scores under 620 — 19 percent higher than the same period in the previous fiscal year. (FICO scores range from 300 to 850; low scores predict higher risks of nonpayment. Average scores for purchasers at giant mortgage investors Fannie Mae and Freddie Mac average around 750.)

— Borrowers are siphoning equity from their homes at an alarming rate. In fiscal 2018, FHA saw a 60 percent increase in “cash-out” refinancing as a percentage of all refinancings. Cash-outs allow borrowers to convert equity into spendable money.

— Growing numbers of loans have multiple indications of serious future risk of nonpayment — combinations of low credit scores of 640 or less and DTI ratios that exceed 50 percent.

Given these omens, FHA clamped down by amending its automated underwriting system. Lenders must now conduct time-consuming “manual” analysis of every new loan application flagged as high risk. Compared with standard automated underwriting, manual processing is far more intensive and entails higher staffing costs and liabilities for lenders. Many balk at it. Some investors refuse to buy manually underwritten loans. As a result, fewer of them make it through the process.

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

-- Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

.png "How to Qualify For a Kentucky FHA Mortgage Loan")