Kentucky First Time Home Buyer Common Questions and Answers below:👇

∘ What kind of credit score do I need to qualify for different first-time home buyer loans in Kentucky?

Answer. Most lenders will want a middle credit score of 620 to 640 for KY First Time Home Buyers looking to go no money down. The two most used no money down home loans in Kentucky being USDA Rural Housing and KHC with their down payment assistance will want a 620 to 640 middle score on their programs.

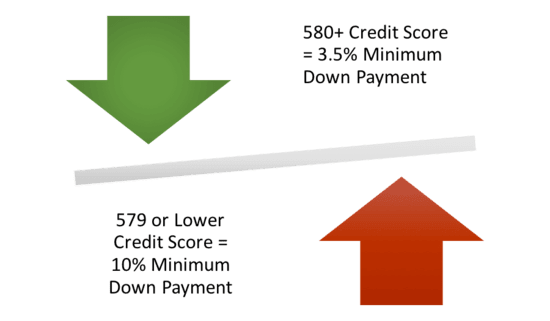

If you have access to 3.5% down payment, you can go FHA and secure a 30-year fixed rate mortgage with some lenders with a 580-credit score. Even though FHA on paper says they will go down to 500 credit score with at least 10% down payment, you will find it hard to get the loan approved because lenders will create overlays to protect their interest and maintain a good standing with FHA and HUD.

Another popular no money down loan is VA. Most VA lenders will want a 580 middle credit score but like FHA, VA on paper says they will go down to a 500 score, but good luck finding a lender for that scenario.

A lot of times if your scores are in the high 500’s or low 600’s range, we can do a rapid rescore and get your scores improved within 30 days.

∘ Does it cost anything to get pre-approved for a mortgage loan?

Answer: Most lenders will not charge you a fee to get pre-approved, but some lenders may want you to pay for the credit report fee upfront. Typically costs for a tri-merge credit report for a single borrower runs about $50 or less. Maybe higher if more borrowers are included on the loan application.

∘ How long does it take to get approved for a mortgage loan in Kentucky?

Answer: Typically, if you have all your income and asset documents together and submit to the lender, they typically can get you a pre-approval through the Automated Underwriting Systems within 24 hours. They will review credit, income and assets and run it through the different AUS (Automated Underwriting Systems) for the template for your loan pre-approval. Fannie Mae uses DU, or Desktop Underwriting, FHA and VA also use DU, and USDA uses a automated system called GUS. GUS stands for the Guaranteed Underwriting System.

If you get an Automated Approval, loan officers will use this for your pre-approval. If you have a bad credit history, high debt to income ratios, or lack of down payment, the AUS will sometimes refer the loan to a manual underwrite, which could result in a longer turn time for your loan pre-approval answer

∘ Are there any special programs in Kentucky that help with down payment or no money down loans for KY First Time Home Buyers?

Answer: There are some programs available to KY First Time Home Buyers that offer zero down financing: KHC, USDA, VA, Fannie Mae Home Possible and HomePath, HUD $100 down and City Grants are all available to Kentucky First Time Home buyers if you qualify for them. Ask your loan officer about these programs

∘ When can I lock in my interest rate to protect it from going up when I buy my first home?

Answer: You typically can lock in your mortgage rate and protect it from going up once you have a home picked-out and under contract. You can usually lock in your mortgage rate for free for 90 days, and if you need more time, you can extend the lock in rate for a fee to the lender in case the home buying process is taking a longer time. The longer the term you lock the rate in the future, the higher the costs because the lender is taking a risk on rates in the future. Interest rates are kind of like gas prices, they change daily

∘ How much money do I need to pay to close the loan?

Answer: Depending on which loan program you choose the outlay to close the loan can vary. Typically, you will need to budget for the following to buy a home: good faith deposit, usually less than $500 which holds the home for you while you close the loan. You get this back at closing; Appraisal fee is required to be paid to lender before closing.

