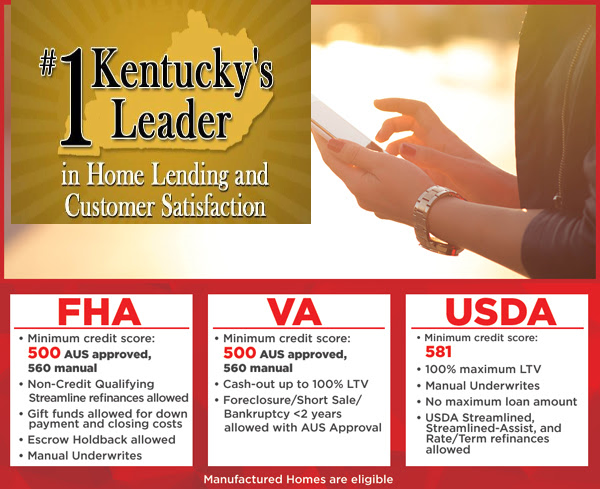

The credit score requirements for Kentucky FHA home loans:

FHA says on paper in their written guidelines that they will insure a FHA loan down to 500 - 579 with a 10% down payment or 580+ with a 3.5% down payment. However, in the real world of lending in the secondary market, most lenders will not adhere to these guidelines.

Most FHA investors will want a 620 middle credit score, but they're a few that will go by the written FHA guidelines above for credit scores, but very few. Your best bet is to get with a loan officer and get your scores up to at least 580 so you can have a better shot of getting approved and access to more FHA lenders.

Bankruptcy Requirements for Kentucky FHA Home Loans:

FHA states in their published guidelines that if you had a Chapter 7 Bankruptcy, you must wait 2 years from the discharge date to reapply for a FHA insured mortgage loan.

If you had a Chapter 13 Bankruptcy and have a 12 month on-time payment history with the courts, you can potentially get approved for a FHA loan if you get permission from the trustee and qualify with the Chapter 13 payment plan in your debt-to-income ratio. If you have been in the plan for over 12 months, and have a good pay history, you can submit your paperwork for FHA approval.

For example, let's say you have been in the Chapter 13 repayment plan for 3 years and you want to buy a home using FHA financing. You could go ahead and petition the Chapter 13 trustee for approval from the courts to get a home loan. The trustee of the Chapter 13 courts will want to know your new loan payment with the home loan, so make sure you know how much you want to borrow before you apply,.

Collections on Credit Report Requirements for Kentucky FHA Home Loans:

:

If the credit report shows a cumulative balance of $2,000 or more for collection accounts:

The debt(s) must be paid in full prior to or at closing, or

Payment arrangements must be made with the creditor and the monthly payment included in the DTI, or

A monthly payment of 5% of the outstanding balances of each collection must be included in the borrower’s DTI.

Collection accounts of non-borrowing spouses in a community property state must be included in the $2,000 cumulative balance and analyzed as part of the Borrower’s ability to pay all collection accounts. Community property states are Arizona, California, Texas, Washington, and Wisconsin

Short-sale or Foreclosure Guidelines for a Kentucky FHA Loan:

If you have experienced a short-sale or foreclosure, FHA states that you must wait 3 years from the date of the sale to obtain FHA financing again. And important note is this: The waiting period starts not when you were discharged from the home or bankruptcy, the waiting period starts when the home is sold and the deed transferred at the courthouse. This is important to remember because a lot of people think it starts when they vacate the home or when there bankruptcy is discharged if the mortgage was in the bankruptcy, but it does not!!! The date used to end the waiting period starts when the deed is transferred at the courthouse from the owner to back to bank or whomever buyus the home in the default.

Delinquent Federal Debt (Taxes, Student Loans) Kentucky FHA Loan Requirements:

If you have a delinquency with the Federal Government, this could hurt your chances of getting approved for a FHA backed Mortgage Loan. Here is why:

All FHA participants are ran through the CAVIRS Alert System administered by HUD to check to see if the mortgage applicant is delinquent to the Federal Government. This usually arises from an IRS income tax lien, overpayment on a social security claim, or lastly, a defaulted student loan.

A lot of the times FHA borrower don't realize that if they don't pay there Federal backed student loans, they go into default and this will hold you up from getting a FHA loan or possibly they will hold your tax refund.

If you have been delinquent on your student loans, you have to call and get on a 9 month repayment plan with them and they will clear you of your CAVIRS Alert. The payment plan can be as little as 5 or $10 a month, but the important thing is to get started so this will improve your credit rating too along with releasing the liens against you for other federal assistance like tax refunds, social security payments and benefits to name just a few.

I have done many FHA loans in Kentucky where they have rehabbed their student loans if they are backed by Federal government and got them loan after 9 months.

If you happen to have an agreement already worked-out with the IRS or student loan creditors, sometimes we can take that arrangement and get you approved sometime with FHA depending on the lender.

Child Support Obligations Kentucky FHA Loan Requirements:

If the credit report shows a delinquent child support agreement, the FHA Government Underwriter will want to see the current child support agreement and what the monthly payment is so as to make sure they have your debt-to-income ratio figured correctly. You can have a delinquency report of child support on your credit report and still get an FHA loan.

It is okay to be paying child support, a lot of times it shows on a borrower's paystubs, and if so, we simply use that child support obligation to use for debt-to-income ratio qualifying.

Joel Lobb

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

click here for directions to our office

Text/call: 502-905-3708