I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Kentucky Mortgage Loans with Past Credit Issues: FHA, VA, USDA, Conventional, and KHC Options

Kentucky mortgage loans after credit challenges: your options and next steps

If you’ve had late payments, collections, bankruptcy, or other setbacks, you’re not out of the game. Kentucky homebuyers routinely qualify using the right loan structure, realistic timelines, and clean documentation. Below is a practical breakdown of FHA, VA, USDA, Conventional, and KHC down payment assistance—plus smart internal and external resources.

Program overview

FHA loans in Kentucky

Potential approvals down to 500 with at least 10% down or 10% equity on a refinance.

580+ score typically enables 3.5% down payment.

Gift funds and DPA allowed; flexible underwriting for limited credit depth.

FHA is introducing new guidelines on loan to value ratios and the minimum credit score required for FHA borrowers in Kentucky. As detailed in a Mortgagee Letter from the Department of Housing and Urban Development (HUD), the following credit requirements will apply for FHA borrowers, effective October 4, 2010.

Kentucky FHA Borrowers with a credit score between 500 and 579 will be limited to a loan to value of 90%. A sub 580 FICO credit score borrower will henceforth need to make a 10% minimum down payment on a purchase transaction.

The new credit requirements are not expected to dramatically change the number of Kentucky FHA mortgage approvals.

minimum credit score requirement of 580 to 620 or higher for Kentucky FHA borrowers.

In limited cases, borrowers with scores between 580 and 639 could still obtain mortgage approval with compensating factors such as large down payment (more than 3.5% minimum), low debt to income ratios, and substantial reserves in the bank with a verifiable pay history of no late payments in the last 12 months of rent and on credit report. A late is considered 30 days late in the credit rating world.

Ultimately, there is no singular credit score that can guarantee you a mortgage approval. Each lender is free to set their own credit score requirements.

But many loan types are insured by government organizations. And lenders cannot accept borrowers with credit scores below the minimum these organizations set.

The four most popular home loan types are:

Conventional: Not backed by any government agency, but must meet the Fannie Mae and Freddie Mac underwriting guidelines

FHA: Loans backed by the Federal Housing Administration

VA: Loans backed by the US Department of Veterans Affairs (for military members)USDA: Loans backed by the US Department of Agriculture (for low- to moderate-income families who buy homes in rural areas)

The minimum credit score requirements for each of these loan types:

Conventional:

620 SCORE NEEDED. BUT TO GET APPROVED FOR A FANNIE MAE LOAN MOSTLY LIKE YOU WILL NEED A 720 SCORE OR HIGHER IF YOU HAVE LESS THAN 20% EQUITY POSITION OR LESS THAN 20% DOWN PAYMENT DUE TO PRIVATE MORTGAGE INSURANCE

FHA:

580 for a 3.5% down payment 500 for down payments of at least 10% **MOST FHA LENDERS WILL WANT A 580 to 620 CREDIT SCORE NOWADAYS

VA:

No minimum BUT MOST VA LENDERS WILL WANT A 580 to 620 CREDIT SCORE

USDA:

No minimum, but with a credit score of at least 620 to 640 you could qualify for streamlined credit analysis and chances of approval goes way down if score is below 640...

Which credit score is used to qualify for a Mortgage loan in Kentucky?

For example if you have a 598, 625, 604 on each of the main three reporting agencies, then your qualifying fico score would be 604.

If you’re planning to apply for a mortgage, be aware that the credit score you see on your application might differ slightly from the one you’re used to.

It might even be different than what comes up when you monitor your credit, or even when you apply for a car loan.

Banks use a slightly different credit score model when evaluating mortgage applicants. Below, we go over what you need to know about credit scores you’re looking to buy a home.

The scoring model used in mortgage applications

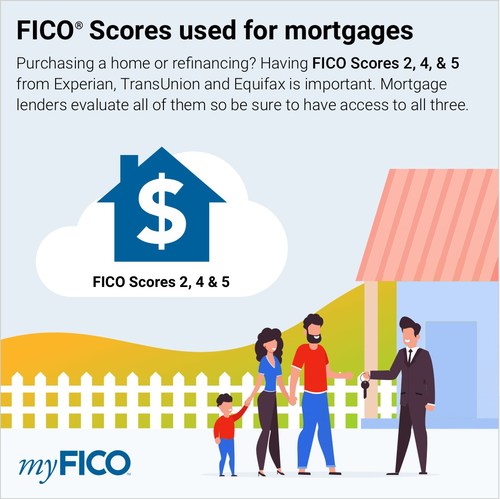

While the FICO® 8 model is the most widely used scoring model for general lending decisions, banks use the following FICO scores when you apply for a mortgage:

As you can see, each of the three main credit bureaus (Equifax, Experian and TransUnion) use a slightly different version of the industry-specific FICO Score. That’s because FICO tweaks and tailors its scoring model to best predict the creditworthiness for different industries and bureaus. You’re still evaluated on the same core factors (payment history, credit use, credit mix and age of your accounts), but the categories are weighed a little bit differently.