Typical costs run around $400-$450 for an appraisal fee, home inspection fees. Even though the lender’s programs don’t require a home inspection, a lot of buyers do get one done. The costs for a home inspection runs around $300-$400.

Lastly, termite report. They are very cheap, usually $50 or less, and VA requires one on their loan programs. FHA, KHC, USDA, Fannie Mae does not require a termite report, but most borrowers get one done.

There are also lender costs for title insurance, title exam, closing fee, and underwriting fees that will be incurred at closing too. You can negotiate the seller to pay for these fees in the contract, or sometimes the lender can pay for this with a lender credit. The lender has to issue a breakdown of the fees you will incur on your loan pre-approval.

Answer: Most lenders will honor your loan pre-approval for 60 days. After that, they will have to re-run your credit report and ask for updated pay stubs, bank statements, to make sure your credit quality and income and assets has not changed from the initial loan pre-approval.

Answer: The general rule for most FHA, VA, KHC, USDA and Fannie Mae loans is that we run your loan application through the Automated Underwriting systems, and it will tell us your max loan qualifying ratios.

There are two ratios that matter when you qualify for a mortgage loan. The front-end ratio is the new house payment divided by your gross monthly income. The back-end ratio is the new house payment added to your current monthly bills on the credit report, to include child support obligations and 401k loans.

Car insurance, cell phone bills, utilities bills does not factor into your qualifying rations.

If the loan gets a refer on the initial desktop underwriting findings, then most programs will default to a front end ratio of 31% and a back-end ratio of 43% for most government agency loans that get a refer. You then take the lowest payment to qualify based on the front-end and back-end ratio.

So for example, let’s say you make $3000 a month and you have $400 in monthly bills you pay on the credit report. What would be your maximum qualifying house payment for a new loan?

Take the $3000 x .43%= $1290 maximum back-end ratio house payment. So take the $1290-$400= $890 max house payment you qualify for on the back-end ratio.

Then take the $3000 x .31%=$930 maximum qualifying house payment on front-end ratio.

So now you know! The max house payment you would qualify would be the $890, because it is the lowest payment of the two ratios.

There are also lender costs for title insurance, title exam, closing fee, and underwriting fees that will be incurred at closing too. You can negotiate the seller to pay for these fees in the contract, or sometimes the lender can pay for this with a lender credit. The lender has to issue a breakdown of the fees you will incur on your loan pre-approval.

How long is my pre-approval good for on a Kentucky Mortgage Loan?

Answer: Most lenders will honor your loan pre-approval for 60 days. After that, they will have to re-run your credit report and ask for updated pay stubs, bank statements, to make sure your credit quality and income and assets has not changed from the initial loan pre-approval.

How much money do I have to make to qualify for a mortgage loan in Kentucky?

Answer: The general rule for most FHA, VA, KHC, USDA and Fannie Mae loans is that we run your loan application through the Automated Underwriting systems, and it will tell us your max loan qualifying ratios.

There are two ratios that matter when you qualify for a mortgage loan. The front-end ratio is the new house payment divided by your gross monthly income. The back-end ratio is the new house payment added to your current monthly bills on the credit report, to include child support obligations and 401k loans.

Car insurance, cell phone bills, utilities bills does not factor into your qualifying rations.

If the loan gets a refer on the initial desktop underwriting findings, then most programs will default to a front end ratio of 31% and a back-end ratio of 43% for most government agency loans that get a refer. You then take the lowest payment to qualify based on the front-end and back-end ratio.

So for example, let’s say you make $3000 a month and you have $400 in monthly bills you pay on the credit report. What would be your maximum qualifying house payment for a new loan?

Take the $3000 x .43%= $1290 maximum back-end ratio house payment. So take the $1290-$400= $890 max house payment you qualify for on the back-end ratio.

Then take the $3000 x .31%=$930 maximum qualifying house payment on front-end ratio.

So now you know! The max house payment you would qualify would be the $890, because it is the lowest payment of the two ratios.

