I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Showing posts with label Credit Score First Time Home Buyer Louisville Kentucky KHC. Show all posts

Showing posts with label Credit Score First Time Home Buyer Louisville Kentucky KHC. Show all posts

100% Financing Zero Down Payment Kentucky Mortgage Home Loans for Kentucky First time Home Buyers: Common Kentucky Mortgage Myths Busted!My credit sc...

100% Financing Zero Down Payment Kentucky Mortgage Home Loans for Kentucky First time Home Buyers: Common Kentucky Mortgage Myths Busted!My credit sc...: Common Kentucky Mortgage Myths Busted! My credit score or fico score is too low: Most people’s credit scores are better than they think. A...

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Homeownership doesn’t mean you need perfect credit. Some people can buy a home with a 620 credit score.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

About FICO® Scores

About FICO® Scores

What is a credit score?

What is a credit score?

A credit score is a number that summarizes your credit risk to lenders, or the likelihood that you’ll pay the lender back the amount you borrowed plus interest. The score is based on a snapshot of your credit report(s) at one of the three major credit bureaus—Equifax®, Experian®, and TransUnion®—at a particular point in time, and helps lenders evaluate your credit risk. Your credit score can influence the credit that’s available to you and the terms, such as interest rate, that lenders offer you.

What is a credit bureau?

A credit bureau, also known as a consumer reporting agency, collects and stores individual credit information and provides it to creditors so they can make decisions on granting loans and other credit activities. Typical clients include banks, mortgage lenders, and credit card issuers. The three largest credit bureaus in the U.S. are Equifax®, Experian®, and TransUnion®.

What are FICO® Scores?

FICO® Scores are the most widely used credit scores and are used in over 90% of U.S. lending decisions. Your FICO® Scores (you have more than one) are based on the data generated from your credit reports at the three major credit bureaus, Experian®, TransUnion® and Equifax®. Each of your FICO® Scores is a three-digit number summarizing your credit risk, that predicts how likely you are to pay back your credit obligations as agreed.

What it the highest credit score?

Most credit scoring models follow a credit score range of 300 to 850 with that 850 being the highest score you can have. However, there can be other ranges for different models, some of which are customized for a particular industry (credit card, auto lending, or insurance for example). While the majority follow the 300 to 850 range, there are some scores (e.g., FICO® Bankcard Score) that range from 250 to 900 and others that may use other score ranges. For more information on the different scoring models, view Understanding the difference between credit scores.

Why do FICO® Scores fluctuate?

There are many reasons why your score may change. The information on your credit report changes each time lenders report new activity to the credit bureau. So, as the information in your credit report at that bureau changes, your FICO® Scores may also change. Keep in mind that certain events such as late payments or bankruptcy can lower your FICO® Scores quickly.

FICO® Scores consider five main categories of information in your credit report.

- Your payment history

- The amount of money you currently owe

- The length of your credit history

- New credit accounts

- Types of credit in use

What are the minimum requirements to produce a FICO® Score?

In order for a FICO® Score to be calculated, a credit report must contain these minimum requirements:

- At least one account that has been open for six months or more.

- At least one account that has been reported to the credit reporting agency within the past six months.

- No indication of deceased on the credit report (Please note: if you share an account with another person and the other account holder is reported deceased, it is important to check your credit report to make sure you are not impacted).

Does a FICO® Score alone determine whether I get credit?

No. Most lenders use a number of factors to make credit decisions, including a FICO® Score. Lenders may look at information such as the amount of debt you are able to handle reasonably given your income, your employment history, and your credit history. Based on their review of this information, as well as their specific underwriting policies, lenders may extend credit to you even with a low FICO® Score, or decline your request for credit even with a high FICO® Score.

How long will negative information remain on my credit reports?

It depends on the type of negative information. Here’s the basic breakdown of how long different types of negative information will remain on your credit reports:

- Late payments: 7 years from the original delinquency date.

- Chapter 7 bankruptcies: 10 years from the filing date.

