I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Getting approved for a loan is not as hard as some make it. The 3C approach breaks it down in its simplest form so no need to overthink or complicate with “what if’s” or variable situations and these factors are the same in every state. They all have to line up for your loan to be approved but here there are in order of significance

Capacity

- No matter if your credit is in 800’s the ability to afford a loan (capacity aka DTI) is the MOST important C and why most applications either get denied or reduced. Income is EVERYTHING.

To get a conforming (FHA / VA / Conventional) loan you need 2yrs of verifiable Full time income even if it’s pieced together with different employers with 2yrs W2’s and your most recent paystub if you’re an employee and OT and/or bonus cannot be used if you’ve been with your employer for less than 2yrs.

If you have part time employment as well that income cannot be used unless you’ve worked both jobs for at least 2yrs UNLESS your P/T job is the exact same as your F/T job and your hours are not variable then in most cases you can get an exception if you’ve been there for at least 1yr. If you’re self employed 2 most recent tax returns with positive income on line 31 of your schedule C.

If homeownership is your goal, then don’t be cheap and have a certified tax preparer prepare your taxes because it’s likely you’ll need certain docs to get approved only they can provide. Also DO NOT write off all your income to avoid paying the IRS taxes because this will disqualify you from a loan and you’ll have to get a more expensive loan with a bigger down payment.

