Kentucky Mortgage Loan Programs | FHA, VA, USDA & Conventional Guide

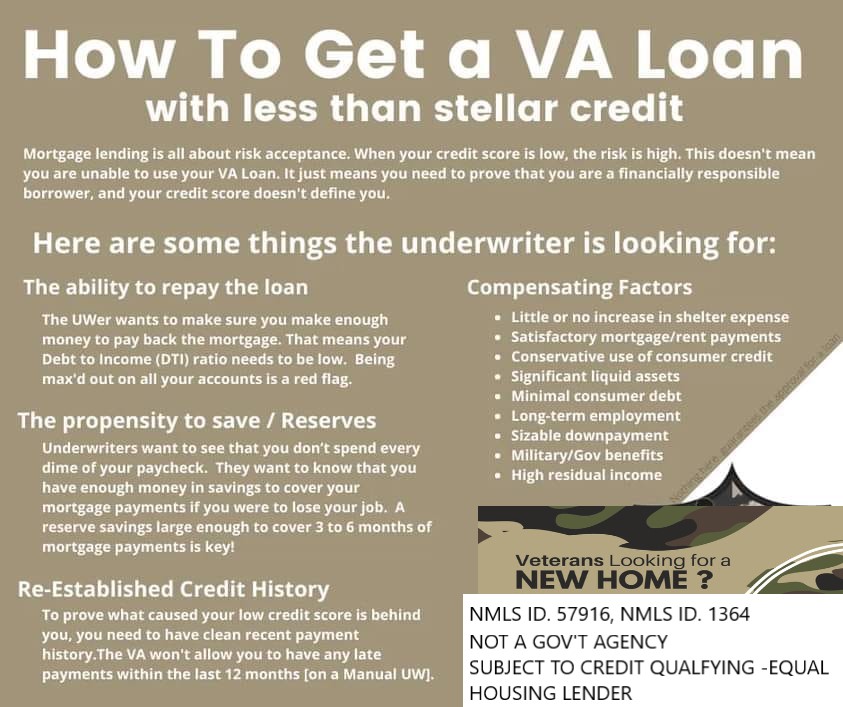

Understanding the Four Main Mortgage Loan Programs in Kentucky When buying a home in Kentucky, your mortgage will typically fall under one of four major loan programs: FHA, VA, USDA, or Conventional (Fannie Mae/Freddie Mac) . Each program offers unique benefits depending on your credit, income, military status, and location. Below is a streamlined breakdown to help you determine the best fit for your situation. Conventional Loan Minimum down payment: 3%–5% Minimum credit score: 620 (680+ for best pricing) Mortgage insurance can be removed at 80% equity Best for: buyers with strong credit & stable income Bankruptcy wait: 4–7 years Foreclosure wait: 7 years Closing costs can be lender-paid (higher rate) Kentucky USDA Rural Housing Loan 100% financing (0% down) Credit score: 640+ for automated GUS approval Mortgage insurance: .35% monthly, 1% upfront Manual underwriting ratio caps: 29% / 41% Property must be U...