- Chapter 13 bankruptcies: 7 years from the filing date.

- Collection accounts: 7 years from the original delinquency date of the account

- Public Record: Generally 7 years

Keep in Mind: For all of these negative items, the older they are the less impact they will have on your FICO® Scores. For example, a collection that is 5 years old will hurt much less than a collection that is 5 months old.

Are FICO® Scores unfair to minorities?

No. FICO® Scores do not consider your gender, race, nationality or marital status. In fact, the Equal Credit Opportunity Act prohibits lenders from considering this type of information when issuing credit. Independent research has shown that FICO® Scores are not unfair to minorities or people with little credit history. FICO® Scores have proven to be an accurate and consistent measure of repayment for all people who have some credit history. In other words, at a given FICO® Score, non-minority and minority applicants are equally likely to pay as agreed.

How are FICO® Scores calculated for married couples?

Married couples don’t share joint FICO® Scores; each person has their own individual credit report, which is used to calculate FICO® Scores, and isn’t impacted by their spouse’s credit history. However, married couples should be mindful of the potential impact of opening joint credit accounts. For example, if you get a new credit card in both spouses’ names, and there is a late payment on that account, the late payment will impact both individuals’ FICO® Scores.

How can I access my credit report?

By federal law, you are entitled to one free credit report every 12 months from each credit reporting company, TransUnion®, Equifax®, and Experian®. Find them at annualcreditreport.com. Take advantage of this service annually to ensure the information on your credit report is current and accurate.

Impacts to FICO® Scores

Will closing a credit card account impact my FICO® Score?

It is possible that closing a credit account may have a negative impact depending on a few factors. FICO® Scores may consider your “credit utilization rate”, which looks at your total used credit in relation to your total available credit. Essentially, it measures how much of your available credit you are actually using. The more of your credit that you use, the higher your utilization rate and high credit utilization rates may negatively impact your FICO® Score. Before you close any credit card account, Wells Fargo recommends that you should first consider whether you really need to close the account or if your real intention is just to stop using that credit card. If you really just want to stop using that card, it may make sense if you stop using the card and put it somewhere for safe keeping in case of an emergency. It’s also important to note that length of your credit history accounts for 15% of your FICO® Score calculation. Therefore, having credit card accounts that are open and in good standing for a long time may affect your FICO® Score.

How does refinancing impact my FICO® Score?

Refinancing and loan modifications may affect your FICO® Scores in a few areas. How much these affect the score depends on whether it’s reported to the consumer reporting agencies as the same loan with changes or as an entirely new loan. There are many reasons why a score may change. FICO® Scores are calculated using many different pieces of credit data in your credit report. This data is grouped into five categories: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%) and credit mix (10%). If a refinanced loan or modified loan is reported as the same loan with changes, two pieces of information associated with the loan modification may affect your score: the new credit inquiry and changes to the amounts owed. If a refinanced loan or modified loan is reported as a “new” loan, your score could still be affected by the new credit inquiry and an increase in amounts owed,— along with the additional impact of a new “open date” which may affect the credit history category. In the end, a new or recent open date typically indicates that it is a new credit obligation and, as a result, may impact the score more than if the terms of the existing loan are simply changed.

How do FICO® Scores consider loan shopping?

In general, if you are “loan shopping” - meaning that you are applying for the same type of loan with similar amounts with multiple lenders in a short period of time - your FICO® Score will consider your “shopping” as a single credit inquiry on your score if the shopping occurs within a short time period (30 to 45 day) depending on which FICO® Score version is used by your lenders.

What are the different categories of late payments and do they impact FICO® Scores?