Credit -

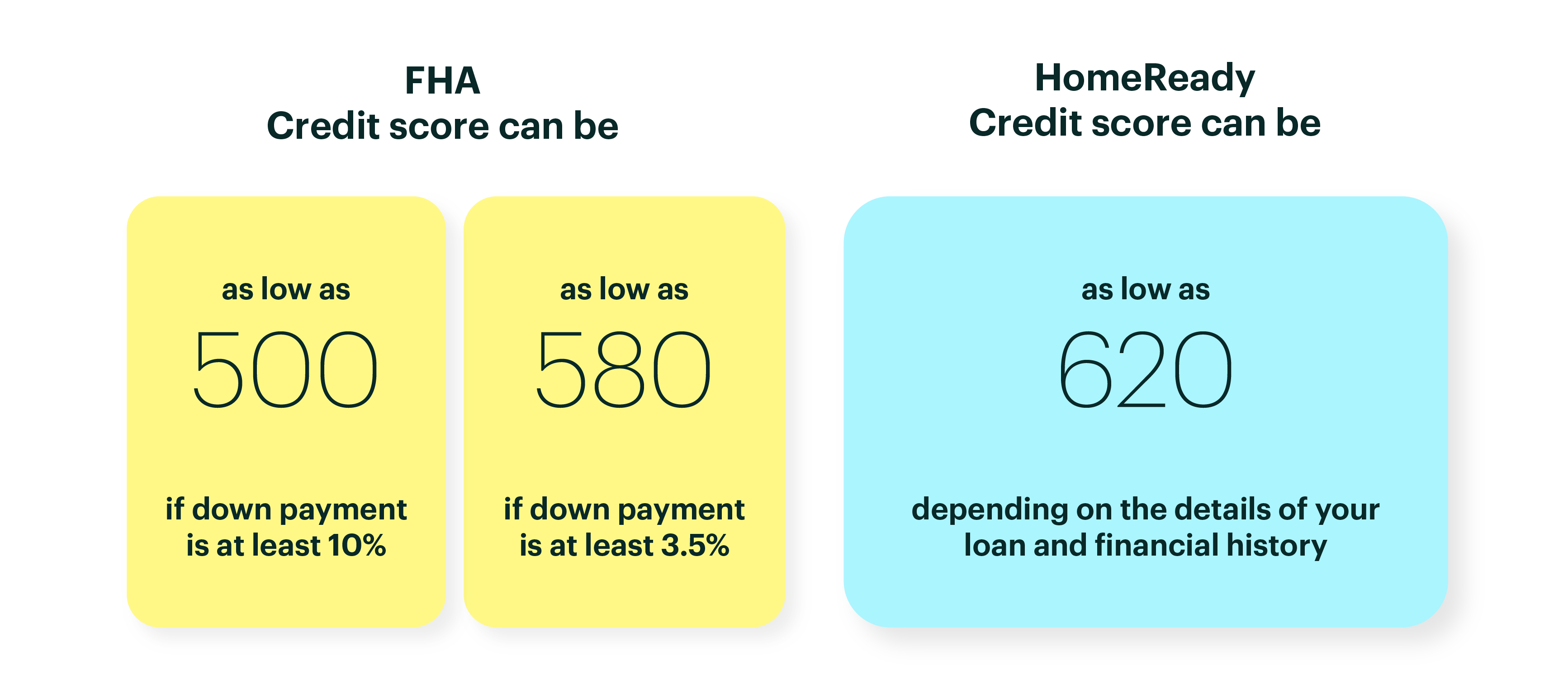

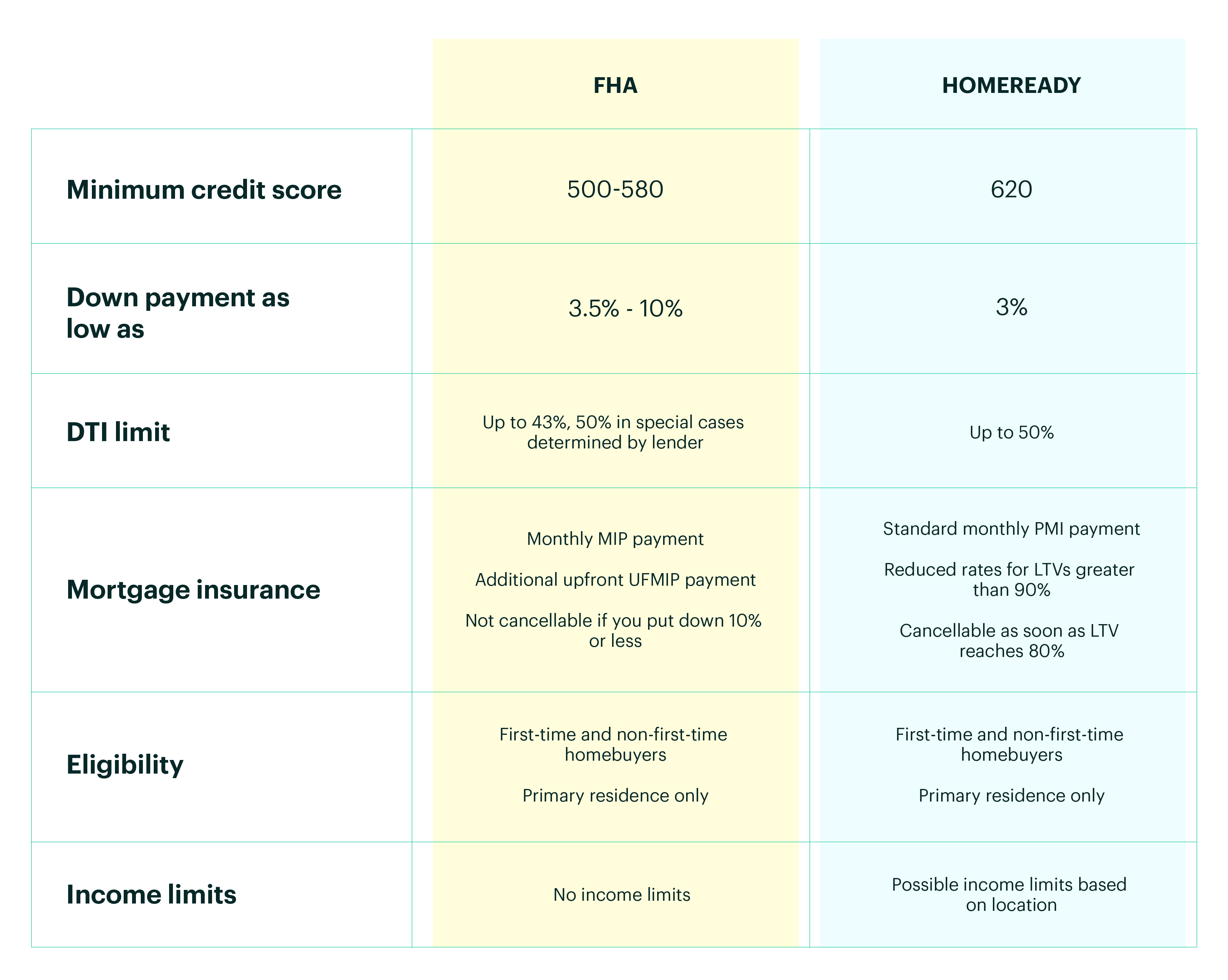

many people think this is the most important but it’s not but it is important. With a high enough capacity (low DTI) I’ve seen clients with minimum scores get approved. FHA requires 580, VA does not have a minimum score requirement and while some lenders can do down in the 500’s generally most lenders do not go below 580, and conventional requires 620.

