I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 1300 Kentucky families buy their first home or refinance their current mortgage for a lower payment; Kentucky First time buyers we still how available down payment assistance with KHC. Free Mortgage applications/ same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS 1738461

Showing posts with label FHA minimum credit score. Show all posts

Showing posts with label FHA minimum credit score. Show all posts

Kentucky FHA Mortgage Loans

Kentucky FHA Loan Requirements For 2022

How to Qualify for a Kentucky FHA Mortgage Loan with a lender?

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Kentucky FHA Mortgage Guidelines in Video

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

fax: 502-327-9119

email: kentuckyloan@gmail.com

email: kentuckyloan@gmail.com

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

What is a Good Credit Score for a Kentucky FHA, VA, USDA, Fannie Mae Conventional KHC Mortgage Loan Approval?

What is a Good Credit Score

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

What is a Good Credit Score?

An established credit history and credit score often stands between potential home or car buyers and their dream. But What is a good credit score? What exactly is a credit score? What makes a credit score “good?” How to improve your credit score? If you’re new to building credit there are a few things you need to know in order to keep your credit looking stellar.

What is a credit score?

Your credit score is a numerical representation of your credit report. This three-digit number is like a badge that predicts risk, credit responsibility and determines your interest rates if you borrow money from lenders much like your CLUE Report. While you will be able to get a copy of your credit report you may not find this numerical key listed. Think of your credit score like the cliff notes version of your credit report. There are a few different measures of credit scores between divisions. Based on their own systems different scorers might view certain numbers in many ways.

Your credit score is a numerical representation of your credit report. This three-digit number is like a badge that predicts risk, credit responsibility and determines your interest rates if you borrow money from lenders much like your CLUE Report. While you will be able to get a copy of your credit report you may not find this numerical key listed. Think of your credit score like the cliff notes version of your credit report. There are a few different measures of credit scores between divisions. Based on their own systems different scorers might view certain numbers in many ways.

what is a good credit score

Deciphering your three-digit credit score is quite easy if you know the levels. The range usually runs from 300-850. Good to excellent credit is considered anything from 700 to 850. If your credit score falls in this range you’re going great! Fair credit runs from 625-699, poor runs from 550-624, and anything below 550 is bad. Some finance experts would classify anything over 720 a good credit rating. Experts will disagree depending on their preferred credit rating systems, and in most cases the criteria you use to determine whether or not your credit score is good will not be far off.

What Does a Good Credit Score Mean?

Having a good credit score is great, but if you don’t know how to use it you could be missing out on some crucial credit building. Credit scores are used in varying ways by lenders and banks. One thing your credit score implies is how likely you are to pay back debt. Basically it announces how reliable you are as a borrower. People with good credit scores are more likely to pay back funds that they borrow while those with lower scores aren’t so reliable. Lenders like reliable borrowers, and good credit points them out.

Having a good credit score is great, but if you don’t know how to use it you could be missing out on some crucial credit building. Credit scores are used in varying ways by lenders and banks. One thing your credit score implies is how likely you are to pay back debt. Basically it announces how reliable you are as a borrower. People with good credit scores are more likely to pay back funds that they borrow while those with lower scores aren’t so reliable. Lenders like reliable borrowers, and good credit points them out.

But a credit score does much more than predict whether or not you’ll pay a loan back. When it comes to buying a house or car, there is an interest charge. Higher credit scores usually have a lower interest rate than those with bad to fair credit. Lenders not only base whether or not they’ll approve a loan by your credit score, but also how much interest to charge. If your credit is in good standing your interest rate won’t be as high as someone with bad credit. Your credit score saves you money with lower interest rates.

How is a Credit Score Calculated?

In order to build and maintain good credit you must first know how your score is determined. Once you know what goes into a credit score you can begin building your credit or nursing your score towards higher digits. Credit scores are based on your financial history only, and laws prevent your score being affected by things like race, gender, age and where you live. What is included are items such as your payment history, your current credit debts, age of your credit history, new credit items added to your accounts and types of credit used.