The FICO 8 model is known for being more critical of high balances on revolving credit lines. Since revolving credit is less of a factor when it comes to mortgages, the FICO 2, 4 and 5 models, which put less emphasis on credit utilization, have proven to be reliable when evaluating good candidates for a mortgage.

Mortgage lenders pull all three reports,from all three bureaus, but they only use one when making their final decision.

“A bank will use all three bureaus,”--- “It’s called a tri-merge.”

If all three of your scores are the same, then their choice is simple. But what if your scores are different?

If two of the three scores are the same, lenders use that one, regardless of whether it’s higher or lower than the other one.

And if you are applying for a mortgage with another person, such as your spouse or partner, each applicant’s FICO 2, 4 and 5 scores are pulled. The bank identifies the median score for both parties, then uses the lowest of the final two.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).

If you’re a first-time homebuyer in Kentucky, chances are you’ve been checking your credit score on free apps like Credit Karma. It feels like a smart step toward homeownership. But here’s the reality: the score you see on your phone isn’t the score your mortgage lender will use.

This mismatch leaves many Kentucky homebuyers shocked — and sometimes discouraged — when they sit down for a mortgage pre-approval. The truth? It’s not your fault, and it’s more common than you think.

As a Kentucky mortgage loan officer with over 20 years of experience helping 1,300+ families buy homes, I see this confusion almost daily. Let’s break down why your Credit Karma score doesn’t match your mortgage FICO® score — and what that means for your path to homeownership.

1. What Your Credit Karma Score Really Means

Credit Karma is a helpful tool, but it’s not designed for mortgage approval. Here’s why:

Scoring Model: Credit Karma uses the VantageScore model.

Data Sources: It pulls from only two credit bureaus (Equifax & TransUnion) — not Experian.

Primary Purpose: Credit Karma’s purpose is consumer education, not lending decisions.

Mortgage Validity: Mortgage lenders do not use VantageScore for approval.

👉 Bottom line: Your Credit Karma score is best used to track trends in your credit health — not to measure mortgage readiness.

2. What Mortgage Lenders Actually Use: The FICO® Mortgage Scores

When applying for an FHA, VA, USDA, KHC, or Conventional loan in Kentucky, lenders are required to use older, more conservative FICO® models (2, 4, 5) — not the newer FICO 8 or VantageScore.

Here’s the breakdown:

Credit Bureau

Mortgage FICO Model Used

Experian

FICO® Score 2

Equifax

FICO® Score 5

TransUnion

FICO® Score 4

The “Middle Score Rule”

If you have three different scores, the middle one is used.

Example: 680 / 700 / 720 → 700 qualifies.

If two scores are the same, that repeated score is used.

Example: 690 / 690 / 710 → 690 qualifies.

These mortgage FICO scores are stricter and more sensitive to things like:

Collections

Recently opened accounts

Hard inquiries

This is why your mortgage score is often 10–50+ points lower than Credit Karma.

3. Credit Karma vs. Mortgage FICO: Side-by-Side Comparison

Factor

Credit Karma (VantageScore)

Mortgage FICO (2, 4, 5)

Used for Mortgages?

❌ No

✅ Yes

Data Pulled From

Equifax & TransUnion

All 3 Bureaus

Typical Score Difference

10–50+ points higher

Accurate for approval

Purpose

Consumer monitoring

Lending decisions

4. Kentucky Mortgage Credit Score Requirements

Here are the minimum mortgage FICO scores most lenders look for in Kentucky:

FHA Loans: 580 minimum

VA Loans: 620+

USDA Loans: 620+

Conventional Loans: 620 minimum, but 680+ improves approval chances and interest rates

💡 Pro Tip: If you want to see your true mortgage scores before talking to a lender, you can use myFICO.com, which provides access to the same models (FICO 2, 4, 5) we use.