A history of payments is the largest factor in FICO® Scores. FICO® Scores consider late payments in these general areas; how recent the late payments are, how severe the late payments are, and how frequently the late payments occur. So this means that a recent late payment could be more damaging to a FICO® Score than a number of late payments that happened a long time ago. Late payments are listed on credit reports by how late the payments are. Typically, creditors report late payments in one of these categories: 30-days late, 60-days late, 90-days late, 120-days late, 150-days late, or charge off (written off as a loss because of severe delinquency). Of course a 90-day late is worse than a 30-day late, but the important thing to understand is that people who continually pay their bills on time tend to appear less risky to lenders. However, for people who continue not to pay debt, and their creditor either charges it off or sends it to a collection agency, it is considered a significant event with regard to a score and will likely have a severe negative impact.

How does a bankruptcy impact my FICO® Score?

A bankruptcy is considered a very negative event by FICO® Scores. As long as the bankruptcy is listed on your credit report, it will be factored into your scores. How much of an impact it will have on your score will depend on your entire credit profile. As the bankruptcy item ages, its impact on a FICO® Score gradually decreases. Typically, here is how long you can expect bankruptcies to remain on your credit reports (from the date filed):

- Chapter 11 and 7 bankruptcies up to 10 years.

- Completed Chapter 13 bankruptcies up to 7 years.

These dates and time periods refer to the public record item associated with filing for bankruptcy. All of the individual accounts included in the bankruptcy should be removed from your credit reports after 7 years.

How do public records and judgments impact FICO® Scores?

Public records are legal documents created and maintained by Federal and local governments, which are usually accessible to the public. Some public records, such as divorces, are not considered by FICO® Scores, but adverse public records, which include bankruptcies, are considered by FICO® Scores. FICO® Scores may be affected by the mere presence of an adverse public record, whether paid or not. Adverse public records will have less effect on a FICO® Score as time passes, but they can remain in your credit reports for up to ten years based on what type of public record it is.

What are inquiries and how do they impact FICO® Scores?

Inquiries may or may not affect FICO® Scores. Credit inquiries are classified as either “hard inquiries” or “soft inquiries”—only hard inquiries have an effect on FICO® Scores.

Soft inquiries are all credit inquiries where your credit is NOT being reviewed by a prospective lender. FICO® Scores do not take into account any involuntary (soft) inquiries made by businesses with which you did not apply for credit, inquiries from employers, or your own requests to see your credit report. Soft inquiries also include inquiries from businesses checking your credit to offer you goods or services (such as promotional offers by credit card companies) and credit checks from businesses with which you already have a credit account. If you are receiving FICO® Scores for free from a business with which you already have a credit account, there is no additional inquiry made on your credit report. FICO® Scores take into account only voluntary (hard) inquiries that result from your application for credit. Hard inquiries include credit checks when you’ve applied for an auto loan, mortgage, credit card or other types of loans. Each of these types of credit checks count as a single inquiry. Inquiries may have a greater impact if you have few accounts or a short credit history. Large numbers of inquiries also mean greater risk.

How does applying for new credit impact my FICO® Score?

Applying for new credit only accounts for about 10% of a FICO® Score. Exactly how much applying for new credit affects your score depends on your overall credit profile and what else is already in your credit reports. For example, applying for new credit may have a greater impact on your FICO® Scores if you only have a few accounts or a short credit history. That said, there are definitely a few things to be aware of depending on the type of credit you are applying for. When you apply for credit, a credit check or “inquiry” can be requested to check your credit standing.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