In order to build and maintain good credit you must first know how your score is determined. Once you know what goes into a credit score you can begin building your credit or nursing your score towards higher digits. Credit scores are based on your financial history only, and laws prevent your score being affected by things like race, gender, age and where you live. What is included are items such as your payment history, your current credit debts, age of your credit history, new credit items added to your accounts and types of credit used.

These five basic areas are where the bulk of your credit score is formed. All criteria have varying degrees of involvement in your score. For example:

- Payment history (35%) – How many on-time payments you’ve made, missed, defaulted and past due items

- Current amount owed (30%) – How much you currently owe – if you owe a large amount this could negatively affect your score

- Age of credit history (15%) – The average length of your credit accounts and time since last activity

- New credit (10%) – The number of new credit items on your accounts

- Types of credit (10%) – The kinds of credit accounts are you currently maintain

How to Improve Your Credit Score?

Many people avoid credit based on all the negatives they’ve heard against it, but neglecting your credit score hurts your chances of being able to make major purchases in the future. The best way to build credit is to use credit, and forming the following good credit habits early will pull your low score to higher ground.

Many people avoid credit based on all the negatives they’ve heard against it, but neglecting your credit score hurts your chances of being able to make major purchases in the future. The best way to build credit is to use credit, and forming the following good credit habits early will pull your low score to higher ground.

- Pay bills on time – This is the easiest and best way to boost your credit score. Since the bulk of your credit score comes from your payment history, paying bills on time will pull you up quickly. Not only will that help, but a recent and consistent history of paying bills on time overshadow a period long in the past where you may have missed payments.

- Budget – Setting up a budget and staying within its parameters will keep you from overspending and using credit for frivolous things. Although using credit builds credit not being able to pay it off hurts more in the future.

- Use all your credit cards regularly – If you have a few credit cards try to use them from time to time in order to show that you use all of your accounts. Remember that the last usage of an account is 15% of your score.

Track a key aspect of your financial profile with your personal FICO® Score history graph. Simply navigate over any point of your score history and view the date the score was calculated. Check back each month to stay on top of changes.

Important items to note:

- We may not receive a new score for you each month. You won’t see a score if we did not receive one for a given month.

- Remember, FICO® Scores are based on data in your credit report, so changes to your score may be a result of changes in your credit report. You can request a free annual credit report from Equifax at www.annualcreditreport.com.

Please refer to our FAQs or Useful Links sections for more information.

FICO® Scores: What You Need to Know

Score Deciding Factors

35% payment history, 30% amount you owe, 15% length of credit history, 10% new credit opened, 10% type of credit.

When it comes to getting a home loan, does your credit report and credit score really matter? Can you use the free credit score you got off the internet to apply for a loan? What if your credit score is low, can you get a mortgage? What if it is high, will you get a better interest rate? And what the heck is FICO?

So many questions. You’ve searched the internet and are still confused. If you are new to getting a mortgage and are overwhelmed by understanding your credit score you are not alone. Your credit score has a big impact on your ability to qualify for a loan and get a favorable interest rate. Therefore, you should take the time now to understand it.

Here’s the good news. We’re here to explain things simply and clearly. Step by step we will walk you through all things credit. When we’re done, you’ll know what you need to know to understand how credit impacts your ability to get a mortgage so you can make smart home buying decisions.

Below are the important items we will discuss:

- What is a credit report?

- What do mortgage lenders use to determine my credit score?

- What does FICO stand for?

- What determines my FICO score?

- What’s a good FICO score?

- What if my FICO score is below 620?

- Can I get a copy of my credit report?

- Ah Ha! Now I understand all things credit and I’m this much closer to owning my home!

What is a credit report?

A credit report record’s your credit history including information about:

- Your identity: name, social security number, date of birth and possibly employment information.

- Your existing credit: credit card accounts, mortgages, car loans, students loans etc.including credit terms, how much you owe, and your payment history.

