Kentucky VA Mortgage Question and Answers for Qualifying for A VA Home Loan in KY?

|

I have a website below about me so check it out. I have great reviews and will get you the best deal out there on your loan.

I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 900 Kentucky families buy their first home and refinance their current mortgage for a lower rate; Kentucky First time buyers $0 down still available with down payment assistance with KHC. Free Mortgage applications same day approvals. Web site is not endorsed by the FHA, VA, USDA govt agency. Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS ID 1364

Kentucky VA Mortgage Question and Answers for Qualifying for A VA Home Loan in KY?

|

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I specialize in Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans. I have helped over 900 Kentucky families buy their first home and refinance their current mortgage for a lower rate; Kentucky First time buyers $0 down still available with down payment assistance with KHC. Free Mortgage applications same day approvals.

Web site is not endorsed by the FHA, VA, USDA govt agency.

Text/call 502-905-3708 kentuckyloan@gmail.com NMLS 57916 NMLS ID 1364

http://www.mylouisvillekentuckymortgage.com/

#homebuyers #mortgage #housing #fhaloan #usdaloan #valoan #homeloan #kentuckymortgage #louisvillemortgage #firsttimehomebuyers

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

New 2023 Loan Limits for Kentucky VA and Kentucky FHA Loans |

Kentucky VA loan limits received a massive increase for 2023. The standard Kentucky VA loan limit in 2023 is $726,200 for most U.S. counties, increasing from $647,200 in 2022. Kentucky VA loan limits also increased for high-cost counties to $1,089,300 for a single-family home.

Kentucky VA loan limits do not represent a cap or max loan amount. Veterans with their full entitlement can get as much as a lender is willing to give them without needing a down payment. However, Veterans with one or more active VA loans or who have defaulted on a previous VA loan will encounter the limits, which will in part determine their zero-down buying power.

For Kentucky FHA loan limits, please click here to consult this page on the Hud.gov website as Loan Limits for FHA loans vary by county in Kentucky each 120 counties. |

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

COMMON KENTUCKY VA LOAN MYTHS FOR KENTUCKY VETERANS

Is it hard to qualify for a VA loan?

Myth #1: Kentucky VA loans are difficult to qualify for.

Fact: VA loans have fewer credit restrictions compared to conventional loans. These reduced restrictions, like a higher debt-to-income (DTI) ratio and more leniency regarding credit scores, mean it can be easier to qualify. VA has no minimum credit score but lenders will have overlays with most being 620 and some going down to 580, with a few going all the way down to 500 but it is very difficult to get approved at this level --- though each individual case and lender will vary.

Do VA loans require a down payment?

Myth #2: All Kentucky VA loans require a down payment.

Fact: While conventional loans generally require down payment options that can reach up to 20%, no such thing is required with a VA home loan at or under the local conforming limit. Down payments are still an option, of course, but they are not a requirement.

The VA allows you to purchase jumbo loans, but the down payment depends on your entitlement:

Do VA loans have PMI?

Myth #3: VA loans require private mortgage insurance (PMI).

Fact: Private mortgage insurance is not required for VA loans. PMI typically adds 0.2%-0.9% of expenses to your monthly mortgage payments when you put less than 20% down. That’s a big additional expense you don’t have to worry about when you get a VA loan. Remember, VA loans do come with a funding fee.

Can you refinance a VA loan?

Myth #4: You can’t refinance a Kentucky VA loan.

Fact: Thanks to VA streamline and cash-out loan programs, VA loans are actually easier to refinance than conventional mortgages. The streamline version lowers the mortgage rate of an already existing VA loan, usually for less than the current principal and interest. This means it doesn't require a credit check or appraisal. The cash-out option involves a credit check and appraisal, since the home’s value represents the maximum loan amount and the new loan will be larger than the existing loan.

How many VA loans can you have?

Myth #5: You can only have one Kentucky VA loan.

Fact: There is no limit to the number of VA loans you can have. While it is possible to have multiple VA loans at once, this depends on VA loan entitlement. VA loan entitlement refers to the amount that the VA will pay your lender if you default on your loan. There is a limit on your VA entitlement. It can be split across multiple loans but the limit remains the same. For full entitlement, the VA covers:

If, however, you’ve used a portion of your entitlement in one loan that you’re still actively paying off (or defaulted on), the amount of entitlement you have on any new loan is reduced. This means that you may need to put money down yourself instead of having the usual benefit of a zero down payment for VA loans. To learn about VA loan limits and entitlement, visit us here.

How many times can you use a VA loan?

Myth #6: You can only use a Kentucky VA loan once.

Fact: There is no limit on the number of times you can use the VA loan benefit. You can use the benefit an unlimited number of times throughout your life, as long as you still qualify. To qualify, you need to meet certain requirements, which you’ll already be aware of if you’ve taken out a VA loan in the past. For those who haven’t taken out a VA loan prior, you can learn how to qualify here.

Are VA loans assumable?

Myth #7: Kentucky VA loans are not assumable.