5. Next Steps: Get Pre-Approved the Right Way in Kentucky

Don’t risk disappointment by relying on a consumer app score. The only way to know your true mortgage-ready credit score is to work with a licensed Kentucky mortgage lender who will pull your official FICO 2, 4, and 5 scores.

By getting pre-approved the right way, you’ll:

Avoid surprises when house hunting

Know exactly what price range you can afford

Get positioned for the best possible loan program

A Final Word from Joel Lobb, Kentucky Mortgage Loan Officer

“Your Credit Karma score won’t cut it—we need to pull the FICO 2, 4, 5 scores to get you approved and locked into the right loan. Let’s do this the right way.”

Why credit scores matter for mortgage underwriting

Mortgage lenders use FICO mortgage score models (FICO 2, 4, 5). Consumer scores (VantageScore, Credit Karma) are not used for final underwriting decisions.

Minimum credit scores by program

Conventional: Minimum 620 (automated); better pricing with higher scores. Learn more

The loan must be for a property used for your primary residence.

The property must be appraised by an FHA-approved appraiser.

The property must be safe, sound and secure, in compliance with minimum property standards as defined by the U.S. Department of Housing and Urban Development, or HUD.

You must have a valid Social Security number and be a legal resident of the U.S.

You must have a minimum credit score of 580 with a down payment of at least 3.5 percent, or a minimum credit score of 500 with a down payment of at least 10 percent.

You may not have delinquent federal debt or judgments, or debt associated with past FHA loans.

You must have steady employment history.

You must make a down payment of at least 3.5 percent of the purchase price. If the down payment was gifted by a family member, documentation is required.

You must have a DTI ratio that does not exceed limits.

Any judgments or collections on the credit report must be resolved or satisfactorily explained.

Any required waiting period has passed, as follows:

Event

Waiting period

Waiting period with extenuating circumstances (nonrecurring events beyond your control that result in sudden, significant, prolonged reduction in income or a catastrophic increase in financial obligations)

Chapter 7 or 11 bankruptcy

Four years

Two years

Chapter 13 bankruptcy

Two years from discharge, or four years from dismissal

Two years

Multiple bankruptcies

Five years if more than one filing in last seven years. Most recent bankruptcy must have been caused by extenuating circumstances.

Three years from most recent discharge or dismissal

Foreclosure

Seven years

Three years, with additional requirements after three years up to seven years: 90 percent maximum loan-to-value purchase, principal residence, limited cash-out refinance

Deed-in-lieu of foreclosure, preforeclosure sale (short-sale), or charge-off of mortgage account

Four years

Two years

Debt-to-Income Ratio Limits for Kentucky FHA Loans

Two DTI ratio figures are calculated when considering an Kentucky FHA mortgage. Thefront-end DTIratio is your total monthly housing expense, which includes the mortgage principal and interest, mortgage insurance, homeowners insurance, property taxes and applicable homeowners association fees, divided by your total monthly income. The back-end DTI ratio is your total monthly debt obligation, including housing, minimum credit card payments, auto loans, student loans and any other required monthly debt payment, divided by your total monthly income.

Standard FHA front- and back-end DTI limits are 31 percent and 43 percent, respectively. If you earn $3,500 per month, your front-end DTI cannot exceed $1,085 and the sum of all your monthly debt obligations cannot exceed $1,505. f Applications for Kentucky FHA borrowers with lower salaries and higher DTIs are manually underwritten. Manual underwriting means that your lender assigns a person to review your loan application and documents, versus running your information through an automated underwriting system. Manually underwritten FHA loans allow for front- and back-end DTI ratios of up to 40 percent and 50 percent, respectively. To qualify for these higher DTI limits, you will need to meet other requirements.

This page is for informational purposes and does not constitute loan approval. Program availability, limits, and terms change — contact us to confirm current eligibility and funding.

To qualify for an FHA loan in Kentucky, you'll need to meet several requirements. Here's a detailed breakdown of what lenders will be looking for in 2025:

Credit Score Requirements

While the FHA itself doesn't set a minimum credit score, most Kentucky FHA lenders do. For 2025, you'll generally need a credit score of at least 580 to qualify for the 3.5% low down payment option. If your score is between 500 and 579, you may still be eligible, but you'll likely need to make a larger down payment of at least 10%.

It's important to note that different lenders may have varying credit score requirements, with some requiring scores of 620 or higher. Shopping around with multiple Kentucky FHA lenders can help you find one that works with your specific credit situation.