- Your public record: Judgments against you, tax liens or bankruptcies.

- Recent Credit Inquiries: Requests for your information from companies extending credit such as credit card companies, auto loans, etc.

Be aware, credit card companies, car companies and mortgage lenders use slightly different models to determine credit risk. Today we are focusing on Mortgage related credit.

How do lenders calculate my credit score?

Your credit score is the key to your castle. Your home is most likely the most expensive purchase you will ever make. Therefore, when buying a home, lenders use a different system for assessing risk than credit card companies or even auto loan companies use.

Mortgage lenders use a comprehensive system of checking credit called a Residential Mortgage Credit Report (RMCR), commonly called a “Tri-Merge” report. The RMCR report combines your three credit reports from the three national credit bureaus, Equifax, Experian, and TransUnion. Each credit reporting agency calculates your credit score or FICO Score differently. Therefore, pulling from all three bureaus gives lenders a more complete picture of your credit behavior.

Once pulled, lenders use the average of these three scores, usually the middle score, to determine loan qualification and interest rate. For example, if Equifax gives you a 720, Experian a 730 and TransUnion a 740, the lender will use the 730 FICO Score to help determine the terms of your mortgage. If you are applying for a loan jointly, your partner’s three reports will also be pulled.

What does FICO stand for?

FICO stands Fair, Isaac and Company. Over 25 years ago, lenders began using FICO’s scoring model, or algorithm, to fairly and more accurately determine a person’s credit risk. Since it’s inception, FICO’s continually updates its’ algorithms to reflect more current lending trends and consumer behaviors. Today, FICO Scores are used by over 90% of enders. Importantly, your FICO score can impact your loan interest rates, terms, approvals and more.

What determines my FICO score?

A Mortgage FICO score is determined by an algorithm that generally looks at five credit factors including payment history, current level of indebtedness, types of credit used, length of credit history and new credit accounts.

What’s a good FICO score?

To qualify for a conventional loan, most Mortgage lenders require a FICO score of 620+. The best interest rates go to borrowers with a 740+ FICO score. For each 40 point drop, borrowers can expect to see a slightly higher interest rates by about 0.2 percentage points. If a borrower drops below 660, the increase is likely to be twice as big, a 0.43 percentage point increase. If your credit score is below 620, it is very difficult to get a conventional loan in today’s marketplace. However, don’t be discouraged. You may still be able to buy a home.

What if my FICO or credit score is below 620?

If your score is below 620, you may still be able to buy a home. There are several options:

- Put more money down. Some lenders offset a weak credit score with a higher down payment. A higher down payment gives you more equity in your home, lowering the lender’s risk.

- You may qualify for a non conventional government issued loan such as an FHA, Veterans Affairs and/or U.S. Department of Agriculture loan which have less stringent lending requirements.

- You may work to get that credit score up!

- Correct any errors on your report. Analyze your credit items line by line. If you notice a mistake, dispute it right away with either the credit bureau providing the report or the company that providing the incorrect information to the credit bureau.

- Make all your payments on time. Late payments are the No. 1 way to lower your credit score.

- Pay down revolving debt. Keeping your credit balances low helps to raise your score.

- Sit back and relax. As long as you're paying down debt and making payments on time, your credit score will eventually rise on its own.

Can I get a copy of my credit report after a lender has pulled it?

Yes! In fact, you can get one free credit report every twelve months from each of the nationwide credit bureaus—Equifax, Experian, and TransUnion. You may also purchase your credit score at any time from any of the credit bureaus. Some Mortgage lenders will tell you your score when you apply for a loan or even give you a copy of your report but they are not required to do so. However, if a lender denies you credit, under the Fair Credit Reporting Act (FCRA) you are entitled to a free copy of your personal credit report if you have received notice that in the past 60 days you have been declined credit

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

email: kentuckyloan@gmail.com

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916 http://www.nmlsconsumeraccess.org/

-- Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

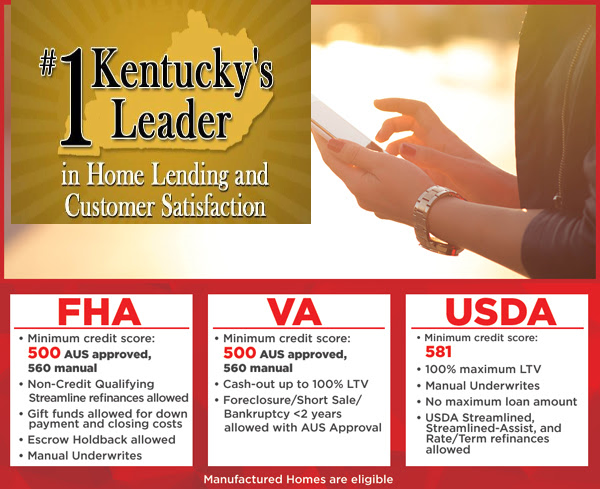

We’ve dropped our minimum FICO score to 620 for Kentucky Mortgage Loan Approvals

Now that’s refreshing!

Call me today to qualify your borrowers with one of our great programs:

KENTUCKY FHA MORTGAGE LOANS

Minimum credit score

620 AUS approved

640 manual

Non-Credit Qualifying Streamline refinances allowed

Gift funds allowed for down payment and closing costs

Cash out 80% LTV

KENTUCKY VA MORTGAGE LOANS

Minimum credit score

620 AUS approved

640 manual/640 High BA

Cash-out up to 90% LTV

Foreclosure/Short Sale/Bankruptcy <2 allowed="" approval="" aus="" p="" with="" years="">

KENTUCKY RURAL USDA MORTGAGE LOANS

Minimum credit score: 620

100% maximum LTV

Manual Underwrites

No maximum loan amount

Rate/Term refinances allowed

KENTUCKY CONVENTIONAL MORTGAGE LOANS

620 min score

Fannie Mae

Freddie Mac

Standard and High Balance

HomeReady

HomePossible

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

fax: 502-327-9119

email: kentuckyloan@gmail.com

email: kentuckyloan@gmail.com

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

KENTUCKY FHA LOAN CREDIT SCORE REQUIREMENTS

What credit score do I need to qualify for Kentucky FHA loan is one of the most common questions lenders hear. The short answer is you must have a minimum credit score of 500 to be eligible for an Kentucky FHA loan. Higher scores will get you better terms and a smaller down payment requirement. Anything lower than 500 disqualifies you from consideration for an Kentucky FHA loan.

There are two sets of credit score requirements.

One important thing to understand is that the Federal Housing Administration (FHA) does not lend money directly to home buyers. You will fill out an application with a regular lender just as you would if you were applying for any other type of mortgage. What the FHA does is ensure your loan to help protect the lender in case you default. You will be required not only to meet the FHA guidelines to qualify for a loan but also meet any additional qualifications required by the lender. This means there are two sets of requirements you have to meet with your credit score.

1. The first set of requirements comes from the Department of Housing and Urban Development (HUD). HUD oversees the FHA and determines what a borrower’s minimum eligibility requirements will be to obtain an FHA loan.

2. The second set of requirements comes from the mortgage lender. The mortgage lender has the right to add its requirements to those mandated by HUD.

What HUD requires of borrowers to be eligible for an FHA loan

The HUD Handbook 4000.1 includes the official guidelines when it comes to the FHA mortgage insurance program.

It states that in 2020 the borrowers with credit scores of 580 or higher are eligible for a 96.5% loan with 3.5% down.

Borrowers with credit scores from 500 to 579 are eligible for a 90% loan with 10% down.

Individuals with credit scores below 500 are not eligible for the FHA program.

What lenders may require of borrowers to be eligible for an FHA loan

Lenders have the right to add requirements over and above the minimum requirements of HUD. These additional requirements are called overlays. Your lender may or may not require them. This is not something that should come as a surprise to you, however. Requiring a credit score of 580 to 620 is not unusual. In addition to your credit score, you must have a manageable debt level that lenders are comfortable with and enough income to repay your loan.