There are basically 4 mortgage programs for first time home buyers in Kentucky to consider:

1. FHA LOANS IN KENTUCKY

Kentucky FHA loans are a popular choice in Kentucky first time home buyers

because they allow the least down payment of 3.5% and can use down payment assistance to meet the 3.5% down payment requirements.

The current credit score requirements center around the 580-620 score for most FHA loans in Kentucky,

Even though FHA insure a mortgage loan down to a 500 credit score or lower sometimes, it is very

difficult to find a lender that will approve the loan with scores below 580.👀

The house payment will need to be around 30% of your gross monthly income. For example, if

you gross around $3000 a month, then the maximum mortgage payment you would qualify

would be $1000 a month. If the loan comes back as an accept, the debt-to-income ratio can be

substantially higher than the 31% rule.

All FHA loans are pre-approved through an AUS, an automated underwriting system upfront

that will dictate your loan approval. The software underwriting engine looks at your credit, income, assets and figures your loan approval and will recommend an accept, refer/eligible, or refer/ineligible, or out of scope.

Most FHA investors will want a Accept on your underwriting findings to do a loan. It it comes back

referred, then there are additional conditions or overlays that could stop your loan from being approved.

2. Kentucky VA Home Loans

Kentucky VA loans require no down payment, but you must have a VA certificate of Eligibility issued by the Veterans Administration to purchase a home using your VA loan entitlement.

The current credit score that most Kentucky VA lenders want is 580-620. There can be no bankruptcies or

foreclosures in the last two years with good, reestablished credit.

The maximum debt to income ratio is 41% with a residual income of around $1000 a month after you pay all your bills. For example, if you make $4000 gross monthly, then the maximum house payment

along with your other household bills would be set at $3000 a month so as you have the $1000 residual income requirement met.

There are some variances on the residual income to whereas it is based on the number of people living in the household and which state you live in.

Most Kentucky USDA mortgage investors want an Accept on the initial underwriting approval to do the loan or at least a 620 to 640 score to do a manual underwrite on the loan.

640 is the score that most USDA lenders want, but USDA will go down to a 581-credit score in the

guidelines but it is very difficult to get approved. If you have a score below 640 and trying to go USDA, work on getting your credit scores up first.

3. Kentucky USDA/Rural Housing:

Kentucky USDA or Rural Housing loans are not available in the more highly populated counties in Kentucky. The counties of Jefferson and Fayette Counties, parts of Boone, Kenton and Campbell, parts of McCracken County, and parts of Bowling Green, Richmond, Frankfort, Hopkinsville, and Owensboro and Henderson County. are not eligible for USDA loans.

Kentucky USDA loans require no down payment and are subject to income and property eligibility requirements by County.

Check Kentucky USDA Income Limits Here"----->>>>

Check Kentucky USDA Property Eligibility Limits Here--->>>>

All Kentucky Rural Housing Loans are ran through GUS, Guarantee Underwriting System, an

online to determine your loan approval The Automated Underwriting engine will come back with an Accept, Refer, or Ineligible.

Kentucky USDA loans require no down payment and are subject to income and property eligibility requirements by County.

Check Kentucky USDA Income Limits Here"----->>>>

Check Kentucky USDA Property Eligibility Limits Here--->>>>

All Kentucky Rural Housing Loans are ran through GUS, Guarantee Underwriting System, an

online to determine your loan approval The Automated Underwriting engine will come back with an Accept, Refer, or Ineligible.

Most Kentucky USDA mortgage investors want an Accept on the initial underwriting approval to do the loan or at least a 620 to 640 score to do a manual underwrite on the loan.

640 is the score that most USDA lenders want, but USDA will go down to a 581-credit score in the

guidelines but it is very difficult to get approved. If you have a score below 640 and trying to go USDA, work on getting your credit scores up first.

4. Kentucky Housing Corp Down Payment Assistance

KHC recognizes that down payments, closing costs, and prepaids are stumbling blocks for many potential home buyers. We offer a special loan program to help with those. Your KHC-approved lender can help you apply.

Regular DAP

- Purchase price up to $349,525 with Secondary Market.