Fact: Federally insured and guaranteed loans are usually assumable. This includes VA loans. What does it mean if a loan is assumable? An assumable mortgage is when the lender allows you, the buyer, to take over the current mortgage that the seller has. This can save a lot of money if the interest rates are lower on the existing mortgage than they would be to take out a new mortgage. Assumable mortgages allow buyers, who otherwise wouldn’t qualify for a VA loan, to take over a VA mortgage. This means that you would get most, if not all, of the benefits that come with VA loan eligibility. In order to assume a VA mortgage, you will need to meet certain requirements, such as:

You will also be required to pay the VA funding fee that comes with VA loans. This equates to 0.5% of the total loan amount. This may be waived if you’re an eligible military borrower who qualifies for an exemption. Other fees may be required as well.

For sellers, if a non-military borrower assumes your mortgage, your VA entitlement won’t be restored until the loan is paid in full. You will want to request that the lender releases you from liability on the loan to avoid dips in your credit reports if the buyer defaults or makes a late payment.

Can you buy land with a VA loan?

Myth #8: You can’t buy land with a Kentucky VA loan.

Fact: The VA doesn’t authorize buyers to singularly purchase land with a VA loan. However, you can purchase land and build a home on it. This is partially because VA loans are granted with a required occupancy period — you must use the property as your primary residence for at least one year. If there is already a home on the land, this is acceptable. Another acceptable scenario is if you plan to immediately build a home on the land after purchase. This may require a purchase/construction loan.

You can also purchase land with a conventional loan or certain other types of loans. Then you can build a home on the land using a VA construction loan. Upon completion, military borrowers can refinance VA construction loans into permanent VA loans. Builders must be VA-approved.

Finally, you can purchase land and build a property using a non-VA purchase/construction loan. Then you can refinance the loan upon completion of the build into a permanent VA loan (as long as the property meets the VA’s requirements).

Can you use a VA loan to build a house?

Myth #9: You can’t build a house with a Kentucky VA loan.

Fact: VA construction loans do exist, as mentioned above, and under the right circumstances, they can be refinanced into permanent VA loans. Ask your lender about VA purchase/construction loan options.

Can you use a VA loan for home improvement?

Myth #10: Kentucky VA loans only apply to the home purchase itself.

Fact: The VA allows for increases to purchase loans for the purpose of making renovations. The VA’s Energy Efficiency Mortgage program, for instance, lets borrowers add up to $6,000 to their home loan amount to install solar heating, insulation and storm windows, among other features.

In conclusion

Applicant subject to credit and underwriting approval. Not all applicants will be approved for financing. Receipt of application does not represent an approval for financing or interest rate guarantee does not guarantee the quality, accuracy, completeness or timelines of the information in this publication. While efforts are made to verify the information provided, the information should not be assumed to be error free.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

Run a 25-year loan if you are not getting an approval with a 30-year. Even with

higher ratios, 25-year loans are considered lower risk and can be key to getting

an Approve Eligible

• You can do a VA IRRRL on a property that the veteran no longer lives in

• Payoff debts at closing with seller concessions. When writing the offer, this

information goes in the “under additional provisions or other terms” section

• No seasoning requirement for being added to the title (No flip rule)

• Only type of loan where an SAR Underwriter can adjust the value after a

secondary review in Tidewater with a request from the borrower. That gives us

two chances to increase the value if it comes in under.

• You can have more than one at the same time.

• If the DD-214 is a Dishonorable Discharge, the Veteran can re-apply and get their

benefits reinstated and then buy their home. (Apply to the BCMR to upgrade on

basis of clemency)

• No max loan amount & no max amount of closing costs a seller can pay.

• Time of service requirements can be appealed if they are discharged due to a

service-related disability

• Student loans in deferred status that go by old guidelines can be omitted.

• Disputes do not need to be removed to qualify. This is a good trick if you need a

couple extra points. (Disputing collections)

• Time of service requirements can be appealed if they are discharged due to a

service-related disability.

• LP is generally nicer to VA Loans that have derogatory trade lines

W-2 forms (previous 2 years)

Paycheck stubs (last 30 days - most current)

Employer name and address (2 year history including any gaps)

Bank accounts statement (recent 2 months – all pages

Statements for 401(k)s, stocks and other investments (most recent)

federal tax returns (previous 2 years)

Residency history (2 year history)

Photo identification for applicant and co-applicant (valid Driver’s License

Joel Lobb (NMLS#57916)