Down Payment Requirements

As mentioned, the minimum down payment for an FHA loan is 3.5% of the purchase price for borrowers with a credit score of 580 or higher. This down payment can come from several sources:

Your personal savings

A gift from a family member (with proper documentation)

Down payment assistance programs available in Kentucky

Funds from a retirement account (with restrictions)

Debt-to-Income (DTI) Ratio

Your DTI ratio is the percentage of your gross monthly income that goes towards paying your monthly debts. For FHA loans, your housing DTI (mortgage payment including principal, interest, taxes, insurance, and HOA fees) should ideally be no more than 31% of your income, and your total DTI (all debts) should be no more than 43%.

However, with a strong credit score and other compensating factors, you may be approved with a higher DTI, potentially up to 55% in some cases. Kentucky FHA lenders will evaluate your entire financial picture when making this determination.

Income and Employment Requirements

You'll need to demonstrate a steady employment history for the past two years. Your income must be verifiable through pay stubs, tax returns, and other documentation. Self-employed individuals will need to provide at least two years of tax returns to demonstrate consistent income.

Recent college graduates may be able to use their education to satisfy the employment history requirement if they can show their degree relates to their current employment.

Property Requirements

The home you're buying must be your primary residence - you cannot use an FHA loan for investment properties or vacation homes. The property also needs to meet the FHA's minimum property standards, which means it must be safe, sound, and secure. An FHA-approved appraiser will inspect the property to ensure it meets these standards.

Eligible property types in Kentucky include single-family homes, condominiums (in FHA-approved projects), townhomes, and multi-unit properties (up to 4 units) where you'll live in one of the units.

2025 FHA Loan Limits in Kentucky

For 2025, the FHA has set the following loan limits for all counties in Kentucky:

Single-Family Home (1-unit): $524,225

2-Unit Property: $671,200

3-Unit Property: $811,275

4-Unit Property: $1,008,300

These limits apply to all 120 Kentucky counties, as there are no high-cost county exceptions in the state for 2025. This means whether you're buying in Jefferson County (Louisville), Fayette County (Lexington), or any rural Kentucky county, the same loan limits apply. It's important to note that these limits can change annually based on housing market conditions.

FHA Mortgage Insurance Premium (MIP)

FHA loans require two types of mortgage insurance premiums that protect the lender in case of default:

Upfront Mortgage Insurance Premium (UFMIP)

This is a one-time premium of 1.75% of the loan amount, which is typically financed into the loan rather than paid out of pocket at closing. For example, on a $200,000 loan, the UFMIP would be $3,500.

Annual Mortgage Insurance Premium (MIP)

This premium is paid monthly as part of your mortgage payment. The amount varies from 0.45% to 1.05% of the loan amount annually, depending on your loan term, loan-to-value ratio, and down payment. For most borrowers with the minimum 3.5% down payment, the annual MIP is 0.85% of the loan amount.

Unlike conventional loan PMI, FHA MIP typically cannot be removed unless you refinance to a conventional loan or pay down your loan balance to 78% of the original purchase price (and the loan is at least 5 years old).

How to Apply for a Kentucky FHA Loan

Applying for an FHA loan in Kentucky is a straightforward process when you work with an experienced Kentucky FHA mortgage lender. Here are the detailed steps you can expect:

Step 1: Get Pre-Approved

The first step is to get pre-approved with an FHA-approved lender. During pre-approval, the lender will review your credit, income, assets, and debts to determine how much you can borrow. This gives you a clear idea of your budget and shows sellers that you are a serious buyer in Kentucky's competitive housing market.

Step 2: Gather Required Documents

You will need to provide various financial documents, including:

Recent pay stubs (typically last 30 days)

Tax returns for the past 2 years

Bank statements for the past 2-3 months

Employment verification letter

Valid government-issued identification

Social Security card

Documentation of any additional income sources

Step 3: Find a Home

Once you are pre-approved, you can start shopping for a home that meets your needs and the FHA's property requirements. Consider working with a real estate agent familiar with FHA loans and Kentucky's housing market to help you find suitable properties.

Step 4: Complete the Loan Application

After you have an accepted offer on a home, you will complete the full loan application with your Kentucky FHA lender. This includes providing updated documentation and any additional information requested by the underwriter.

Step 5: Home Appraisal and Inspection

The lender will order an FHA appraisal to ensure the home meets FHA property standards and is worth the purchase price. You may also want to get a separate home inspection for your own peace of mind.

Step 6: Final Underwriting and Approval

The underwriter will review all documentation and make a final decision on your loan. They may request additional documentation or clarification during this process.