- Assistance in the form of a loan up to $10,000 in $100 increments.

- Repayable over a 10-year term at 3.75 percent.

- Available to all KHC first-mortgage loan recipients.

More About Down Payment and Closing Costs

- No liquid asset review and no limit on borrower reserves.

- Specific credit underwriting standards may apply to down payment programs.

Secondary Market Eligibility

To qualify for a Secondary Market KHC loan, you must meet the following requirements:

- Meet Secondary Market Income Limits for your county.

- Be a U.S. citizen, other national or qualified alien person

- Have a minimum credit score of 620.

- Be a first-time or repeat homebuyer.

Property Eligibility

The home you wish to purchase must meet the following guidelines.

- Borrower must occupy the home within 60 days of closing and for duration of loan.

- New or previously occupied detached, single-family home.

- New or previously occupied condominium, townhouse, or attached unit in a planned unit development.

- Check with lender for eligible condominiums.

- New or previously occupied manufactured housing, single or double wide, permanently affixed to the foundation and taxed as real estate

- Must meet loan type's foundation requirements.

- The property purchased must be in Kentucky.

Why should I buy, instead of rent?

Answer: A home is an investment. When you rent, you write your monthly check and that money is gone forever. But when you own your home, you can deduct the cost of your mortgage loan interest from your federal income taxes, and usually from your state taxes. This will save you a lot each year, because the interest you pay will make up most of your monthly payment for most of the years of your mortgage. You can also deduct the property taxes you pay as a homeowner. In addition, the value of your home may go up over the years. Finally, you'll enjoy having something that's all yours - a home where your own personal style will tell the world who you are.

What are "HUD homes," and are they a good deal?

Answer: HUD homes can be a very good deal. When someone with a HUD insured mortgage can't meet the payments, the lender forecloses on the home; HUD pays the lender what is owed; and HUD takes ownership of the home. Then we sell it at market value as quickly as possible. Read all about buying a HUD home. Check our listings of HUD homes and homes being sold by other federal agencies.

Can I become a homebuyer even if I have I've had bad credit, and don't have much for a down-payment?

Answer: You may be a good candidate for one of the federal mortgage programs. Start by contacting one of the HUD-funded housing counseling agencies that can help you sort through your options. Also, contact your local government to see if there are any local homebuying programs that might work for you. Look in the blue pages of your phone directory for your local office of housing and community development or, if you can't find it, contact your mayor's office or your county executive's office.

Are there special homeownership grants or programs for single parents?

Answer: There is help available. Start by becoming familiar with the homebuying process and pick a good real estate broker. Although as a single parent, you won't have the benefit of two incomes on which to qualify for a loan, consider getting pre-qualified, so that when you find a house you like in your price range you won't have the delay of trying to get qualified. Contact one of the HUD-funded housing counseling agencies in your area to talk through other options for help that might be available to you. Research buying a HUD home, as they can be very good deals. Also, contact your local government to see if there are any local homebuying programs that could help you. Look in the blue pages of your phone directory for your local office of housing and community development or, if you can't find it, contact your mayor's office or your county executive's office.

Should I use a real estate broker? How do I find one?

Answer: Using a real estate broker is a very good idea. All the details involved in home buying, particularly the financial ones, can be mind-boggling. A good real estate professional can guide you through the entire process and make the experience much easier. A real estate broker will be well-acquainted with all the important things you'll want to know about a neighborhood you may be considering...the quality of schools, the number of children in the area, the safety of the neighborhood, traffic volume, and more. He or she will help you figure the price range you can afford and search the classified ads and multiple listing services for homes you'll want to see. With immediate access to homes as soon as they're put on the market, the broker can save you hours of wasted driving-around time. When it's time to make an offer on a home, the broker can point out ways to structure your deal to save you money. He or she will explain the advantages and disadvantages of different types of mortgages, guide you through the paperwork, and be there to hold your hand and answer last-minute questions when you sign the final papers at closing. And you don't have to pay the broker anything! The payment comes from the home seller - not from the buyer.