What credit score do I need to qualify for FHA loan?

These percentages show that the majority of borrowers who successfully qualify for FHA loans fall into the 600 to 799 range. While it is true that some successfully qualify in the low range of 500 to 599, you have a much better chance of being approved for a loan with good terms and a low down payment if you fall into the higher range.

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

How Do Mortgage Companies Average the Score on All 3 Credit Reports?

How Do Mortgage Companies Average the Score on All 3 Credit Reports?

Your credit score measures your risk of paying late or defaulting on a loan. Lenders use credit scores along with the rest of your loan information to measure your likelihood of paying back the debt on time. Credit scores allow mortgage companies to use software programs called automated underwriting systems, or AUS, to determine if the amount of risk is acceptable for the loan program requested.

The three major credit bureaus are Equifax, Experian and TransUnion. Lenders are encouraged to report loans and payment history to the credit bureaus on a monthly basis. When companies need to examine a potential borrower's payment history, they buy a credit report using the borrower's name, address and Social Security number. Each credit bureau calculates the credit score differently. This is why the exact same information can be on all three credit reports and they all report a different credit score.

Many factors affect your credit score. Making your payments on time every month is one important factor. Payments made more than 30 days late will lower your credit score. Collections, judgments, tax liens, bankruptcy and foreclosure can have devastating effects on your credit score. Each time you authorize someone to look at your credit that can lower your credit score as well.

One misconception is the belief that paying off credit cards will raise your credit score. The credit bureaus want to see your ability to manage ongoing credit without missing payments or using the entire credit line. Pay down your credit cards so the balances are between 30 to 45 percent of the total available credit line. The older the credit line, the better. If you close a credit card, close the newest ones first and keep the older ones.

Mortgage lenders require access to all three credit bureaus for each borrower. They use the mid-credit score. If your three scores were 780, 776 and 790 they would use the middle of the three scores, in this case 780. They would not average the scores by adding the three numbers together and dividing the sum by three.

In January 2010, the Federal Housing Authority, or FHA, began requiring a minimum 580 credit score for any FHA loan with less than a 10 percent down payment or equity if the loan is a refinance. Conventional loans require a minimum credit score of 620. Lenders are allowed to require their own minimum credit score requirements beyond what the mortgage investors and insurers require. Having the required score does not guarantee loan approval; it is only one factor that lenders consider when approving a loan.

References

Consumer Federation of America: Your Credit Scores

Credit Report.com: Credit Scores

Consumer Credit Help: Do They Add All Three Credit Score Points Together?

Your credit score measures your risk of paying late or defaulting on a loan. Lenders use credit scores along with the rest of your loan information to measure your likelihood of paying back the debt on time. Credit scores allow mortgage companies to use software programs called automated underwriting systems, or AUS, to determine if the amount of risk is acceptable for the loan program requested.

Credit Bureaus

The three major credit bureaus are Equifax, Experian and TransUnion. Lenders are encouraged to report loans and payment history to the credit bureaus on a monthly basis. When companies need to examine a potential borrower's payment history, they buy a credit report using the borrower's name, address and Social Security number. Each credit bureau calculates the credit score differently. This is why the exact same information can be on all three credit reports and they all report a different credit score.

Factors that Affect Credit Scores

Many factors affect your credit score. Making your payments on time every month is one important factor. Payments made more than 30 days late will lower your credit score. Collections, judgments, tax liens, bankruptcy and foreclosure can have devastating effects on your credit score. Each time you authorize someone to look at your credit that can lower your credit score as well.

Raising Your Credit Score

One misconception is the belief that paying off credit cards will raise your credit score. The credit bureaus want to see your ability to manage ongoing credit without missing payments or using the entire credit line. Pay down your credit cards so the balances are between 30 to 45 percent of the total available credit line. The older the credit line, the better. If you close a credit card, close the newest ones first and keep the older ones.