Having said all that just because you meet the minimum score does not mean you’ll get an approval before credit profile (positive tradeline history, collection activity, credit usage) is what matters most. I’ve seen applicants with 680+ get denied for conventional loans because they have a poor credit profile or low capacity (higher DTI).

FHA is a little more forgiving which is why they are easier loans to get than conventional. Obviously the higher the score, the better the chances are for approval but high scores aren’t needed if capacity and collateral are strong.

Collateral - aka down payment.

Underwriters request either 1 bank statement for FHA or 2 bank statements for conventional and all they are looking for is verification of cash to close, large deposit (FHA more than 1% of loan amount deposited in 1 deposit) activity and reserves if needed, not spending habits. Large purchases are irrelevant and NSF’s can be explained with an explanation letter. The higher the down payment in percentages (3.5 or 5%, 10%, 15%, 20% etc…) not dollars ($2000 or $5000 more than required) then the lower the risk and higher chance of approval especially for conventional loans. Plus dollars don’t noticeably reduce your monthly payment but percentages do.

Overlays -

additional restrictions some lenders have in addition to standard mortgage guidelines. If your lender is telling you anything more is required than what’s posted above it’s because they have overlays which make it more difficult to get approved with them. Example - Veteran’s United will not take credit scores under 620 = OVERLAY

If you want a personalized answer for your unique situation call, text, or email me or visit my website below:

Kentucky Home Buyers: What Credit Score Do You Need?

Buying a home in Kentucky? Your credit score plays a crucial role in determining which mortgage loans you qualify for and how much you’ll pay in interest rates. Understanding the minimum credit score requirements for FHA, VA, USDA, and Conventional loans can help you prepare for homeownership and secure the best loan options.

While there's no single, simple answer, this guide will break down the minimum credit score requirements for various Kentucky mortgage options, empowering you to understand where you stand and how to achieve your homeownership goals. We'll cut through the confusion and give you the straight facts!

Why Your Credit Score Matters: More Than Just a Number

Think of your credit score as your financial reputation. Lenders use it to assess the risk of lending you money. A higher score signals lower risk, translating to better interest rates, more favorable loan terms, and potentially lower down payment requirements.

Here's the credit score impact on interest rates and your wallet (in general terms):

760-850: The Gold Standard! Expect the lowest interest rates and the most attractive loan options.

700-759: Excellent! You'll still qualify for very competitive rates and favorable terms.

640-699: Good. You'll likely be approved, but interest rates will be slightly higher.

620-639: Acceptable. This range is often the minimum for conventional loans, but be prepared for less favorable rates.

As the guide shows, aiming for a 740+ score can lead to best rates and closing costs on mortgage loans, especially Conventional Mortgage Loans,.

Let's explore the minimum credit score requirements for different Kentucky mortgage types:

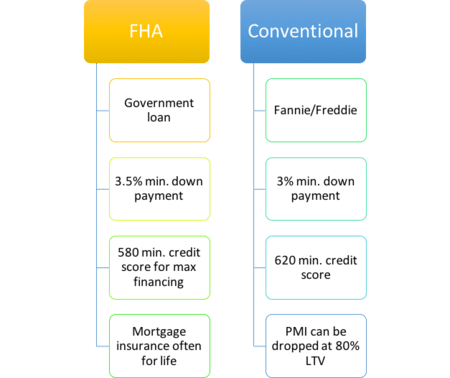

Conventional Loan

• At least 3%-5% down• Closing costs will vary on which rate you choose and the lender. Typically, the higher the rate, the lesser closing costs due to the lender giving you a lender credit back at closing for over par pricing. Also, called a no-closing costs option. You have to weigh the pros and cons to see if it makes sense to forgo the lower rate and lower monthly payment for the higher rate and less closing costs.

Fico scores needed start at 620, but most conventional lenders will want a higher score to qualify for the 3-5% minimum down payment requirements Most buyers using this loan have high credit scores (over 720) and at least 5% down.

The rates are a little higher compared to FHA, VA, or USDA loan but the mortgage insurance is not for life of loan and can be rolled off when you reach 80% equity position in home. Conventional loans require 4-7 years removed from Bankruptcy and foreclosure. Kentucky USDA Rural Housing Program If you meet income eligibility requirements and are looking to settle in a rural area, you might qualify for the KY USDA Rural Housing program. The program guarantees qualifying loans, reducing lenders’ risk and encouraging them to offer buyers 100% loans. That means Kentucky home buyers don’t have to put any money down, and even the “upfront fee” (a closing cost for this type of loan) can be rolled into the financing.