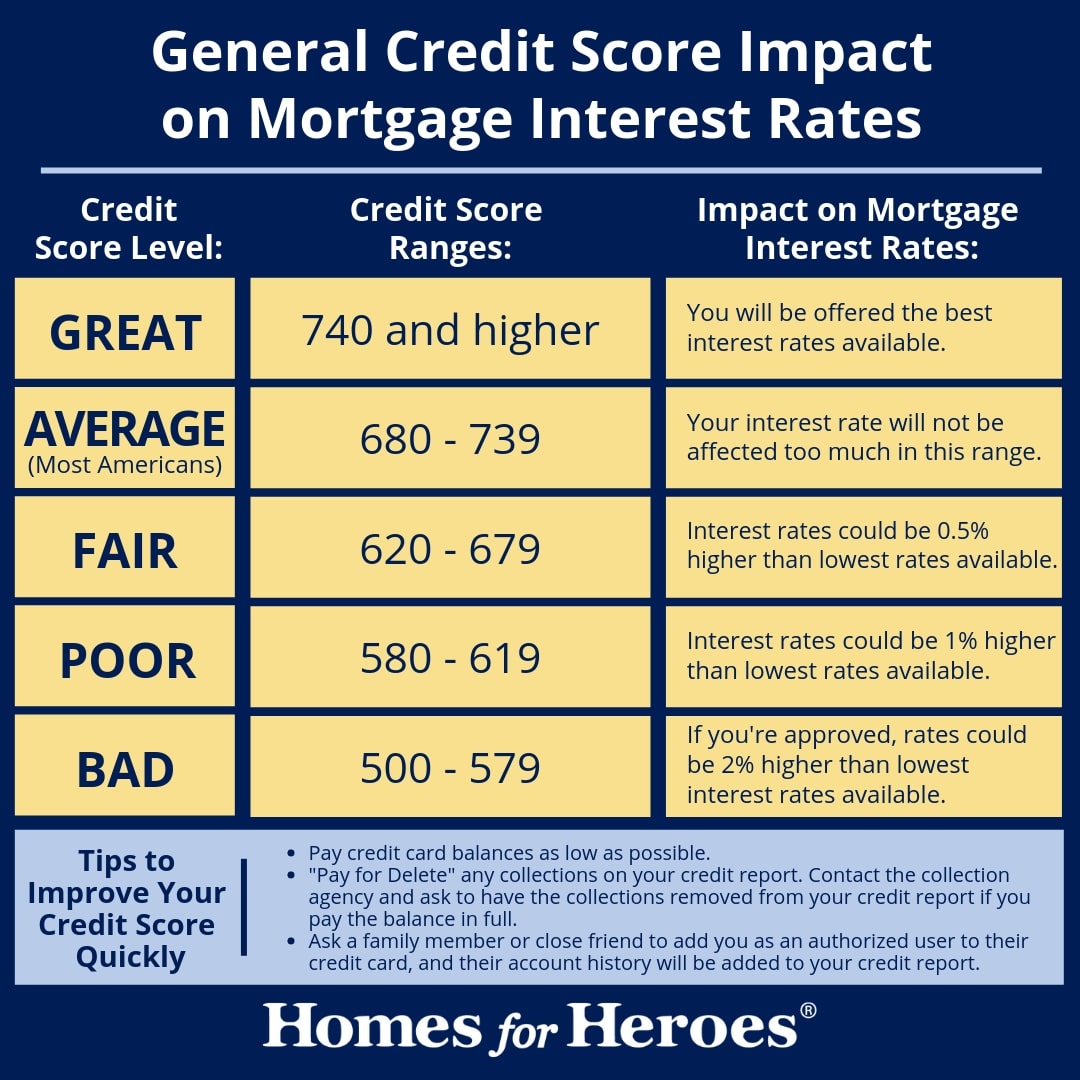

Credit Scores FHA Loans Louisville Kentucky KHC First Time Home Buyer Credit Score

What is the minimum Credit Score Needed to Buy a House and get a Kentucky Mortgage Loan?

5 POPULAR PROGRAMS THAT KENTUCKY HOME BUYERS USE TO PURCHASE THEIR FIRST HOME.

• At least 3%-5% down• Closing costs will vary on which rate you choose and the lender. Typically the higher the rate, the lesser closing costs due to the lender giving you a lender credit back at closing for over par pricing. Also, called a no-closing costs option. You have to weigh the pros and cons to see if it makes sense to forgo the lower rate and lower monthly payment for the higher rate and less closing costs.

Fico scores needed start at 620, but most conventional lenders will want a higher score to qualify for the 3-5% minimum down payment requirements Most buyers using this loan have high credit scores (over 720) and at least 5% down.

The rates are a little higher compared to FHA, VA, or USDA loan but the mortgage insurance is not for life of loan and can be rolled off when you reach 80% equity position in home.Conventional loans require 4-7 years removed from Bankruptcy and foreclosure.Max Conventional loan limits are set at $510,400 for 2020 in Kentucky

If you meet income eligibility requirements and are looking to settle in a rural area, you might qualify for the KY USDA Rural Housing program. The program guarantees qualifying loans, reducing lenders’ risk and encouraging them to offer buyers 100% loans. That means Kentucky home buyers don’t have to put any money down, and even the “upfront fee” (a closing cost for this type of loan) can be rolled into the financing.

Fico scores usually wanted for this program center around 620 range, with most lenders wanting a 640 score so they can obtain an automated approval through GUS. GUS stands for the Guaranteed Underwriting system, and it will dictate your max loan pre-approval based on your income, credit scores, debt to income ratio and assets.

They also allow for a manual underwrite, which states that the max house payment ratios are set at 29% and 41% respectively of your income.

They loan requires no down payment, and the current mortgage insurance is 1% upfront, called a funding fee, and .35% annually for the monthly mi payment. Since they recently reduced their mi requirements, USDA is one of the best options out there for home buyers looking to buy in an rural area

A rural area typically will be any area outside the major cities of Louisville, Lexington, Paducah, Bowling Green, Richmond, Frankfort, and parts of Northern Kentucky .There is a map link below to see the qualifying areas.

Thee is also a max household income limits with most cutoff starting at $86,400 for a family of four, and up to $115,000 for a family of five or more.USDA requires 3 years removed from bankruptcy and foreclosureThere is no max USDA loan limit.

FHA loans are good for home buyers with lower credit scores and no much down, or with down payment assistance grants. FHA will allow for grants, gifts, for their 3.5% minimum investment and will go down to a 580 credit score.

The current mortgage insurance requirements are kinda steep when compared to USDA, VA , but the rates are usually good so it can counteracts the high mi premiums. As I tell borrowers, you will not have the loan for 30 years, so don’t worry too much about the mi premiums.

THe mi premiums are for life of loan like USDA.

FHA requires 2 years removed from bankruptcy and 3 years removed from foreclosure.Maximum FHA loan limits in Kentucky are set around $331,600 and below.

VA loans are for veterans and active duty military personnel. The loan requires no down payment and no monthly mi premiums, saving you on the monthly payment. It does have an funding fee like USDA, but it is higher starting at 2% for first time use, and 3% for second time use. The funding fee is financed into the loan, so it is not something you have to pay upfront out of pocket.

VA loans can be made anywhere, unlike the USDA restrictions, and there is no income household limit and no max loan limits in Kentucky

Most VA lenders I work with will want a 580 credit score, even though VA says in their guidelines there is no minimum score, good luck finding a lender

VA requires 2 years removed from bankruptcy or foreclosure

VA requires 2 years removed from bankruptcy or foreclosure

This type of loan is administered by KHC in the state of Kentucky. They typically have $4500 to $6000 down payment assistance year around, that is in the form of a second mortgage that you pay back over 10 years.

Sometimes they will come to market with other down payment assistance and lower market rates to benefit lower income households with not a lot of money for down payment.KHC offers FHA, VA, USDA, and Conventional loans with their minimum credit scores being set at 620 for all programs. The conventional loan requirements at KHC requires 660 credit score.

The max debt to income ratios are set at 40% and 50% respectively.

Joel Lobb (NMLS#57916)

Senior Loan Officer

Text/call 502-905-3708

Senior Loan Officer

Text/call 502-905-3708

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant

Equal Opportunity Lender. NMLS#57916

http://www.

Estimated Sale Price: $110,000

• Rate - 3.75%

• APR - 4.854%

• Down payment - $3850.00

• Principal & Interest - $500.20

• Insurance (estimated) - $75

• Taxes - $47.92

• PMI - $74.56

TOTAL PAYMENT INCLUDING

TAXES + INSURANCE:

$697.68 a month!

