I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 900 Kentucky families buy their first home and refinance their current mortgage for a lower rate; Kentucky First time buyers $0 down still available with down payment assistance with KHC. Free Mortgage applications same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS ID 1364

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgage: Kentucky First Time Home Buyer Programs

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgage: Kentucky First Time Home Buyer Programs: What home loan programs are available to first time home buyers in Kentucky? 1. FHA Loans in Kentucky I do not have a lot of mo...

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

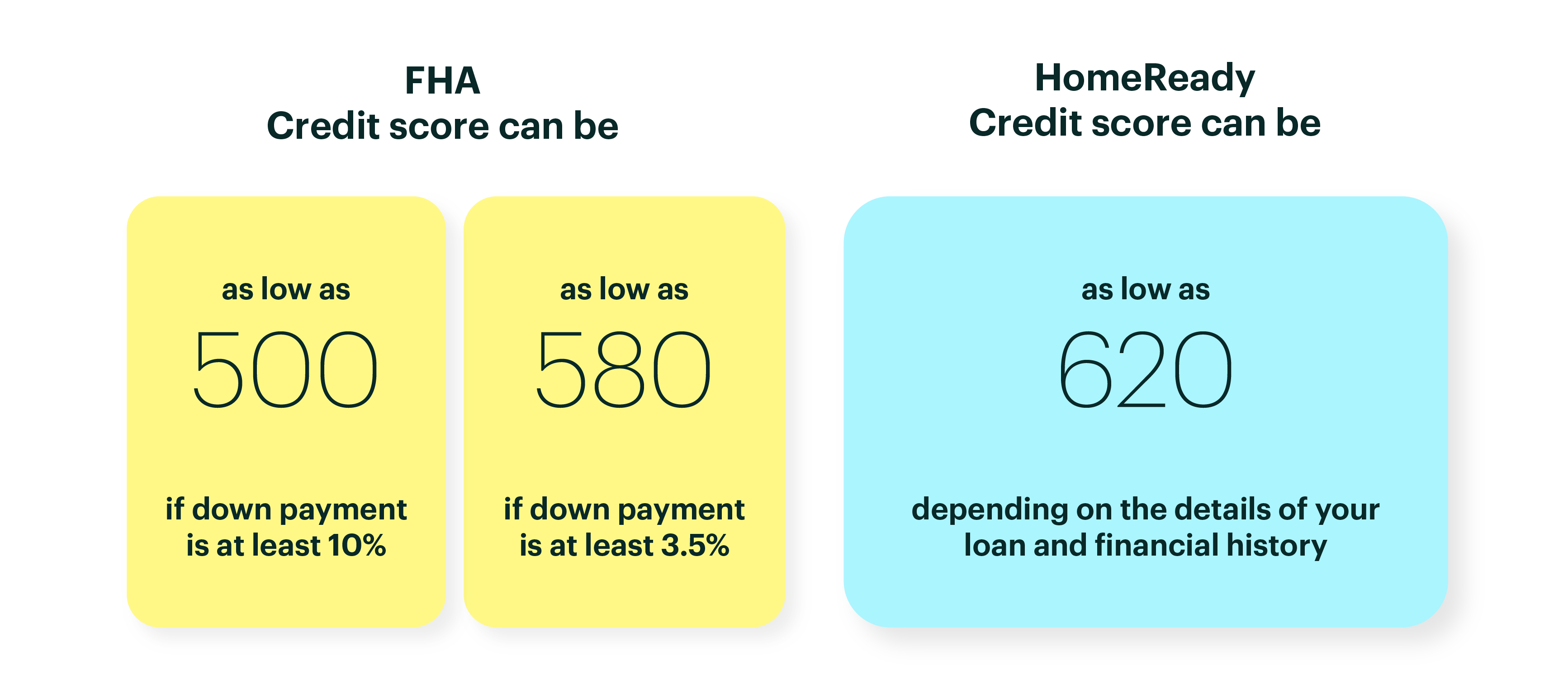

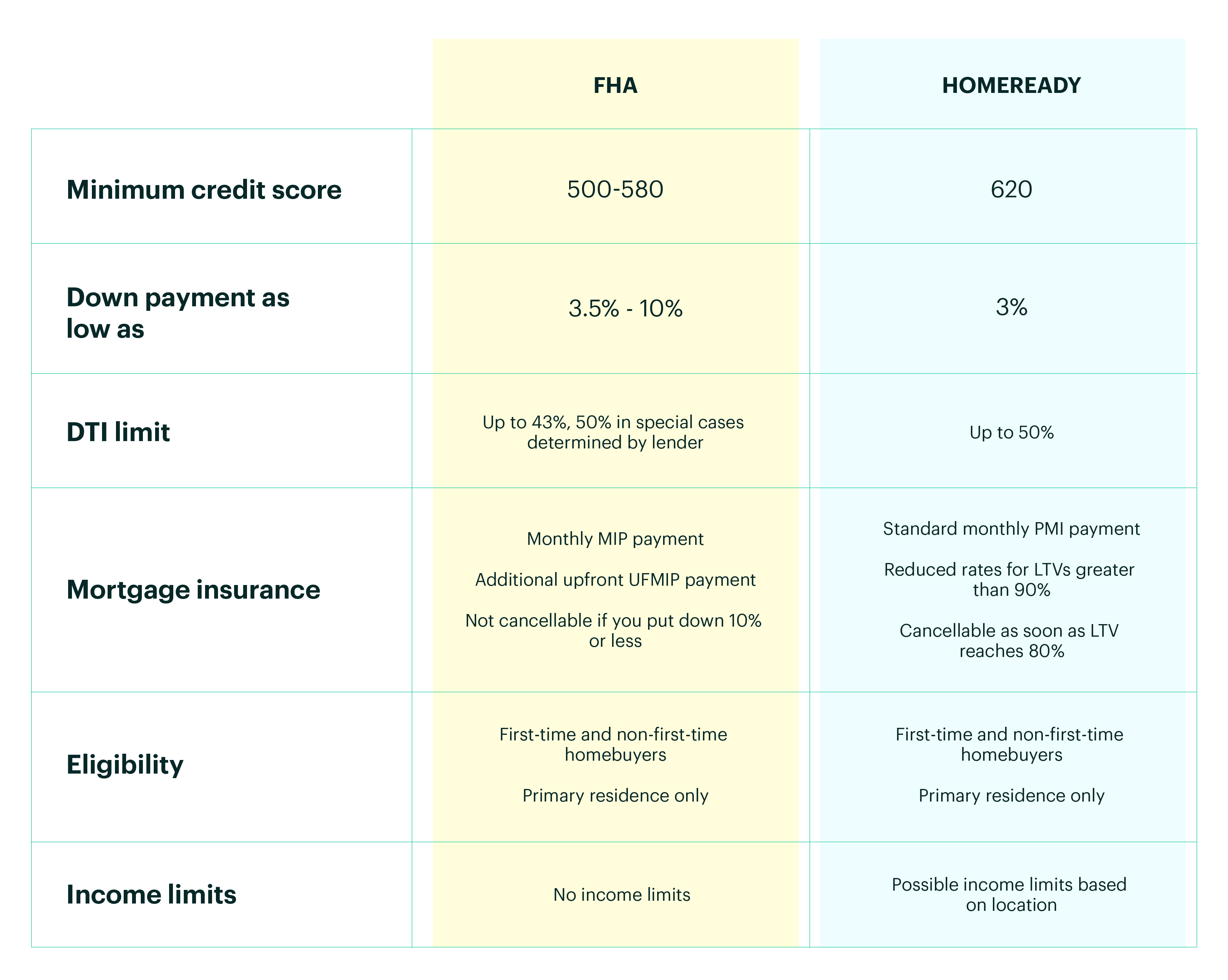

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgage: WHAT IS THE MINIMUM CREDIT SCORE FOR A KENTUCKY FH...

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgage: WHAT IS THE MINIMUM CREDIT SCORE FOR A KENTUCKY FH...: Kentucky FHA Mortgage Credit Score Requirements. FHA is introducing new guidelines on loan to value ratios and the minimum credit sco...

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

Louisville Kentucky VA Home Loan Mortgage Lender: Tips on getting a Kentucky VA Mortgage Guidelines ...

Louisville Kentucky VA Home Loan Mortgage Lender: Tips on getting a Kentucky VA Mortgage Guidelines ...: Getting your Louisville Kentucky VA Loan Approval Run a 25-year loan if you are not getting an approval with a 30-year. Even with higher...