Finding the Middle Score

Mortgage lenders require access to all three credit bureaus for each borrower. They use the mid-credit score. If your three scores were 780, 776 and 790 they would use the middle of the three scores, in this case 780. They would not average the scores by adding the three numbers together and dividing the sum by three.

Minimum Credit Score Requirement

In January 2010, the Federal Housing Authority, or FHA, began requiring a minimum 580 credit score for any FHA loan with less than a 10 percent down payment or equity if the loan is a refinance. Conventional loans require a minimum credit score of 620. Lenders are allowed to require their own minimum credit score requirements beyond what the mortgage investors and insurers require. Having the required score does not guarantee loan approval; it is only one factor that lenders consider when approving a loan.

References

Consumer Federation of America: Your Credit Scores

Credit Report.com: Credit Scores

Consumer Credit Help: Do They Add All Three Credit Score Points Together?

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Kentucky FHA Home buyers with heavy debt might find it tougher to get a mortgage with FHA in 2019

Homebuyers with heavy debt might find it tougher to get a mortgage:

--

Text/call: 502-905-3708

Here’s what’s happening: For several years, FHA has insured loans to buyers who previously would have been considered too risky or marginal at best. Those applicants often carried crushing monthly personal debts — for credit cards, auto loans, student loans and other obligations — totaling more than half of their monthly incomes. Many also had histories of credit problems that lowered their credit scores. Combined with skimpy down payments of 3.5 percent and minimal bank reserves, these borrowers have a high statistical probability of defaulting on their loans.

To prevent big losses to FHA’s insurance fund, the agency recently informed lenders nationwide that from March 18 onward, it would be applying more stringent standards to applications from high-risk home-buyers. In its letter, FHA documented its reasons for the crackdown. According to FHA Commissioner Brian Montgomery, the agency has been seeing disturbing trends in the quality of loans lenders have been delivering to it:

— Nearly one of every four approved home purchasers had a debt-to-income (DTI) ratio exceeding 50 percent, the worst since 2000. In January, 28 percent of buyers were in that category.

— FICO credit scores are tanking. They’ve fallen to the lowest level since 2008 — an industry-low average of 670. In the first quarter of fiscal 2019, more than 28 percent of all new purchase loans had FICOs below 640. In the same quarter, more than 13 percent of new loans had scores under 620 — 19 percent higher than the same period in the previous fiscal year. (FICO scores range from 300 to 850; low scores predict higher risks of nonpayment. Average scores for purchasers at giant mortgage investors Fannie Mae and Freddie Mac average around 750.)

— Borrowers are siphoning equity from their homes at an alarming rate. In fiscal 2018, FHA saw a 60 percent increase in “cash-out” refinancing as a percentage of all refinancings. Cash-outs allow borrowers to convert equity into spendable money.

— Growing numbers of loans have multiple indications of serious future risk of nonpayment — combinations of low credit scores of 640 or less and DTI ratios that exceed 50 percent.

Given these omens, FHA clamped down by amending its automated underwriting system. Lenders must now conduct time-consuming “manual” analysis of every new loan application flagged as high risk. Compared with standard automated underwriting, manual processing is far more intensive and entails higher staffing costs and liabilities for lenders. Many balk at it. Some investors refuse to buy manually underwritten loans. As a result, fewer of them make it through the process.

“Absolutely they’re going to turn a lot of loans down,” said Skeens. Joe Metzler, a loan officer at Mortgages Unlimited in St. Paul, Minnesota, welcomes the stricter standards. “FHA has become the dumping ground for crappy [loan] files with ridiculous DTI allowances and bad scores,” he said. “A lot of it lately has been straight-up subprime. We should not be doing them.”

According to FHA, nearly 83 percent of its home-purchase loans in January went to first-time buyers. Just under 40 percent went to minorities. Those who have the weakest financial profiles — FICO scores under 640 with debt ratios above 50 percent — could be shocked when they go to buy a house this spring. They may have to turn to subprime lenders who charge much higher interest rates, or they may have to simply postpone their purchase until they’re in better financial shape.