By the way, if you want to buy a HUD home, you will be required to use a real estate broker to submit your bid. To find a broker who sells HUD homes, check your local yellow pages or the classified section of your local newspaper.

How much money will I have to come up with to buy a home?

Answer: Well, that depends on a number of factors, including the cost of the house and the type of mortgage you get. In general, you need to come up with enough money to cover three costs: earnest money - the deposit you make on the home when you submit your offer, to prove to the seller that you are serious about wanting to buy the house; the down payment, a percentage of the cost of the home that you must pay when you go to settlement; and closing costs, the costs associated with processing the paperwork to buy a house.

When you make an offer on a home, your real estate broker will put your earnest money into an escrow account. If the offer is accepted, your earnest money will be applied to the down payment or closing costs. If your offer is not accepted, your money will be returned to you. The amount of your earnest money varies. If you buy a HUD home, for example, your deposit generally will range from $500 - $2,000.

The more money you can put into your down payment, the lower your mortgage payments will be. Some types of loans require 10-20% of the purchase price. That's why many first-time homebuyers turn to HUD's FHA for help. FHA loans require only 3% down - and sometimes less.

Closing costs - which you will pay at settlement - average 3-4% of the price of your home. These costs cover various fees your lender charges and other processing expenses. When you apply for your loan, your lender will give you an estimate of the closing costs, so you won't be caught by surprise. If you buy a HUD home, HUD may pay many of your closing costs.

How do I know if I can get a loan?

Answer: Use our simple mortgage calculators to see how much mortgage you could pay - that's a good start. If the amount you can afford is significantly less than the cost of homes that interest you, then you might want to wait awhile longer. But before you give up, why don't you contact a real estate broker or a HUD-funded housing counseling agency? They will help you evaluate your loan potential. A broker will know what kinds of mortgages the lenders are offering and can help you choose a lender with a program that might be right for you. Another good idea is to get pre-qualified for a loan. That means you go to a lender and apply for a mortgage before you actually start looking for a home. Then you'll know exactly how much you can afford to spend, and it will speed the process once you do find the home of your dreams.

How do I find a lender?

Answer: You can finance a home with a loan from a bank, a savings and loan, a credit union, a private mortgage company, or various state government lenders. Shopping for a loan is like shopping for any other large purchase: you can save money if you take some time to look around for the best prices. Different lenders can offer quite different interest rates and loan fees; and as you know, a lower interest rate can make a big difference in how much home you can afford. Talk with several lenders before you decide. Most lenders need 3-6 weeks for the whole loan approval process. Your real estate broker will be familiar with lenders in the area and what they're offering. Or you can look in your local newspaper's real estate section - most papers list interest rates being offered by local lenders. You can find FHA-approved lenders in the Yellow Pages of your phone book. HUD does not make loans directly - you must use a HUD-approved lender if you're interested in an FHA loan.

In addition to the mortgage payment, what other costs do I need to consider?

Answer: Well, of course you'll have your monthly utilities. If your utilities have been covered in your rent, this may be new for you. Your real estate broker will be able to help you get information from the seller on how much utilities normally cost. In addition, you might have homeowner association or condo association dues. You'll definitely have property taxes, and you also may have city or county taxes. Taxes normally are rolled into your mortgage payment. Again, your broker will be able to help you anticipate these costs.

So what will my mortgage cover?

Answer: Most loans have 4 parts: principal: the repayment of the amount you actually borrowed; interest: payment to the lender for the money you've borrowed; homeowners insurance: a monthly amount to insure the property against loss from fire, smoke, theft, and other hazards required by most lenders; and property taxes: the annual city/county taxes assessed on your property, divided by the number of mortgage payments you make in a year. Most loans are for 30 years, although 15 year loans are available, too. During the life of the loan, you'll pay far more in interest than you will in principal - sometimes two or three times more! Because of the way loans are structured, in the first years you'll be paying mostly interest in your monthly payments. In the final years, you'll be paying mostly principal.

What do I need to take with me when I apply for a mortgage?