*Rates effective 01/16/2020, based on 740 FICO score and subject to change. ARP may vary. Loan terms are fixed rate 30 year loans and payment will not rise over the life of the loan. Not all applicants will qualify for advertised terms and conditions, must meet underwriting guidelines and are subject to credit review and approval. This does not constitute a commitment to lend. The disclosed rates, payments, homeowners insurance and mortgage insurance are estimates and may vary according to lender guidelines. Property taxes based on current assessed value with homestead and mortgage exemptions in place. Equal Housing Lender.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant

Equal Opportunity Lender. NMLS#57916

http://www.

Estimated Sale Price: $110,000

• Rate - 3.75%

• APR - 4.854%

• Down payment - $3850.00

• Principal & Interest - $500.20

• Insurance (estimated) - $75

• Taxes - $47.92

• PMI - $74.56

• Rate - 3.75%

• APR - 4.854%

• Down payment - $3850.00

• Principal & Interest - $500.20

• Insurance (estimated) - $75

• Taxes - $47.92

• PMI - $74.56

TOTAL PAYMENT INCLUDING

TAXES + INSURANCE:

$697.68 a month!

TAXES + INSURANCE:

$697.68 a month!

*Rates effective 01/16/2020, based on 740 FICO score and subject to change. ARP may vary. Loan terms are fixed rate 30 year loans and payment will not rise over the life of the loan. Not all applicants will qualify for advertised terms and conditions, must meet underwriting guidelines and are subject to credit review and approval. This does not constitute a commitment to lend. The disclosed rates, payments, homeowners insurance and mortgage insurance are estimates and may vary according to lender guidelines. Property taxes based on current assessed value with homestead and mortgage exemptions in place. Equal Housing Lender.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Credit Score Information for KY Home buyers

Credit Score Information for KY Home buyers

When it comes to your credit score, believing the wrong information could literally cost you.

What Types of Credit Pulls Really Harm My Score?

Research shows that people who apply for new credit too frequently indicate a higher credit risk. For this reason, scoring models like FICO® factor in the number of inquiries on your credit reports, which leads some people to incorrectly believe that having your credit pulled automatically damages your score. That is not exactly the case — and here’s the scoop:

- It is true that some inquiries can potentially harm your credit. Hard inquiries, like a lender pulling your credit report, could affect your score. But soft inquiries, like checking your own credit score, will not.For example: If you apply for numerous credit cards, then it will probably negatively impact your credit score. But if you have multiple credit pulls from mortgage companies, student loan providers, or auto lenders because you are rate shopping, then there might be a less substantial impact on your score because rate shopping doesn’t indicate an elevated credit risk — as long as multiple inquires occur within a small window of time (usually between 14 and 45 days).

Should I Close Paid-Off Credit Cards?

Another common credit myth is that paid-off credit card accounts should be closed. According to FICO, credit card accounts should never be closed for the sole purpose of raising a credit score. Closing a zero-balance credit card account often has the unintended effect of raising your revolving utilization ratio — or your available credit relative to your outstanding account balances.

When you close an unused account, the available credit limit is no longer factored into your revolving utilization. If you carry an outstanding balance on any other credit cards, closing a zero-balance account could result in a higher overall revolving utilization ratio, which in turn could cause your credit score to drop.

Is 30% the Magic Number for Credit Card Utilization?

When it comes to credit card utilization, a lower percentage is generally better. One credit scoring myth that has confused a lot of consumers over the years is the idea that 30% is the magic number for credit card utilization. According to FICO, that isn’t true.

If you want to have a healthy credit score, aim to pay off your credit card balances in full each month. Pay by the statement closing date, and you should see that the account balance on your credit report is reflected as zero — and note that a zero balance can lead to lower revolving credit utilization (and generally a better credit score).

