I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Kentucky First Time Home Buyer Programs For Home Mortgage Loans: 5 Things to Know For First Time Home Buyers in Ken...

Kentucky First Time Home Buyer Programs For Home Mortgage Loans: 5 Things to Know For First Time Home Buyers in Ken...: First Time Home Buyers in Kentucky 1. Do Mortgage Rates Change Daily? Just like the gas prices at the pump, mortgage rates can c...

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

How to Raise Your Credit Score Fast for Kentucky Mortgage Loan Approval for FHA, VA, USDA and KHC Mortgage loans.

How to Raise Your Credit Score Fast for Kentucky Mortgage Loan Approval for FHA, VA, USDA and KHC Mortgage loans.

Fico Score Tips to raise score

There are certain times when it pays to have the highest credit score possible. Maybe you’re about to refinance your mortgage. Or maybe you’re recovering from a bad credit history and you want to get approved for a credit card.

It’s always good to have a healthy score, of course.

But if you’re in a place where you really need to up that score as soon as possible, there are a few under-the-radar ways to speed up the process.

How to Raise Your Credit Score Fast

- Find Out When Your Issuer Reports Payment History

- Pay Down Debt Strategically

- Pay Twice a Month

- Raise Your Credit Limits

- Mix It Up

How long will it take to increase your credit score? It won’t happen instantly, but if you follow the steps in this article your credit score will begin to go up within a couple of months. Let’s get started.

1. Find Out When Your Issuer Reports Payment History

Call your credit card issuer and ask when your balance gets reported to the credit bureaus. That day is often the closing date (or the last day of the billing cycle) on your account. Note that this is different from the “due date” on your statement.

There’s something called a “credit utilization ratio.” It’s the amount of credit you’ve used compared to the amount of credit you have available. You have a ratio for your overall credit card use as well as for each credit card.

It’s best to have a ratio — overall and on individual cards — of less than 30%. But here’s an insider tip: To boost your score more quickly, keep your credit utilization ratio under 10%.

Here’s an example of how the utilization ratio is calculated:

Let’s say you have two credit cards. Card A has a $6,000 credit limit and a $2,500 balance. Card B has a $10,000 limit and you have a $1,000 balance on it.

This is your utilization ratio per card:

Card A = 42% (2,500/6,000 = .416, or 42%), which is too high.

Card B = 10% (1,000/10,000 = .100, or 10%), which is awesome.

This is your overall credit utilization ratio: 22% (3,500/16,000 = 0.218), which is very good.

But here’s the problem: Even if you pay your balance off every month (and you should), if your payment is received after the reporting date, your reported balance could be high — and that negatively impacts your score because your ratio appears inflated.

So pay your bill just before the closing date. That way, your reported balance will be low or even zero. The FICO method will then use the lower balance to calculate your score. This lowers your utilization ratio and boosts your score.

2. Pay Down Debt Strategically

Okay, let’s build on what you just learned about utilization ratios.

In the above example, you have balances on more than one card. Note that Card A has a 42% ratio, which is high, and Card B has a wonderfully low 10% ratio.

Since the FICO score also looks at each card’s ratio, you can bump up your score by paying down the card with the higher balance. In the example above, pay down the balance on Card A to about $1,500 and your new ratio for Card A is 25% (1,500/6,000 = .25). Much better!

3. Pay Twice a Month

Let’s say you’ve had a rough couple of months with your finances. Maybe you needed to rebuild your deck (raising my hand) or get a new fridge. If you put big items on a credit card to get the rewards, it can temporarily throw your utilization ratio (and your credit score) out of whack.

You know that call you made to get the closing date? Make a payment two weeks before the closing date and then make another payment just before the closing date. This, of course, assumes you have the money to pay off your big expense by the end of the month.