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

fax: 502-327-9119

email: kentuckyloan@gmail.com

email: kentuckyloan@gmail.com

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Credit Inquiries--How much do they effect my score?

Credit Inquiries Are A Formal Process

A "credit inquiry" is a formal request to review a person's credit report.

Credit inquires are grouped with other traits into a credit-scoring category called "New Credit". New Credit represents 10 percent a person's complete credit score. On the scale of 300-850, therefore, credit inquiries represent a tiny portion of a maximum of 85 points to a FICO.

There are many times of credit inquiries, but really only 4 of the set can impact a person's credit score:

1. A credit check for a mortgage loan

2. A credit check for an auto loan

3. A credit check for a credit card application

4. A credit check for a store credit card, or consumer loan

These 4 types are singled out because, in each case, the inquiry is made by the applicant in order to get access to more debt. Because extra debt increases the probability of default, credit inquiries can sometimes foreshadow trouble.

Even then, however, the risk of default varies by application type.

For example, credit card applications can be more damaging to a credit score than a mortgage application. This is because credit card debts tend to revolve higher over time versus a mortgage which eventually pays down to $0.

So, all things equal, a credit card application will harm your credit score more than an application for a home loan.

A Credit Inquiry Lowers Your FICO By 5 Points

When compared to the other credit scoring elements, Credit Inquiries is a relative nothing.

In the official FICO scoring model, Payment History and Credit Utilization account for 65% of a score, combined, and the amount of time during which you've had credit to your name accounts for 15%. These three areas are over-weighted because the bureaus are more concerned with what you've already done with your credit versus what you might do with more of it.

Your credit past is the best clue to your credit future and it's one of two reasons why it's okay to give your social security number to as many lenders as you want. The impact of a credit inquiry is tiny next to the value of being a Model Credit Citizen.

A mortgage credit inquiry is estimated to lower a credit score by just 5 points.

Unfortunately, we'll never know for sure because the very act of examining the credit score causes it to move. In Chemistry, this is called the Heisenberg Principle. On MTV, it's called The Jersey Shore Syndrome. Put a camera on something, and it changes.

The Credit Bureaus Don't Hit Your FICO Twice

The second reason you should shop around with lenders is that -- unlike applying for multiple credit cards -- applying for multiple mortgages won't count as multiple, consumer-initiated inquiries. This is a common thing.

You might apply for 5 credit cards and use them all. You're not going to be approved for 5 mortgages.

As such, the credit bureaus have made it formal policy to permit "rate shopping". Talk to as many lenders as you want in a 14-day time frame; have your credit checked as often as you'd like; compare rates and fees. All of the inquiries will be lumped into a single application.

It's good for you and it's good for the bureaus. Your credit scores stay high and TransUnion, Equifax and Experian collect more fees from the banks.

Advice From The Credit Bureaus On Getting Low Rates

To promote rate shopping and to lessen The Fear of Credit Inquiry, the people behind the FICO brand spell out for you the best way to get the best mortgage rates possible:

1. If you want the best rate, you should "shop around"

2. Limit rate shopping to 14-day timespan to keep your credit scores high

3. Mortgage lenders can't give accurate rate quotes without a credit score so give up your social security number

Metaphorically, not letting your lender see your FICO is like not letting your doctor check your blood pressure. You'll get a diagnosis when the appointment is over -- it just might not be the right one.

Joel Lobb

Senior Mortgage Loan Officer

Fill out my form!

Why Work With Me?

Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs.

Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly.

Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs.

Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process.

About My Website

Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find:

Step-by-step guides for first-time homebuyers.

Information on loan programs like FHA, VA, USDA, and KHC.

Tools to help you calculate potential payments and affordability.

Blog posts with tips and updates on the Kentucky housing market.

A secure portal to start your loan application and upload documents.

Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

Subscribe to:

Posts (Atom)