Fico scores usually wanted for this program center around 620 range, with most lenders wanting a 640 score so they can obtain an automated approval through GUS. GUS stands for the Guaranteed Underwriting system, and it will dictate your max loan pre-approval based on your income, credit scores, debt to income ratio and assets.

They also allow for a manual underwrite, which states that the max house payment ratios are set at 29% and 41% respectively of your income.

They loan requires no down payment, and the current mortgage insurance is 1% upfront, called a funding fee, and .35% annually for the monthly mi payment. Since they recently reduced their mi requirements, USDA is one of the best options out there for home buyers looking to buy in a rural area

A rural area typically will be any area outside the major cities of Louisville, Lexington, Paducah, Bowling Green, Richmond, Frankfort, and parts of Northern Kentucky. There is a map link below to see the qualifying areas.

There is also a max household income limits with most cutoff starting at 109,500 for a family of four, and up to $136,000 for a family of five or more.

The income limits change every spring, so make sure and check to see what updated income limits are. USDA requires 3 years removed from bankruptcy and foreclosure There is no max USDA loan limit.

Kentucky FHA Loan

FHA loans are good for home buyers with lower credit scores and no much down, or with down payment assistance grants. FHA will allow for grants, gifts, for their 3.5% minimum investment and will go down to a 580-credit score.

The current mortgage insurance requirements are kind of steep when compared to USDA, VA, but the rates are usually good so it can counteract the high mi premiums. As I tell borrowers, you will not have the loan for 30 years, so don’t worry too much about the mi premiums.

The mi premiums are for life of loan like USDA.

FHA requires 2 years removed from bankruptcy and 3 years removed from foreclosure.

Kentucky VA Loan

VA loans are for veterans and active-duty military personnel. The loan requires no down payment and no monthly mi premiums, saving you on the monthly payment. It does have an funding fee like USDA, but it is higher starting at 2% for first time use, and 3% for second time use. The funding fee is financed into the loan, so it is not something you have to pay upfront out of pocket.

VA loans can be made anywhere, unlike the USDA restrictions, and there is no income household limit and no max loan limits in Kentucky

Most VA lenders I work with will want a 580-credit score, even though VA says in their guidelines there is no minimum score, good luck finding a lender VA requires 2 years removed from bankruptcy or foreclosure Clear Caviars needed to for a VA loan.

Kentucky Down Payment Assistance

This type of loan is administered by KHC in the state of Kentucky. They typically have $10,000 down payment assistance year around, that is in the form of a second mortgage that you pay back over 10 years. Current terms are $10,000 over 10 years at 3.75%

Sometimes they will come to market with other down payment assistance and lower market rates to benefit lower income households with not a lot of money for down payment.

KHC offers FHA, VA, USDA, and Conventional loans with their minimum credit scores being set at 620 for all programs. The conventional loan requirements at KHC requires 660 credit score. The max debt to income ratios is set at 50% and 50% respectively.

FHA Loans – Best for First-Time Homebuyers with Low Credit

500-579 Credit Score – Requires 10% down payment 580+ Credit Score – Requires 3.5% down payment Flexible credit guidelines & lower down payments Easier approval for first-time buyers & those with past credit issues

VA Loans – Best for Veterans and Active Military

No official minimum credit score Most lenders require 580-620+ 0% down payment – No mortgage insurance required Best for veterans, active-duty military & eligible spouses

USDA Loans – Best for Rural & Suburban Homebuyers

Minimum 620 to 640+ Credit Score (for automatic approval through GUS ) Some lenders may approve below 640 with manual underwriting with a minimum score of 581 and above 0% down payment required Best for low-to-moderate-income homebuyers in rural areas Income limits and property locations restrictions

Conventional Loans – Best for Borrowers with Good Credit

Minimum 620+ Credit Score-Truthfully, if scores are 620 and less than 20% down payment look at going to the government loan programs like FHA, USDA and VA Higher scores (760+) qualify for better interest rates Down payment: 3%-5% or more Best for buyers with strong credit & stable income

Minimum 620+ Credit Score, Income limits and max dti is 50% usually used for the down payment and closing costs on a FHA, VA, USDA or Conventional loan with the $10k DAP assistance Offers down payment assistance for eligible buyers Best for first-time homebuyers needing financial help

Non-QM Loans – Alternative Financing for Unique Situations

Minimum 500-620 Credit Score (Varies by lender) Includes Bank Statement Loans, DSCR Loans, Asset-Based Loans Best for self-employed borrowers, real estate investors & those with non-traditional income sources

Why Choose Non-QM? These non-traditional loans are great for borrowers who don’t qualify for conventional or government-backed loans due to income verification challenges.