Take care not to use a credit card for a big bill if you plan to carry a balance. The compound interest will create an ugly pile of debt pretty quickly. Credit cards should never be used for long-term loans unless you have a card with a zero percent introductory APR on purchases. Even then, you have to be mindful of the balance on the card and make sure you can pay the bill off before the intro period ends.

4. Raise Your Credit Limits

If you tend to have problems with overspending, don’t try this.

The goal is to raise your credit limit on one or more cards so that your utilization ratio goes down. But again, this only works out in your favor if you don’t feel compelled to use the newly available credit.

I also don’t recommend trying this if you have missed payments with the issuer or have a downward-trending score. The issuer could see your request for a credit limit increase as a sign that you’re about to have a financial crisis and need the extra credit. I’ve actually seen this result in a decrease in credit limits. So be sure your situation looks stable before you ask for an increase.

That said, as long as you’ve been a great customer and your score is reasonably healthy, this is a good strategy to try.

All you have to do is call your credit card company and ask for an increase to your credit limit. Have an amount in mind before you call. Make that amount a little higher than what you want in case they feel the need to negotiate.

Remember the example in #1? Card A has a $6,000 limit and you have a $2,500 balance on it. That’s a 42% utilization ratio (2,500/6,000 = .416, or 42%).

If your limit goes up to $8,500, then your new ratio is a more pleasing 29% (2,500/8,500 = .294, or 29%). The higher the limit, the lower your ratio will be and this helps your score.

5. Mix It Up

A few years back, I realized I didn’t have much of a mix of credit. I have credit cards with low utilization ratios and a mortgage, but I hadn’t paid off an installment loan for a couple of decades.

I wanted to raise my score a nudge, so I decided to get a car loan at a very low rate. I spent a year paying it off just to get a mix in my credit. At first, my score went down a little, but after about six months, my score started increasing. Your credit mix is only 10% of your FICO score, but sometimes that little bit can bump you up from good credit to excellent credit.

I wasn’t planning on applying for credit within the next six months, so my approach was fine. But if you’re refinancing your mortgage (or planning something else really big) and you want a quick boost, don’t use this strategy. This is a good one for a long-term approach.

Bottom Line

When you want to boost your credit score, there are two basic rules you have to follow:

First, keep your credit card balances low.

Second, pay your bills on time (and in full). Do these two things and then toss in one or more of the sneaky ways above to give your score a kickstart.

And remember — you do not have to carry a balance to build a good score. If you do that, you’re on a slippery slope to debt.

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

fax: 502-327-9119

email: kentuckyloan@gmail.com

email: kentuckyloan@gmail.com

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Kentucky First Time Home Buyer Programs

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Tips to keep your Kentucky Mortgage Loan Pre-Approval Valid until closing

10 Tips for Mortgage Loan Applicants Not to After Pre-Approval for a KY Mortgage

1. Don’t change jobs or become self-employed.

2. Don’t buy a car, truck, van, boat or motorhome unless you plan to live in it.

3. Don’t use your credit cards or let your payments fall behind.

4. Don’t spend the money you have saved for your down payment.

5. Don’t buy furniture before you buy your house.

6. Don’t originate any new inquiries on your credit report.

7. Don’t make any LARGE or CASH deposits into your bank account.

8. Don’t change bank accounts.

9. Don’t co-sign for anyone.

10. Don’t purchase anything until after the closing.

Kentucky Mortgage Pre-Approval Checklist of Items Needed for Approval Letter

- Bank Statements - Last 2 Months – All bank statements for all accounts from the last 2 months. Include all numbered pages of all bank statements!

- Driver's License – Legible state-issued driver's license

- Evidence of Insurance – For all properties owned

- Federal Tax Returns - Last 2 Years – Last 2 years of federal tax returns to prove income, include all schedules

- HOA statement (if applicable) – Most current statement

- Loan Application (1003) – Please complete all fields

- Mortgage Statement(s) – Most recent for all properties owned

- Pay Stubs - Received in Last 30 Days – Last 30 days of pay stubs to prove income

- Social Security Card – Legible social security card to prove social security number

- W-2s - Last 2 Years – Last 2 years of W-2s to prove income

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

fax: 502-327-9119

email: kentuckyloan@gmail.com

email: kentuckyloan@gmail.com

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Kentucky USDA Mortgage Loan Qualifying Guidelines

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Kentucky USDA Rural Housing Mortgage Lender: USDA Extends Foreclosure and Eviction Moratorium, ...