Answer: Good question! If you have everything with you when you visit your lender, you'll save a good deal of time. You should have: 1) social security numbers for both your and your spouse, if both of you are applying for the loan; 2) copies of your checking and savings account statements for the past 6 months; 3) evidence of any other assets like bonds or stocks; 4) a recent paycheck stub detailing your earnings; 5) a list of all credit card accounts and the approximate monthly amounts owed on each; 6) a list of account numbers and balances due on outstanding loans, such as car loans; 7) copies of your last 2 years' income tax statements; and 8) the name and address of someone who can verify your employment. Depending on your lender, you may be asked for other information.

I know there are lots of types of mortgages - how do I know which one is best for me?

Answer: You're right - there are many types of mortgages, and the more you know about them before you start, the better. Most people use a fixed-rate mortgage. In a fixed rate mortgage, your interest rate stays the same for the term of the mortgage, which normally is 30 years. The advantage of a fixed-rate mortgage is that you always know exactly how much your mortgage payment will be, and you can plan for it. Another kind of mortgage is an Adjustable Rate Mortgage (ARM). With this kind of mortgage, your interest rate and monthly payments usually start lower than a fixed rate mortgage. But your rate and payment can change either up or down, as often as once or twice a year. The adjustment is tied to a financial index, such as the U.S. Treasury Securities index. The advantage of an ARM is that you may be able to afford a more expensive home because your initial interest rate will be lower. There are several government mortgage programs,including the Veteran's Administration's programs and the Department of Agriculture's programs. Most people have heard of FHA mortgages. FHA doesn't actually make loans. Instead, it insures loans so that if buyers default for some reason, the lenders will get their money. This encourages lenders to give mortgages to people who might not otherwise qualify for a loan. Talk to your real estate broker about the various kinds of loans, before you begin shopping for a mortgage.

When I find the home I want, how much should I offer?

Answer: Again, your real estate broker can help you here. But there are several things you should consider: 1) is the asking price in line with prices of similar homes in the area? 2) Is the home in good condition or will you have to spend a substantial amount of money making it the way you want it? You probably want to get a professional home inspection before you make your offer. Your real estate broker can help you arrange one. 3) How long has the home been on the market? If it's been for sale for awhile, the seller may be more eager to accept a lower offer. 4) How much mortgage will be required? Make sure you really can afford whatever offer you make. 5) How much do you really want the home? The closer you are to the asking price, the more likely your offer will be accepted. In some cases, you may even want to offer more than the asking price, if you know you are competing with others for the house.

What if my offer is rejected?

Answer: They often are! But don't let that stop you. Now you begin negotiating. Your broker will help you. You may have to offer more money, but you may ask the seller to cover some or all of your closing costs or to make repairs that wouldn't normally be expected. Often, negotiations on a price go back and forth several times before a deal is made. Just remember - don't get so caught up in negotiations that you lose sight of what you really want and can afford!

So what will happen at closing?

Answer: Basically, you'll sit at a table with your broker, the broker for the seller, probably the seller, and a closing agent. The closing agent will have a stack of papers for you and the seller to sign. While he or she will give you a basic explanation of each paper, you may want to take the time to read each one and/or consult with your agent to make sure you know exactly what you're signing. After all, this is a large amount of money you're committing to pay for a lot of years! Before you go to closing, your lender is required to give you a booklet explaining the closing costs, a "good faith estimate" of how much cash you'll have to supply at closing, and a list of documents you'll need at closing. If you don't get those items, be sure to call your lender BEFORE you go to closing. Be sure to read our booklet on settlement costs. It will help you understand your rights in the process. Don't hesitate to ask questions.

When your down payment is less than 20% you usually have to pay for Private Mortgage Insurance (PMI). This protects the lender in case you don't make your house payments. This doesn't mean you can blow off making your house payments -- if you fail to pay, the bank will still repossess your house. The insurance company will pay the bank the difference between 20% and the amount you actually put down. If you put down 5% and default, the insurance company pays the bank the other 15% that you didn't pay.

