Kentucky FHA loan limits for 2026: county coverage, requirements, and FHA vs conventional

FHA loan limits set the maximum mortgage amount the Federal Housing Administration will insure. These limits directly affect how much Kentucky homebuyers can borrow using FHA financing and help set realistic expectations when purchasing a home.

For 2026, the Department of Housing and Urban Development increased FHA loan limits nationwide due to continued home price appreciation. The new limits apply to FHA case numbers assigned on or after January 1, 2026.

2026 FHA loan limits in Kentucky (all counties)

All 120 Kentucky counties fall under the standard FHA floor limits for 2026. There are no high-cost county exceptions in Kentucky.

- 1-unit (single-family): $541,287

- 2-unit: $693,050

- 3-unit: $837,700

- 4-unit: $1,041,125

These limits apply to FHA purchase and refinance transactions when FHA credit, income, and underwriting requirements are met.

Kentucky FHA loan limits by county (2026)

Every Kentucky county listed below uses the same FHA loan limits for 2026:

Adair, Allen, Anderson, Ballard, Barren, Bath, Bell, Boone, Bourbon, Boyd, Boyle, Bracken, Breathitt, Breckinridge, Bullitt, Butler, Caldwell, Calloway, Campbell, Carlisle, Carroll, Carter, Casey, Christian, Clark, Clay, Clinton, Crittenden, Cumberland, Daviess, Edmonson, Elliott, Estill, Fayette, Fleming, Floyd, Franklin, Fulton, Gallatin, Garrard, Grant, Graves, Grayson, Green, Greenup, Hancock, Hardin, Harlan, Harrison, Hart, Henderson, Henry, Hickman, Hopkins, Jackson, Jefferson, Jessamine, Johnson, Kenton, Knott, Knox, Larue, Laurel, Lawrence, Lee, Leslie, Letcher, Lewis, Lincoln, Livingston, Logan, Lyon, McCracken, McCreary, McLean, Madison, Magoffin, Marion, Marshall, Martin, Mason, Meade, Menifee, Mercer, Metcalfe, Monroe, Montgomery, Morgan, Muhlenberg, Nelson, Nicholas, Ohio, Oldham, Owen, Owsley, Pendleton, Perry, Pike, Powell, Pulaski, Robertson, Rockcastle, Rowan, Russell, Scott, Shelby, Simpson, Spencer, Taylor, Todd, Trigg, Trimble, Union, Warren, Washington, Wayne, Webster, Whitley, Wolfe, Woodford

Kentucky FHA loan requirements for 2026

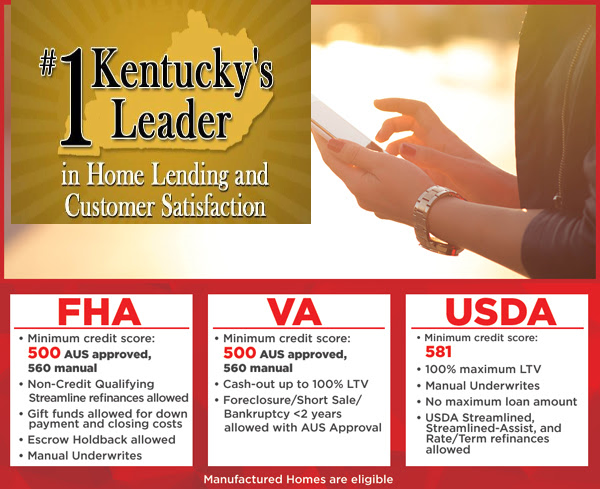

Credit score

Most Kentucky FHA lenders require a minimum credit score of 580 to qualify for the 3.5% down payment option. Borrowers with scores between 500 and 579 may qualify with a 10% down payment, subject to lender overlays.

Down payment

The minimum down payment is 3.5% with qualifying credit. Funds may come from savings, documented gifts, retirement accounts (with restrictions), or Kentucky down payment assistance programs.

Debt-to-income ratio

FHA guidelines typically allow up to 31% housing DTI and 43% total DTI. With strong compensating factors, approvals up to 45.99 on front end ratio and 56.9% DTI may be possible on the backend ratio.

Income and employment

Borrowers must show a two-year employment history with verifiable income. Self-employed borrowers generally need two years of tax returns.

Property requirements

The home must be owner-occupied and meet FHA minimum property standards. Eligible properties include single-family homes, FHA-approved condominiums, townhomes, and 2- to 4-unit properties where the borrower occupies one unit.

FHA mortgage insurance (MIP)

Upfront mortgage insurance premium

FHA charges an upfront mortgage insurance premium of 1.75% of the loan amount, typically financed into the loan.