Kentucky USDA Rural Housing Mortgage Lender: USDA Extends Foreclosure and Eviction Moratorium, ...: Moratorium and relief options extended through February 28, 2021 Foreclosure and Eviction Moratorium Extension: The U.S. Department of Agr...

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

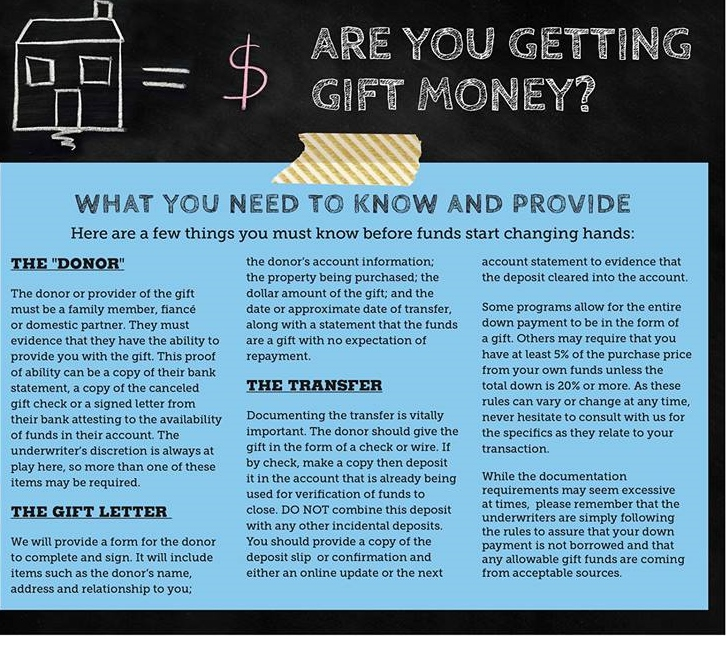

Can I get a Gift for A Down payment on a Kentucky Mortgage Loan?

For many Kentucky first time buyers, saving for a down payment is one of the most challenging steps in fulfilling their dream of purchasing a home. Oftentimes, they know they can afford their potential monthly mortgages (which could be less or equal their current rents), but the upfront costs of buying, such as down payment and closing costs, may be too much for them to pay.

This is why it's possible to get a little help in the form of a down payment gift from a family member or relative, close friend, or even a charitable organization. And it’s actually becoming more popular, especially among millennials. In the National Association of REALTORS® 2020 Generational Trends Report, 13 percent of home buyers (and 27 percent for ages 22 to 29) indicated their source of down payment to be a gift from their relative or friend.

So if you’re lucky enough to find down payment fund as one of your gifts under the Christmas tree this year (or maybe you’re the one who wants to give it), it may not be as simple as opening your cash gift (or handing someone a wad of cash) and going straight to the lender to use it to buy a home.

Down payment gift funds, whether you’re giving or receiving it, are closely regulated by lenders and must meet certain requirements. Here are certain rules that the gift giver and recipient should know to avoid trouble down the road.

While we may automatically consider a family member, like parents or siblings, when thinking about who can give a mortgage down payment gift, there are other entities who could also be eligible gift sources. But because cash can come with strings attached, and lenders want to make sure that the gift money is nothing but a gift (which will be discussed later on), there are restrictions on who can give money (or who you can give money to) to help purchase a home.