Run a 25-year loan if you are not getting an approval with a 30-year. Even with

higher ratios, 25-year loans are considered lower risk and can be key to getting

an Approve Eligible

• You can do a VA IRRRL on a property that the veteran no longer lives in

• Payoff debts at closing with seller concessions. When writing the offer, this

information goes in the “under additional provisions or other terms” section

• No seasoning requirement for being added to the title (No flip rule)

• Only type of loan where an SAR Underwriter can adjust the value after a

secondary review in Tidewater with a request from the borrower. That gives us

two chances to increase the value if it comes in under.

• You can have more than one at the same time.

• If the DD-214 is a Dishonorable Discharge, the Veteran can re-apply and get their

benefits reinstated and then buy their home. (Apply to the BCMR to upgrade on

basis of clemency)

• No max loan amount & no max amount of closing costs a seller can pay.

• Time of service requirements can be appealed if they are discharged due to a

service-related disability

• Student loans in deferred status that go by old guidelines can be omitted.

• Disputes do not need to be removed to qualify. This is a good trick if you need a

couple extra points. (Disputing collections)

• Time of service requirements can be appealed if they are discharged due to a

service-related disability.

• LP is generally nicer to VA Loans that have derogatory trade lines

Mortgage Application Checklist of Documents Needed below 👇

W-2 forms (previous 2 years)

Paycheck stubs (last 30 days - most current)

Employer name and address (2 year history including any gaps)

Bank accounts statement (recent 2 months – all pages

Statements for 401(k)s, stocks and other investments (most recent)

federal tax returns (previous 2 years)

Residency history (2 year history)

Photo identification for applicant and co-applicant (valid Driver’s License

Joel Lobb (NMLS#57916)

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

NMLS Consumer Access for Joel Lobb

Accessibility for Website

Privacy Policy

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

Kentucky Mortgage: USDA Rural Housing Kentucky Loan Information

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgage: USDA Rural Housing Kentucky Loan Information: A Kentucky USDA home loan is a zero-dollar-down mortgage option provided by USDA’s Department of Rural Development. This government-...

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

FHA Publishes Updates to Handbook 4000.1

FHA Publishes Updates to Handbook 4000.1

FHA announced they are making updates to the 4000.1, which include enhancements, revisions to existing guidance as well as various technical edits. Changes to the Handbook can be implemented immediately but must be implemented for mortgages with case numbers assigned on or after 01/24/2022.

A brief summary of changes to the handbook are as follows:

- Contingent Liabilities

- Guidance was added providing that when a contingent liability is created by a divorce decree or other court order, evidence that the other legally obligated party has made 12 months of timely payments is not required.

- In situations where a copy of the divorce decree ordering the spouse or other legally obligated party to make payments is required, FHA has added for other court orders to be permitted in lieu of the divorce decree.

- Temporary Reduction in Income

- Guidance was added providing that, federal, state, tribal, or local government employees temporarily out of work due to a government shutdown or other similar, temporary events (where lost income is anticipated to be recovered), income preceding the shutdown can be considered as effective income.

- Pre-leave income received prior to and after the first mortgage payment due date is permitted to be used as effective income based on specific criteria.

- Section 8 Homeownership Voucher

- Updated guidance for acceptability of grossing up Section 8 Homeownership Voucher income.

- Documenting the Transfer of Gift Funds

- Guidance was added for gifts of land requiring proof of ownership by the donor and evidence of the transfer of title to the Borrower.

- 203(K) Rehab Program

- Updated list of eligible projects to include the interior space of a condominium unit excluding any areas that are not the responsibility of the Condo Association

- Checking/Savings Accounts

- FHA has removed the requirement for non-borrower parties on a shared account to provide a written statement that the Borrower has full access and use of the funds.

- Payment History Requirements

- Provided clarity that for both Mortgages underwritten through TOTAL Scorecard and manually underwritten, the mortgage payment history for the previous 12 months must be documented.

- Streamline Refinances

- Updated the Streamline Refinance’s Net Tangible Benefit guidance to specify the required minimum term reduction must be 3 years or more.

- Required Inspections for New Construction Financing

- Expanded guidance to allow, in certain circumstances, a qualified trades person or contractor to provide the required inspections and certifications.