Step 7: Closing

Once your loan is approved and all conditions are met, you will close on your new Kentucky home and get the keys!

Frequently Asked Questions (FAQs)

Can I get an FHA loan with a bankruptcy?

Yes, it is possible to get an FHA loan after a bankruptcy. Generally, you will need to wait at least two years after a Chapter 7 bankruptcy discharge and have re-established good credit. For a Chapter 13 bankruptcy, you may be able to qualify after making 12 on-time payments in your plan, with court approval.

Are FHA loans only for first-time homebuyers?

No, FHA loans are available to all qualified homebuyers, not just first-time buyers. They are a great option for anyone who can meet the eligibility requirements, including repeat buyers and those looking to refinance.

What is the difference between an FHA loan and a conventional loan?

The main differences include down payment requirements (3.5% vs typically 5-20%), credit score requirements (580 vs typically 620+), and mortgage insurance (MIP vs PMI). FHA loans are generally more accessible but require mortgage insurance for the life of the loan in most cases.

Can I use an FHA loan to buy a fixer-upper in Kentucky?

Yes, the FHA 203(k) renovation loan program allows you to finance both the purchase and renovation costs in a single loan. This can be a great option for buyers looking to purchase and improve a home in Kentucky.

How long does it take to close on an FHA loan in Kentucky?

Typically, FHA loans take 30-45 days to close from the time of application, though this can vary based on the lender, property type, and complexity of your financial situation.

Ready to Get Started with Your Kentucky FHA Loan?

Don't let another month go by without taking action toward homeownership. Kentucky's housing market is competitive, and having your financing in place gives you a significant advantage.

Our experienced Kentucky FHA mortgage specialists are ready to guide you through every step of the process.

Find the Right Kentucky FHA Mortgage Lender

Choosing the right lender is just as important as choosing the right loan. Look for a Kentucky FHA mortgage lender that is experienced with FHA loans and can guide you through the process smoothly. A good lender will:

Answer your questions promptly and thoroughly

Help you understand your options and loan terms

Work with you to find a loan that fits your financial situation

Provide competitive rates and fees

Have experience with Kentucky's local housing market

Offer excellent customer service throughout the process

Kentucky Housing Market Insights for 2025

Understanding Kentucky's housing market can help you make informed decisions about your FHA loan. As of 2025, Kentucky continues to offer relatively affordable housing compared to national averages, making it an attractive state for first-time homebuyers using FHA loans.

Major Kentucky cities like Louisville, Lexington, Bowling Green, and Owensboro each offer unique opportunities for FHA loan borrowers. Rural areas of Kentucky also present excellent value propositions for families looking to maximize their purchasing power with an FHA loan.

An FHA loan can be an excellent path to homeownership for Kentucky residents, offering flexible requirements, competitive rates, and low down payment options. Whether you're a first-time homebuyer in Louisville, a growing family in Lexington, or anyone in between looking to purchase a home in the Bluegrass State, an FHA loan might be the perfect solution for your needs.

The key to success is working with an experienced Kentucky FHA mortgage lender who understands both the FHA program requirements and the local Kentucky housing market. Take the first step today by getting pre-approved and discovering how much home you can afford with an FHA loan.

Ready to take the next step towards homeownership in Kentucky?

About the Author

Joel Lobb is a licensed Kentucky Mortgage Loan Officer (NMLS #57916) with more than 20 years of experience helping families across Kentucky achieve homeownership. Specializing in FHA, VA, USDA, and KHC loan programs, Joel has guided over 1,300 families through the mortgage process—including hundreds of borrowers with credit scores in the 580–620 range.

Licensing Information

• NMLS Personal ID: 57916

• Company NMLS ID: 1738461 (EVO Mortgage)

• Licensed to originate mortgage loans in Kentucky only

• Equal Housing Lender

Legal Disclaimers

This website is for educational purposes only and does not constitute financial or legal advice. Loan programs, rates, and requirements are subject to change without notice. Not all borrowers will qualify. This information is not endorsed or sponsored by FHA, VA, USDA, Fannie Mae, or any government agency.

Joel Lobb is licensed to originate mortgages in Kentucky only.

Equal Housing Lender. All rights reserved. Licensed by the Kentucky Department of Financial Institutions.

.")

.png "Minimum Credit Scores for FHA, VA, USDA, and Conventional Loans in Kentucky")

.png "How to Qualify For a Kentucky FHA Mortgage Loan")

Call/Text -

Call/Text -