How Credit Scores Affect Mortgage Interest Rates

Your credit score doesn’t just determine loan eligibility—it also affects the interest rate you receive.

Here’s how credit scores impact mortgage rates (examples based on typical loan rates):

Credit Score

Estimated Interest Rate

Kentucky Mortgage Loan Options Available

760-850

Best Rate (Lowest Cost)

Kentucky Conventional, FHA, VA, USDA

700-759

Good Rate

Kentucky Conventional, FHA, VA, USDA

640-699

Higher Rate

Kentucky FHA, VA, USDA, Some Conventional

620-639

Even Higher Rate

Kentucky FHA, VA, USDA, Some Conventional

Below 620

Limited Options, Highest Rates

FHA, VA, USDA and (with higher down payment), Non-QM

Evo Mortgage Company NMLS# 1738461 Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

Freddie Mac and Fannie Mae Underwriting Guidelines for Mortgage Approval

These are called conventional because they must conform to the Freddie Mac and Fannie Mae standards set by the government, but they are not government insured. This poses a greater risk to lenders because they are not guaranteed repayment in the event the loan defaults; rather, they are forced to take a personal loss.

For these reasons, conventional mortgages are more difficult to obtain with stricter lending requirements in regards to credit score,down payment, debt to income ratio,mortgage insurance and previous bankruptcies or foreclosure.

Let's take a look at each subject below:👇

Credit Scores:

Fannie Mae and Freddie Mac Require a minimum 620 credit score.

You have three credit scores from Experian, Equifax, and Transunion, and they take the middle score, throwing out the high and low score. The higher the credit score the better pricing you will get on the rate and mortgage insurance along with your down payment.

Ideally for higher credit score buyers, say over 680, and with at least 3% down payment with a low debt to income ratio.

Down Payment:

Conventional mortgage loans require a minimum of 3% down payment. The more you put down, the better the rate, lower the mortgage insurance, and greater chances of getting approved.

If you put down 20%, then you will not have to pay mortgage insurance, or if you refinance an existing loan that has mortgage insurance, you can potentially get rid of the mortgage insurance if your equity position is less than 20% of the home's value.

Debt to Income:

Conventional Mortgage loans typically will not allow for a back-end ratio of over 45%. They're two ratios, the front-end and back-end ratio. The front-end ratio is a percentage of the total house payment of your total gross monthly income. The back-end ratio is the new total house payment along with the monthly payments on your credit report divided by your total gross monthly income.

For example, if you make $3,000 gross a month, your total backend ratio would me maxed out at 1,350 a month. So if you had $300 in monthly payments on the credit report, this would allow for a maximum house payment of $1,050.00

Mortgage Insurance:

Mortgage insurance is typically cheaper and less expensive on conventional mortgage loans. They're competing private mortgage insurance companies competing for the business with the names of MGIC, Radian, Essent, Genworth and Ugcorp.

Conversely, it is not like Government insured FHA, VA and USDA mortgage loans where all applicants get the same premiums regardless of credit score, down payment and debt to income ratio. Mortgage insurance is usually expressed as a monthly premium, with no upfront mortgage premiums like FHA, VA, and USDA government loan programs.

The higher the credit score, lower debt to income ratio and more nd can be removed once you reach 80% equity position in the home.

Bankruptcies and Foreclosure:

Bankruptcy (Chapter 7 or Chapter 11)

A four-year waiting period is required, measured from the discharge or dismissal date of the bankruptcy action.

Exceptions for Extenuating Circumstances

A two-year waiting period is permitted if extenuating circumstances can be documented, and is measured from the discharge or dismissal date of the bankruptcy action.

Bankruptcy (Chapter 13)

A distinction is made between Chapter 13 bankruptcies that were discharged and those that were dismissed. The waiting period required for Chapter 13 bankruptcy actions is measured as follows:

two years from the discharge date, or

four years from the dismissal date.

.Foreclosure

A seven-year waiting period is required, and is measured from the completion date of the foreclosure action as reported on the credit report or other foreclosure documents provided by the borrower.

Deed-in-Lieu of Foreclosure, Pre-foreclosure Sale, and Charge-Off of a Mortgage Account

These transaction types are completed as alternatives to foreclosure.