So the bank gets protected and you get to pay for their protection.What's in it for you? What's in it for you is that you get to buy a home for less than 20% down! Used to be that banks wouldn't give you a loan under any circumstances unless you made a large down payment because they felt it was too risky. But now with PMI, banks will take loans with very low down payments, sometimes even 0% down. That makes it much easier for you to get into a home.

There's no PMI on VA (veterans) loans, which is a nice bonus if you qualify for one of these.

You don't shop for PMI. If your lender requires it, they'll choose it and add it automatically.

The PMI premium is paid monthly as part of your mortgage payment. The smaller your down payment, the more expensive the PMI is. My PMI Calculator will give you a good estimate.

Another way to do it is to divide the loan amount by 1300, 1500, 2300, or 3700 for loans with down payments of 3%, 5%, 10%, or 15% respectively. For example, let's say you buy a $200,000 home and put 5% down. Your down payment is $10,000 and the morgtage is $190,000. Divide the $190,000 mortgage by 1500 and you get your monthly PMI cost, $127.

Canceling PMI

PMI is usually (but not always) canceled automatically once you own 22% of your home. It used to be that the insurance company would keep happily charging you the premium forever, since many homeowners didn't know they could cancel. This was obviously taking advantage of the uninformed homeowner, so now insurance companies are required by law to automatically cancel your PMI as soon as you own at least 22% of your home, based on the original purchase price, although in some cases they're not required to automatically cancel (which we'll cover in a minute). Assuming you qualify for automatic cancellation, here's how long it will take to reach 22% equity, depending on the length of the loan and the interest rate, ignoring any possible appreciation:

(for 5% / 10% and 15% down payments) | ||

From this table you might think "Wait a minute -- on a 30-year loan I should own about half of my house after about 15 years, but with a 10% interest rate and a 5% down payment you're saying I'd own only 22%?! What gives?"

The answer is that because of how mortgage interest works, most of your payments in the early years goes to interest, not paying down your loan. On a 30-year loan of $100k at 7%, the payment is $665/mo., but when you make the first payment, a whopping $583 goes to interest, and a mere $82 goes towards owning the home. On 15-year loans a much higher percentage goes towards the home itself, which is why 15-year mortgages are a better deal if you can get them -- and why you should try to pay off your loan in 15 years anyway if you can't. There's more on this in our section about paying off a loan early.

But let's get back to PMI and canceling it. Of course, you don't have to wait for the automatic cancellation at 22%. You can write to the insurance company and ask them to cancel your PMI coverage as soon as you hit 20% equity.

And here's one more thing you can do: If your house has increased in value then you suddenly own a lot more of it, and you can cancel your PMI even earlier. For example, let's say you put $5,000 down on a $100,000 home, and in a couple of years the value shoots up to $119,000 because it's a hot real estate market. You own the $5000 you put into the house, plus the $19,000 it increased, for a total of $24,000. (You also own the equity you built from making mortgage payments, but because of how mortgage interest works, most of your payments for the first few years goes to interest and not principal, so we'll ignore paid equity for our example.) So the $24,000 you own divided by the $119,000 value of the home means you own over 20% of your home. So you don't need PMI any more. But to cancel the PMI you'll need to convince the lender that your home is really worth $119,000 now, so you'll have to pay for an appraisal which might run $400 or so. You'll have to weigh the cost of the appraisal against the amount you'll save by canceling PMI early to see if it's a good deal for you.

When PMI is canceled automatically and when it isn't

Don't assume your PMI will be canceled automatically. Check this table.

| Canceled Automaticallyif ALL are true | Not Canceled Automaticallyif ANY are true |

| Conventional loans | FHA loans |

| Loan signed on or after July 29, 1999 | Loan signed earlier than that |

| All mortgage payments have been made on time in the year prior to PMI cancellation | Any mortgage payments have been late |

| Buyer is not considered high risk | Buyer is considered high risk |

References

- Article examining the overall advantage of PMI to homeowners, Auburn University, 1997