- Condo Flood Insurance

- In addition to the form HUD-9991, the following is required (if applicable):

- the certificate of insurance or a complete copy of the NFIP policy; and

- the Letter of Map Amendment (LOMA), Letter of Map Revision (LOMR), or elevation certificate.

- In addition to the form HUD-9991, the following is required (if applicable):

- New Construction

- New construction financing guidance implemented per ML 2020-36 has been incorporated into the Handbook. No guideline changes are being made.

- Appraisal – Changing Markets

- Guidance was added providing alternatives for appraisers in the absence of two credible comparables.

- Valuation of Leasehold Interest

- The calculation of leasehold interest guidance has been removed in consideration of factors that offer advantages and disadvantages affecting value.

Ginnie Mae Clarifies Seasoning Requirements for Modified VA Loans

Ginnie Mae published a clarification on 10/29/2021 to advise that when a new VA refinance is paying off a previously modified non-VA loan that the modified loan is still subject to all current Ginnie Mae seasoning requirements in order to be eligible for a new VA Type I or II refinance.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgage: Louisville Kentucky First Time Home Buyer Programs...

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgage: Louisville Kentucky First Time Home Buyer Programs...: Kentucky First Time Home Buyer Programs and Resources If you are a potential Louisville Kentucky First Time home buyer first time home ...

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

100% Financing Zero Down Payment Kentucky Mortgage Home Loans for Kentucky First time Home Buyers: Common Kentucky Mortgage Myths Busted!My credit sc...

100% Financing Zero Down Payment Kentucky Mortgage Home Loans for Kentucky First time Home Buyers: Common Kentucky Mortgage Myths Busted!My credit sc...: Common Kentucky Mortgage Myths Busted! My credit score or fico score is too low: Most people’s credit scores are better than they think. A...

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

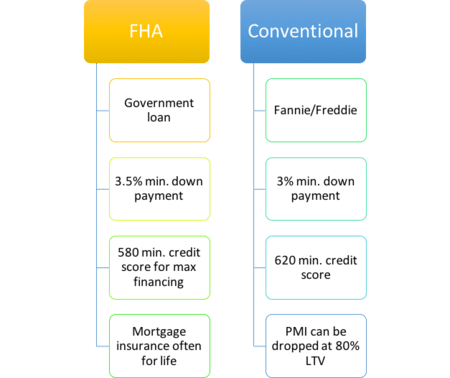

𝗪𝗵𝗮𝘁 𝗶𝘀 𝗮 Kentucky 𝗰𝗼𝗻𝘃𝗲𝗻𝘁𝗶𝗼𝗻𝗮𝗹 𝗹𝗼𝗮𝗻, 𝗮𝗻𝗱 𝗵𝗼𝘄 𝗶𝘀 𝗶𝘁 𝗱𝗶𝗳𝗳𝗲𝗿𝗲𝗻𝘁 𝗳𝗿𝗼𝗺 𝗮𝗻 Kentucky 𝗙𝗛𝗔 𝗹𝗼𝗮𝗻?

Unlike Kentucky FHA loans, conventional loans are 𝙉𝙊𝙏 backed by a government agency, but they do follow specific guidelines set by Conventional Mortgage Kentucky Fannie Mae and Freddie Mac, federally backed companies that buy and guarantee mortgages.

𝗧𝗵𝗲 𝗶𝗺𝗽𝗼𝗿𝘁𝗮𝗻𝘁 𝘁𝗵𝗶𝗻𝗴 for you to know is that conventional loans have many benefits, including:

Down payments as low as 3% No upfront mortgage insurance premium Monthly mortgage insurance that automatically falls off once the home has been paid down to 78% of the home’s value The ability to choose between an adjustable-rate or fixed-rate mortgage with different term lengths Use on different property types, including primary residences, second homes, and investment properties

Down payments as low as 3% No upfront mortgage insurance premium Monthly mortgage insurance that automatically falls off once the home has been paid down to 78% of the home’s value The ability to choose between an adjustable-rate or fixed-rate mortgage with different term lengths Use on different property types, including primary residences, second homes, and investment properties✔ Maximum Loan Limits set each year.

✔ PMI based on credit score and equity position

|

|

|

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

Subscribe to:

Posts (Atom)