A deed-in-lieu of foreclosure is a transaction in which the deed to the real property is transferred back to the servicer. These are typically identified on the credit report through Remarks Codes such as “Forfeit deed-in-lieu of foreclosure.”

A pre-foreclosure sale or short sale is the sale of a property in lieu of a foreclosure resulting in a payoff of less than the total amount owed, which was pre-approved by the servicer. These are typically identified on the credit report through Remarks Codes such as “Settled for less than full balance.”

A charge-off of a mortgage account occurs when a creditor has determined that there is little (or no) likelihood that the mortgage debt will be collected. A charge-off is typically reported after an account reaches a certain delinquency status, and is identified on the credit report with a manner of payment (MOP) code of “9.”

A four-year waiting period is required from the completion date of the deed-in-lieu of foreclosure, pre-foreclosure sale, or charge-off as reported on the credit report or other documents provided by the borrower.

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916 http://www.nmlsconsumeraccess.org/

Fannie Mae is making a big change to its loan guidelines. On November 18, 2023, the maximum LTV ratio for two- to four-unit principal residence purchase and limited cash-out transactions will increase to 95%.

This means that borrowers can now put down as little as 5% on a two- to four-unit property, making it easier for them to buy a home or investment property.

Here's what you need to know:

This change applies to loans that are submitted or resubmitted to Fannie Mae's Desktop Underwriter (DU) on or after the weekend of November 18, 2023. 🗓

This change does not apply to high-balance mortgage loans or loans that are manually underwritten.

This is a great opportunity for those who are looking to buy a two- to four-unit property.

General Loan Limits for 2022 Mortgage Loans in Kentucky for FHA, VA, and Conventional Home Loans

Maximum Loan Limits for 2022 – Kentucky Conventional and Kentucky FHA Programs

Kentucky CONVENTIONAL Mortgage Loans Limits for 2022

The Federal Housing Finance Agency (FHFA) has issued the following maximum first mortgage loan limits that will apply to conventional loans for acquisition by Fannie Mae / Freddie Mac with a note date on and after January 1, 2022.

For calendar year 2022, the Department of Housing and Urban Development (HUD) announced the following maximum first mortgage loan limits that will apply to Kentucky FHA loans with case numbers assigned on and after January 1, 2022 through December 31, 2022:

2022 Kentucky FHA Loan Limits

Units

Kentucky FHA Loan Limits for 2022

One

$420,680

Two

$538,650

Three

$651,050

Four

$809,150

Please Note: These new limits apply to FHA loans with case numbers assigned on and after January 1, 2022 through December 31, 2022.

Although VA guaranteed loans do not have a maximum dollar amount, lenders who sell their VA loans in the secondary market must limit the size of those loans to the maximums prescribed by GNMA (Ginnie Mae) which are listed below.

Joel Lobb (NMLS#57916) Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com

If You are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

Kentucky Fannie Mae Loans versus Kentucky FHA Loans

Non Occupant Co-Borrower for Fannie Mae and FHA Loans.

The differences below:

Kentucky Fannie Mae Loans

Allowed on all Purchases up to 95% LTV

Allowed on all Refinances including Cash out

Does not have to be a Family Member

Kentucky FHA Loans

Limited to 75% LTV. LTV can be increased to max 96.5% LTV provided:

Non occupying borrower is not the seller in the transaction

Property is not a 2-4 unit property

Has to be a family member

Not allowed on Cash out Refinances

Non Occupant Co Borrowers must either be United State Citizens or have a Principal Residence in the United States.

Non arms Length / Identity of Interest for FHA and Fannie Mae Loans In KY

Fannie Mae Loans(non arms length)

Underwriter must confirm transaction is not a bail out

Gift of Equity is allowed

No additional restrictions apply

FHA loans (Identity of Interest)

Gift of Equity is allowed

LTV limited to 85% unless

Purchase is the principle residence of another Family Member

Borrower has been a tenant in property for 6 months predating the sales contract. A lease or other written evidence is needed to verify occupancy

Borrower is an employee of the Builder of the property

If a Family Member is providing secondary financing for the transaction, additional guidelines apply. See HUD 4000.1 II.A.4.(3) for additional guidelines.

Call/Text - 502-905-3708

.png "Minimum Credit Score Requirements for Kentucky Mortgage Loans")

Email -

Email - Website:

Website:  Address: 911 Barret Ave., Louisville, KY 40204

Address: 911 Barret Ave., Louisville, KY 40204

First-Time Home Buyers Welcome

First-Time Home Buyers Welcome