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Credit Score Information for Kentucky Mortgage Loan Approvals

Credit Score Knowledge Quiz Information for Kentucky Mortgage Loans

Credit scores are taking an even more important role in qualifying for a Kentucky FHA, VA, Rural Housing and Fannie Mae mortgage today, which makes it vital to maintain a good credit history. See how much you know about credit scores with our Credit Knowledge Quiz and what you need to focus on to better your score.

Question 01

A credit score is:

- a. A three-digit number summarizing the state of your credit

- b. An alphabetical score grading your creditworthiness

- c. A numerical score reporting how much money you owe

Question 02

What is the number-one contributing factor to a good credit score?

- a. Length of credit history

- b. Amounts you owe

- c. Payment history

Question 03

Does each consumer have just ONE generic credit score?

- a. Yes

- b. No

- c. Don't Know

Question 04

Your credit score affects?

- a. Whether you can get a loan

- b. Your interest rate

- c. Both A and B

Question 05

Who collects the information on which credit scores are most frequently based?

- a. FICO and VantageScore

- b. Three main credit bureaus – Experian, Equifax, and TransUnion

- c. Individual lenders

- d. Federal government

Question 06

Lenders look at credit scores when deciding whether to extend which type of credit?

- a. Credit cards

- b. Mortgages

- c. Loans

- d. All of the above

Question 07

How important is it to check the accuracy of your credit reports at the three main credit bureaus?

- a. Very Important

- b. Somewhat Important

- c. Not Very Important

- d. No Big Deal

Question 08

Which of the following actions helps a consumer raise a low score or maintain a high one?

- a. Make all loan payments on time

- b. Avoid opening several credit card accounts at the same time

- c. Use a credit card keeping the balance under 25% of the credit limit

- d. All of the above

Question 09

After paying off a high-interest credit card, you should:

- a. Continue using it occasionally

- b. Close the account

- c. Use the full amount of available credit every month

Question 10

Which of the following does a credit score MAINLY indicate?

- a. Knowledge of consumer credit

- b. Amount of consumer debt

- c. Risk of not repaying a loan

- d. Financial resources to pay back loans

Question 11

How long can negative items on your credit history impact your score?

- a. 1 year

- b. 3 years

- c. 5 years

- d. 7 years

Question 12

Are missed payments a factor used to calculate a credit score?

- a. Yes

- b. No

- c. Maybe

Question 13

Which of the following is NOT considered when calculating your FICO score?

- a. Your payment history

- b. The types of credit you are using

- c. The amount of debt you owe

- d. Your income

Question 14

Applying for credit cards in order to just receive a free sign-up gift (t-shirt, mugs, etc.) has no impact on my credit profile?

- a. True

- b. False

Question 15

Is marital status a factor used to calculate a credit score?

- a. Yes

- b. No

- c. Maybe

Question 16

Does a cell phone company use a credit score to decide whether a person can buy a service and/or what price they'll pay?

- a. Yes

- b. No

- c. Maybe

Question 17

Does a mortgage lender use a credit score to decide whether a person can get credit and what interest rate they'll pay?

- a. Yes

- b. No

- c. Maybe

Question 18

Does a landlord use a credit score to decide whether a person can rent a property and/or what price they'll pay?

- a. Yes

- b. No

- c. Maybe

Question 19

Does an electric utility use a credit score when establishing service for a consumer?

- a. Yes

- b. No

- c. Maybe

Question 20

Your credit card company just increased the spending limit on your card. Will this help or hurt your credit score?

- a. Help

- b. Hurt

Question 21

In regards to a married couple purchasing a home, the mortgage lender uses which credit score when more than one borrower is applying together?

- a. The highest score between both people

- b. The lowest middle score between both people

- c. The average of all scores

- d. The median score between both people

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

email: kentuckyloan@gmail.com

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916 http://www.nmlsconsumeraccess.org/

-- Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Fill out my form!

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Subscribe to:

Posts (Atom)