Annual mortgage insurance premium

Annual FHA mortgage insurance is paid monthly and is commonly 0.55% for borrowers putting down 3.5%. FHA mortgage insurance generally remains for the life of the loan unless refinanced.

FHA vs conventional loan limits in 2026

- FHA loan limit in Kentucky (1-unit): $541,287

- Conventional conforming loan limit (baseline): $832,750

FHA loans are often chosen for lower down payment needs and more flexible credit standards. Conventional loans may offer higher loan limits and cancellable PMI for borrowers with stronger credit profiles.

2026 mortgage loan limits for Kentucky (conventional, FHA, VA, USDA)

Mortgage loan limits affect how much homebuyers in Kentucky can borrow using different loan programs. These limits are set annually by federal agencies and vary by loan type, property type, and county.

For 2026, Kentucky remains a standard-cost state, meaning all 120 counties use the national baseline loan limits with no high-cost county adjustments.

Published December 12, 2025

By Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA

Kentucky loan limits overview for 2026

- Total counties in Kentucky: 120

- High-cost counties: None

- Maximum conforming limit statewide: $832,750

2026 Kentucky baseline loan limits

The table below shows the standard 2026 loan limits that apply to all Kentucky counties.

| Loan Type | 1 Unit | 2 Units | 3 Units | 4 Units |

|---|---|---|---|---|

| Conventional | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| FHA | $541,287 | $693,050 | $837,700 | $1,041,125 |

| VA | $832,750* | $1,066,250* | $1,288,800* | $1,601,750* |

| USDA | No loan limit** | Not eligible | Not eligible | Not eligible |

* VA loans do not have a formal loan limit for eligible veterans with full entitlement, but these figures align with conforming loan thresholds.

** USDA loans do not have loan limits. USDA eligibility is based on household income limits and property location in designated rural areas.

Important USDA clarification (this matters)

USDA loans are often misunderstood. There is no maximum loan amount set by USDA. Instead, approval is based on:

- Household income limits (based on county and household size)

- Debt-to-income ratios

- Property eligibility in USDA-designated rural areas

Any source listing a fixed USDA loan limit (such as $433,020) is incorrect.

Kentucky mortgage market insight

Kentucky continues to offer affordable housing compared to national averages. The majority of buyers remain well within conforming loan limits, and jumbo loans are uncommon statewide.

For most Kentucky buyers, FHA, VA, USDA, and conventional conforming loans remain the primary financing options in 2026.

How to use Kentucky loan limits

1. Identify your loan program

Each loan type has different rules. FHA limits are lower but allow smaller down payments. Conventional loans offer higher limits for buyers with stronger credit. VA and USDA loans focus more on eligibility than loan size.

2. Match limits to affordability

Loan limits do not equal approval amounts. Income, credit, debts, and monthly payment comfort matter more than the maximum number.

3. Get pre-approved early

A Kentucky-based lender can review your full financial picture and confirm which loan type fits best before you shop for a home.

Kentucky county loan limits

All Kentucky counties use the same 2026 baseline limits:

Adair, Allen, Anderson, Ballard, Barren, Bath, Bell, Boone, Bourbon, Boyd, Boyle, Bracken, Breathitt, Breckinridge, Bullitt, Butler, Caldwell, Calloway, Campbell, Carlisle, Carroll, Carter, Casey, Christian, Clark, Clay, Clinton, Crittenden, Cumberland, Daviess, Edmonson, Elliott, Estill, Fayette, Fleming, Floyd, Franklin, Fulton, Gallatin, Garrard, Grant, Graves, Grayson, Green, Greenup, Hancock, Hardin, Harlan, Harrison, Hart, Henderson, Henry, Hickman, Hopkins, Jackson, Jefferson, Jessamine, Johnson, Kenton, Knott, Knox, Larue, Laurel, Lawrence, Lee, Leslie, Letcher, Lewis, Lincoln, Livingston, Logan, Lyon, McCracken, McCreary, McLean, Madison, Magoffin, Marion, Marshall, Martin, Mason, Meade, Menifee, Mercer, Metcalfe, Monroe, Montgomery, Morgan, Muhlenberg, Nelson, Nicholas, Ohio, Oldham, Owen, Owsley, Pendleton, Perry, Pike, Powell, Pulaski, Robertson, Rockcastle, Rowan, Russell, Scott, Shelby, Simpson, Spencer, Taylor, Todd, Trigg, Trimble, Union, Warren, Washington, Wayne, Webster, Whitley, Wolfe, Woodford

Published by Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA

Helping Kentucky homebuyers navigate loan limits and financing options with clarity.

Helpful Kentucky homebuyer resources

- Kentucky FHA loan guide

- Kentucky USDA zero-down loans

- Kentucky Housing Corporation programs

- Kentucky first-time homebuyer programs

Published by Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA