I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 900 Kentucky families buy their first home and refinance their current mortgage for a lower rate; Kentucky First time buyers $0 down still available with down payment assistance with KHC. Free Mortgage applications same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS ID 1364

Kentucky First Time Home Buyer Programs

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

Legal Separation vs. Divorce Decree for a Kentucky Mortgage Loan.

- be a legal separation,

- include the same information that would be obtained from a divorce decree,

- be recorded, if required by law. (See Kentucky State Specific Requirements for Divorce and Legal Separation for Kentucky Mortgage Loans in Fairway guidelines)

Property in a Divorce

- What kinds of things are property?

- What happens to our property in a divorce?

- What is the difference between marital and non-marital property?

- Does the court divide marital property 50-50?

- What if I do not agree with what my spouse says is non-marital property?

- What about property from after the separation, but before the divorce is final?

- Will I get half of each asset?

- How do we know the value of our home?

- Will the court allow us to divide our property the way we want to?

- Real property, such as buildings and land, and

- Personal property, such as money in cash or in a financial institution, furniture, jewelry, automobiles, etc.

- Was obtained during your marriage (even if the title is in only one of your names),

- Was given to both of you as a gift, or

- You inherited together.

- You already had when you got married, or

- You inherited or received as a gift individually. (If your spouse says the property was given to both of you, you will have to prove that it was given only to you.)

- Each spouse's financial situation, including income, spousal maintenance, and non-marital property,

- Each spouse's contribution to their marital property,

- Which spouse will stay in the marital home, if there are children, and

- If a spouse improperly destroyed marital property after you separated.

Mortgage Loan Officer

email: kentuckyloan@gmail.com

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

How does consumer credit counseling effects things on a Kentucky FHA or USDA loan in Kentucky ?

KENTUCKY FHA GUIDELINES FOR CONSUEMR CREDIT COUNSELING

(J) Credit Counseling/Payment Plan (APPROVE/ELIGIBLE)Participatin

(K) Credit Counseling/Payment Plan (MANUAL UW) Participating in a consumer credit counseling

- one year of the payout period has elapsed under the plan;

- the Borrower’s payment performance has been satisfactory and all required payments have been made on time; and

- the Borrower has received written permission from the counseling agency to enter into the mortgage transaction.

KENTUCKY RURAL HOUSING USDA GUIDELINES FOR CONSUMER CREDIT COUNSELING

CONSUMER CREDIT COUNSELING - DEBT MANAGEMENT PLANS |

Credit counseling provides guidance and support to consumers which may include assistance to negotiate with creditors on behalf of the borrower to reduce interest rates, late fees, and agree upon a repayment plan. The credit score will reflect the degradation of credit due to participation in this plan. Credit accounts that are included in the repayment plan may continue to report as delinquent or as late pays. This is typical and will not be considered as recent adverse credit. Lenders must retain documentation to support the accounts included in the debt management plan and the applicable monthly payment. Lenders must include the monthly payment amount due for the counseling plan in the monthly liabilities. GUS Accept/Accept with Full Documentation files: No credit exception is required. GUS Refer, Refer with Caution, and manually underwritten files: The following must be documented and retained in the lender’s permanent loan file: •One year of the payment period of the debt management plan has elapsed; •All payments have been made on time; and •Written permission from the counseling agency to recommend the applicant as acandidate for a new mortgage loan debt. •No credit exception is required |

Mortgage Loan Officer

email: kentuckyloan@gmail.com

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

Kentucky USDA Rural Housing Mortgage Lender: Kentucky USDA Rural Housing Guidelines for Debt Ra...

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgages: Kentucky VA Mortgage Loan Information

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

First Time Home Buyer Kentucky DOWN PAYMENT ASSISTANCE KENTUCKY Kentucky First Time Home Buyer Programs

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

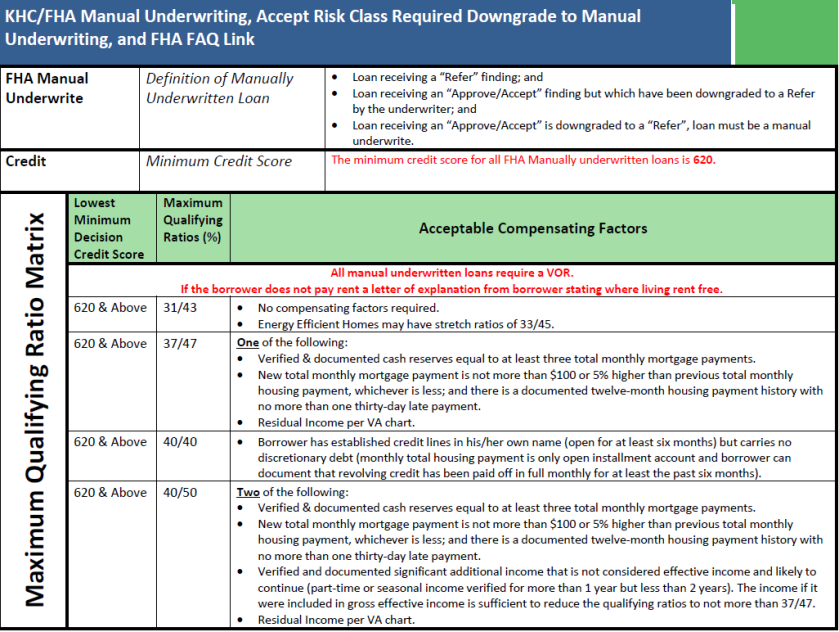

FHA Mortgage Manual Underwriting Video Guidelines

We have the expertise to manually underwrite even the most difficult Kentucky FHA Mortgage loans. Whether it’s purchase or refi—we work hard to approve what other lenders won’t.

Did you know over 50% of our Kentucky FHA loans are manual underwrites?

Kentucky FHA will consider the borrower’s entire story, including extenuating circumstances and compensating factors, to justify loan approvals. If your borrower falls under any of these conditions, they may benefit from manual underwriting:

- Non-traditional credit / lack of credit

- True extenuating circumstances affecting credit or income history

- Lack of seasoning on a Chapter 13

- Disputed accounts over $1,000

- Frequent job changes in the last 12 months

If you think your borrower could benefit from manual underwriting call us to learn more about manual underwriting or submit your scenario today.

Lowest Minimum Decision Credit Score Maximum Qualifying Ratios (%) Acceptable Compensating Factors

All manual underwritten loans require a VOR.

If the borrower does not pay rent a letter of explanation from borrower stating where living rent free.

620 & Above

31/43

• No compensating factors required.

• Energy Efficient Homes may have stretch ratios of 33/45.

620 & Above

37/47

One of the following:

• Verified & documented cash reserves equal to at least three total monthly mortgage payments.

• New total monthly mortgage payment is not more than $100 or 5% higher than previous total monthly housing payment, whichever is less; and there is a documented twelve-month housing payment history with no more than one thirty-day late payment.

• Residual Income per VA chart.

620 & Above

40/40

• Borrower has established credit lines in his/her own name (open for at least six months) but carries no discretionary debt (monthly total housing payment is only open installment account and borrower can document that revolving credit has been paid off in full monthly for at least the past six months).

620 & Above

40/50

Two of the following:

• Verified & documented cash reserves equal to at least three total monthly mortgage payments.

• New total monthly mortgage payment is not more than $100 or 5% higher than previous total monthly housing payment, whichever is less; and there is a documented twelve-month housing payment history with no more than one thirty-day late payment.

• Verified and documented significant additional income that is not considered effective income and likely to continue (part-time or seasonal income verified for more than 1 year but less than 2 years). The income if it were included in gross effective income is sufficient to reduce the qualifying ratios to not more than 37/47.

• Residual Income per VA chart.

Residual Income

Calculating Residual Income

Residual income is calculated in accordance with the following:

• Calculate the total gross monthly income of all occupying borrowers

• Deduct from the gross monthly income the following items:

➢ State income taxes

➢ Federal income taxes

➢ Municipal or other income taxes

➢ Retirement or Social Security

➢ Proposed total monthly fixed mortgage payment

➢ All recurring monthly debt obligations

➢ Estimated maintenance and utilities ($0.14 x sq. ft.)

➢ Job related expenses (e.g., child care)

• The difference between the gross monthly income and the deductions above is the residual income

Compensating Factors

Using Residual Income as a Compensating Factor

Count all members of the household of the occupying borrowers without regard to the nature of their relationship and without regard to whether they are joining on title or the note.

Exception: As stated in the VA Guidelines, the mortgagee may omit any individuals from “family size” who are fully supported from a source of verified income which is not included in the effective income in the loan analysis. These Individuals must voluntarily provide sufficient documentation to verify their income to qualify for this exemption.

From the table below, select the applicable loan amount and household size. If residual income equals or exceeds the corresponding amount on the table, it may be cited as a compensating factor.

Accept Risk Class required downgrade to Manual Underwriting

The Mortgagee must downgrade and manually underwrite any mortgage that received an accept or approve/eligible recommendation if:

• The mortgage file contains information or documentation that cannot be evaluated by TOTAL.

• Additional information, not considered in the AUS recommendation affects the overall insurability of the mortgage.

• The borrower has $1,000 or more collectively in Disputed Derogatory Credit Accounts.

• The date of the borrower’s bankruptcy discharge as reflected on bankruptcy documents is within two years from the date of the case number assignment.

• The case number assignment date is within three years of the date of the transfer of title through a Pre-Foreclosure Sale (Short Sale).

• The case number assignment date is within three years of the date of the transfer of title through a foreclosure sale.

• The case number assignment date is within three years of the date of the transfer of title through a Deed-in-Lieu (DIL) of foreclosure.

• The Mortgage Payment history, for any mortgage trade line reported on the credit report used to score the application, requires a downgrade as defined in Housing Obligations/Mortgage Payment History.

• The Borrower has undisclosed mortgage debt that requires a downgrade.

• Business income shows a greater than 20 percent decline over the analysis period.

• Per AUS Findings.

FHA FAQ link

ML 2014 – 02 on Manual Underwriting was incorporated into the HUD Handbook 4000.1. Additional source for questions will be the FAQ’s. Use “manual underwriting and compensating factors” to searcH

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

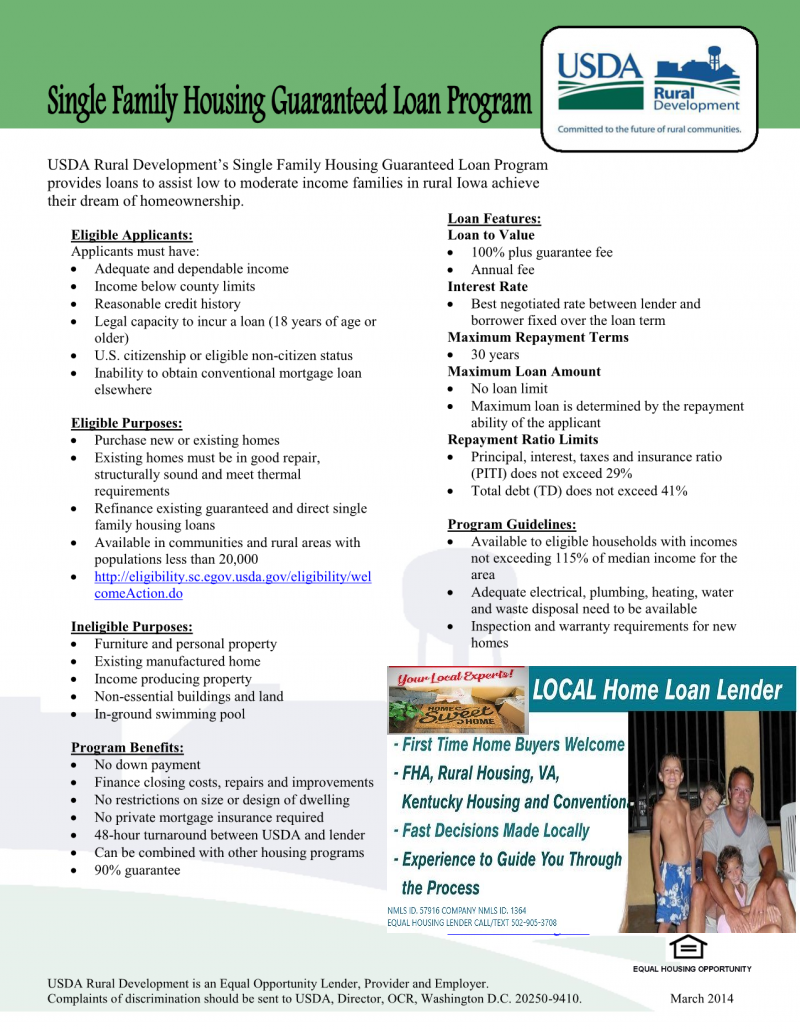

Louisville Kentucky Mortgage Lender for FHA, VA, KHC, USDA and Rural Housing Kentucky Mortgages: USDA Rural Housing Kentucky Loan Information

Kentucky USDA Rural Development Loans Program Guidelines

Loan Purpose of Kentucky Rural Housing Loans

- Purchase

- One-time Close Construction Loan (very few lenders do this)

- Rate-term refinance for existing USDA Loans Only. Cannot refinance a Conventional loan, FHA, VA, or other loans into an USDA loan.

Credit Profile for a Kentucky Rural Housing Buyer

- 581 minimum middle credit score for all borrowers on the loan – purchase

- No score allowed with alternative trade lines

- Most Kentucky USDA lenders will want a 620 or 640 score or higher. A 640 middle score is required for a USDA loan through GUS, the automated underwriting system used by rural development to determine the max lending limits for a loan.

- No foreclosure, short sale, or Chapter 7 bankruptcy discharge within three years of contract ratification date on credit report not permitted

- Minimum of two tradelines on credit, with a positive pay history within the most recent 12-month period. Accounts can be open or closed

- If two tradelines aren’t on credit, alternative tradelines can be

- No mortgage delinquency in the last 12 months for a USDA-to-USDA Refinance

Loan Amount limits for USDA loans in Kentucky.

- No maximum loan amounts. A lot of borrowers think they're max limits on this because there is max limits on total household income by county in Kentucky, but there actually is no limit as long as the borrower gets approved on the ability to repay the loan.

Mortgage Insurance Requirements and Premiums for USDA Loans:

- USDA charges a 1% Commitment Fee that is financed into the loan. Not paid out of pocket but can be

- Commitment Fee can be financed into the loan

Example:

Purchase price - $100,000

Base Loan amount - $100,000

Commitment Fee - $1,010 ($100,000 [purchase price] /.99 - 100,000)

Maximum financed loan amount = $101,010 - USDA requires a monthly Annual Fee (i.e. mortgage insurance premium) with an annual factorial of .35%

- This is much lower than FHA's upfront 1.75% and the monthly mi of .85% so keep that in mind.

Ratios for USDA Loan Approval in Kentucky

- 33.99/45.99% (DTI) with GUS Accept/Eligible underwriting findings

- 29/41% debt-to-income (DTI) with GUS Accept/Refer underwriting findings and credit score less than 679

- 31.99/42.99 with GUS Accept/Refer underwriting findings and credit score greater than 680 and with compensating factors such as:

- 680 or higher credit score

- No or low "payment shock" - less than a 100% increase in proposed mortgage payment Vs. current rental housing expenses

- Fiscally sound use of credit

- Ability to accumulate savings

- Stable employment history with 2 or more in current position or continuous employment history with no job gaps

- Cash reserves available for use after settlement

- Career advancement as indicated by job training or additional education in the applicants profession

- Trailing spouse income - as a result of a job transfer, the house is being purchased, prior to the secondary wage-earner obtaining employment. If the secondary wage-earner has an established history of employment and has a reasonable chance to obtain new employment in the area

- Low total debt load

Property Type for USDA Loan Approval in Kentucky

- Must be located in an eligible USDA Rural Development Location

- Owner-occupied properties---no rental properties or second homes

- Existing attached and detached single-family residences

- New construction with permanent financing only

- PUD's (i.e. Townhomes)

- Condo-units. HUD, VA, FNMA or FHLMC approved project

- Log cabin homes, provided Appraisal Report lists other comparable log cabin homes that have recently sold in the area

- No used or old mobile homes allowed. Only allows new mobile homes from dealer setup on land with mobile home land package deal...Kentucky only. ..

Documentation for loan approval on income/job history for a Kentucky Rural Housing Loan:

- All loans must be fully documented per Agency Guidelines. USDA likes to see a 2 year job history with stable employment. Does not have to be same employer, just a contiguous 2 year work history with no gaps over 30 days.

- If recently graduated form college, sometimes they will waive the 2 year job history rule if show transcripts and be on your job for 6-12 months. Case by case here.

- For Self Employed borrowers, in addition to Agency Guidelines, two years of the tax returns (personal and business) along with a year-to-date profit and loss (unaudited)

- If overtime or bonus income or second job is used to qualify, you can take a 2 year avg and as long as stable and not decreasing, you can usually this income to qualify.

- They usually will take your base gross income to qualify you on the mortgage loan. They don't qualify you off your net income.

Down Payment/Closing Costs for a USDA loan in KY

- 0% down payment required, but if you have available 20% down payment in checking or savings, they will make you use that..If the money is in a tax-deferred or 401k plan, retirement plan, they will not hold this against you.

- Seller contribution toward buyers closing costs up to 6% of the purchase price

- Closing cost help can come from flexible sources including family member gifts and loans against a 401k retirement account

- If the appraised value of the property exceeds the purchase price, the difference can be used to cover closing costs---This is a key benefit of Kentucky USDA loans. This is the only type of loan that will allow this.

Terms

- Amortization period: 30-year fixed rate-They do not offer any other terms. Just a 30 year fixed rate loan with no prepay penalty.

Existing Properties Owned

- USDA primarily often won't allow applicants to own other properties

- Exceptions include when the other property owned is:

- Not owned in the local commuting area as the new property; or

- Not structurally sound and/or functionally adequate

- Manufactured home not on a permanent foundation

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.