Criteria

|

Loan Type

| |

FHA

|

USDA

| |

|

3.5%

|

0% – None

|

| .85%

|

0.35%

|

|

1.75

|

1.0

|

|

Per County

|

None

|

|

None

|

YES -per county,etc

|

|

None

|

YES

|

| 580 down to 3.5% 500 score with 10% down payment

| no minimum score

|

There are a few other points that put the Kentucky USDA loan at an advantage over the Kentucky FHA mortgage program such as the appraisal value. USDA appraisal value is normally higher than the selling price. If the appraisal value is more than the purchase price, this becomes an additional advantage for borrowers as the USDA will permit you to roll in closing costs.

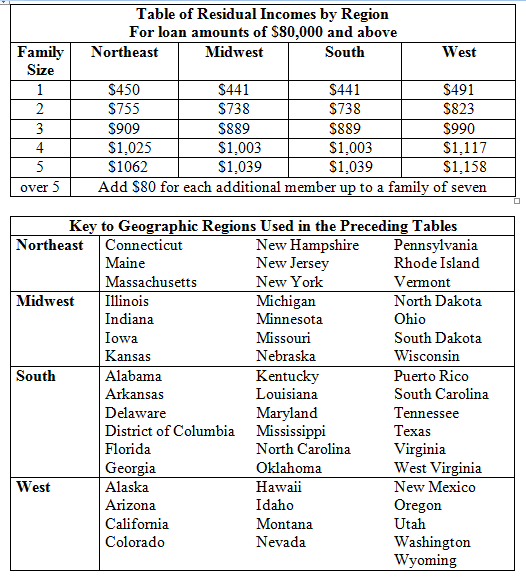

Essentially the only issues that could be considered as drawbacks of the USDA loan are the restriction of location and the USDA RD income limits. The location must be in a designated rural area with a total population of 20,000. This can be a setback for those who do not want to drive farther to get to work in the city. But buyers should check their location in detail, please click here for the USDA housing map. Many populated locations just outside of the big cities are USDA rural housing approved - locations just outside of Louisville, Ky, Lexington Kentucky, and Northern Kentucky Counties..

Additionally, the USDA ‘s income limit imposed on would-be borrowers is currently set at 115% of the median or average income of the area where your home is to be situated. That means for those who have a higher income than the average in town would have to opt for mortgage loans under the FHA or through a conventional lender if they so decide to live in a rural area.

Regarding the rates as well as the guidelines in qualifying potential borrowers, the FHA and USDA are just about equally matched, and they are currently at historic low rates. However, the USDA, unlike the FHA, allows borrowers to finance the whole purchase price and include any closing expenses as well into the loan.

Lastly, all USDA guaranteed loans have a 30-year fixed rate term. This can be very advantageous mainly when the homeowner eventually starts earning more than the required 115% median, the rate is fixed and even after 10 years only, will practically be insignificant compared to other monthly expenses at this time.

The funding fee in both governments backed programs are incorporated (rolled into) into the overall loan.

Apply for FREE Below for your Kentucky FHA Mortgage loan or USDA Loan:

Joel Lobb (NMLS#57916)Senior Loan Officer

502-905-3708 cell

502-813-2795 fax

502-905-3708 cell

502-813-2795 fax

Fill out my form!

Call/Text -

Call/Text -