For conventional loans

If you are getting a loan through Fannie Mae or Freddie Mac, gifts can only be from a family member or relative. This may be your spouse, child, siblings, parents, grandparents, or anyone related by blood, marriage, adoption, or legal guardianship. Soon-to-be family members such as your domestic partner, fiancé, or even future in-laws are also eligible to give funds for a down payment.

For FHA loans

The Federal Housing Administration (FHA) has its own set of rules when it comes to giving or receiving down payment gifts, although they offer a broader eligibility range. If you are getting an FHA loan, you can receive down payment funds from family members, friends who have a clearly defined and documented interest in your life, employers, labor unions, government agencies, and even charitable organizations.

For USDA and VA home loans

VA loans (backed by the U.S. Department of Veterans Affairs) and USDA mortgages (given by the U.S. Department of Agriculture)may have fewer restrictions, but the down payment gift funds cannot come from anyone who would benefit from the proceeds of the purchase, such as the seller, developer, builder, your real estate agent, and some other entity.

There are no limits on the amount of money someone can give you for a down payment or to cover closing costs. However, rules still apply depending on the type of loan and property you're purchasing. Some types of loans may need you to contribute a certain amount of the down. The key is to check with your lender for the latest regulations on how much you can really use.

Likewise, there can be tax implications on the person giving the gift funds. They may be liable if the amount exceeds the gift tax exclusion limit. As of 2020, for instance, any individual can give funds up to $15,000 without a tax penalty. On the other hand, parents who are married and are filing jointly can give up to $30,000 per child for a mortgage down payment (or any other purpose), without incurring the gift tax. For a down payment gift that exceeds the said amounts, the donor must file a gift tax return to disclose the gift.

You need to confirm the relationship between you and the giver and provide the right paperwork.

If you're fortunate enough to have a family member or any eligible entity who can give you funds towards your home’s down payment, you’ll need to confirm your relationship with the gift-giver and provide your mortgage underwriter more information about where the funds came from.

For lenders to confirm that the new money isn’t a loan, you’ll need these things:

1. A down payment gift letter - If your lender has a template letter for this purpose, you will need to send it to the funds’ donor. If there isn’t a template, you might want to ask what information should be included so you can draft your own.

The letter typically includes details about the gift-giver, such as the name, address, contact phone, relationship to the borrower, and address of the property to be purchased. The date when the gift was transferred and the amount of funds given to the borrower must also be indicated. The donor should also write a sentence explaining that the fund is a gift and that there isn’t any expectation of repayment. The letter must be signed by both the gift-giver and the borrower.

2. The gift-giver’s bank statements - This is to show they have the funds to give the buyer as much money as promised.

3. A bank slip from the buyer’s account - This is to indicate when the money was transferred, to verify that the cash is from a legitimate source and that the borrower has an appropriate relationship with the donor, and to confirm the information provided in the letter.

Remember: you can't pay back the gift.

Down payment gift funds need to be just like that—a gift and not a loan that is expected to be paid. You need to make it clear with your mortgage lender that the money you received was entirely gifted and not something that you need to pay back eventually, because by then it will be considered mortgage or loan fraud. Besides, it can also put your loan qualification at risk since your debt-to-income ratio will be factored when you get a mortgage.

Try to make it a “seasoned” gift money.

It might make more sense to try and make your gift money “seasoned”, especially if you know that someone is going to help you buy a home (often in the case of parents or other relatives). Lenders refer to it as seasoned money when it has been sitting in your bank account for some time, at least for two months. When the gifted money is given in advance, you often don't have to worry about writing gift letter documentation.

Bottom Line

Down payment gift funds make it easier for first-time home buyers to afford a home. If you anticipate accepting help, remember to consider the rules above so you can accept such a gift in a proper manner. Be upfront with your mortgage lender if you plan on using gift funds for the down payment. Don't forget to also talk to the individual or entities who are planning to give you money about the tax implications and other considerations.

--

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

fax: 502-327-9119

email: kentuckyloan@gmail.com

email: kentuckyloan@gmail.com

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Subscribe to:

Posts (Atom)