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

NMLS Consumer Access for Joel Lobb

Accessibility for Website

Privacy Policy

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

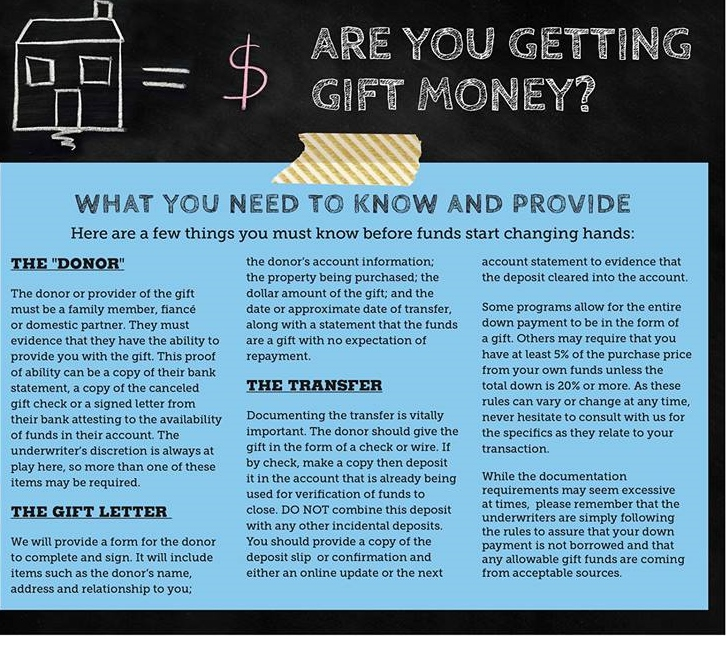

For many Kentucky first time buyers, saving for a down payment is one of the most challenging steps in fulfilling their dream of purchasing a home. Oftentimes, they know they can afford their potential monthly mortgages (which could be less or equal their current rents), but the upfront costs of buying, such as down payment and closing costs, may be too much for them to pay.

This is why it's possible to get a little help in the form of a down payment gift from a family member or relative, close friend, or even a charitable organization. And it’s actually becoming more popular, especially among millennials. In the National Association of REALTORS® 2020 Generational Trends Report, 13 percent of home buyers (and 27 percent for ages 22 to 29) indicated their source of down payment to be a gift from their relative or friend.

So if you’re lucky enough to find down payment fund as one of your gifts under the Christmas tree this year (or maybe you’re the one who wants to give it), it may not be as simple as opening your cash gift (or handing someone a wad of cash) and going straight to the lender to use it to buy a home.

Down payment gift funds, whether you’re giving or receiving it, are closely regulated by lenders and must meet certain requirements. Here are certain rules that the gift giver and recipient should know to avoid trouble down the road.

While we may automatically consider a family member, like parents or siblings, when thinking about who can give a mortgage down payment gift, there are other entities who could also be eligible gift sources. But because cash can come with strings attached, and lenders want to make sure that the gift money is nothing but a gift (which will be discussed later on), there are restrictions on who can give money (or who you can give money to) to help purchase a home.

If you are getting a loan through Fannie Mae or Freddie Mac, gifts can only be from a family member or relative. This may be your spouse, child, siblings, parents, grandparents, or anyone related by blood, marriage, adoption, or legal guardianship. Soon-to-be family members such as your domestic partner, fiancé, or even future in-laws are also eligible to give funds for a down payment.

The Federal Housing Administration (FHA) has its own set of rules when it comes to giving or receiving down payment gifts, although they offer a broader eligibility range. If you are getting an FHA loan, you can receive down payment funds from family members, friends who have a clearly defined and documented interest in your life, employers, labor unions, government agencies, and even charitable organizations.

VA loans (backed by the U.S. Department of Veterans Affairs) and USDA mortgages (given by the U.S. Department of Agriculture)may have fewer restrictions, but the down payment gift funds cannot come from anyone who would benefit from the proceeds of the purchase, such as the seller, developer, builder, your real estate agent, and some other entity.

There are no limits on the amount of money someone can give you for a down payment or to cover closing costs. However, rules still apply depending on the type of loan and property you're purchasing. Some types of loans may need you to contribute a certain amount of the down. The key is to check with your lender for the latest regulations on how much you can really use.

Likewise, there can be tax implications on the person giving the gift funds. They may be liable if the amount exceeds the gift tax exclusion limit. As of 2020, for instance, any individual can give funds up to $15,000 without a tax penalty. On the other hand, parents who are married and are filing jointly can give up to $30,000 per child for a mortgage down payment (or any other purpose), without incurring the gift tax. For a down payment gift that exceeds the said amounts, the donor must file a gift tax return to disclose the gift.

You need to confirm the relationship between you and the giver and provide the right paperwork.

If you're fortunate enough to have a family member or any eligible entity who can give you funds towards your home’s down payment, you’ll need to confirm your relationship with the gift-giver and provide your mortgage underwriter more information about where the funds came from.

For lenders to confirm that the new money isn’t a loan, you’ll need these things:

1. A down payment gift letter - If your lender has a template letter for this purpose, you will need to send it to the funds’ donor. If there isn’t a template, you might want to ask what information should be included so you can draft your own.

The letter typically includes details about the gift-giver, such as the name, address, contact phone, relationship to the borrower, and address of the property to be purchased. The date when the gift was transferred and the amount of funds given to the borrower must also be indicated. The donor should also write a sentence explaining that the fund is a gift and that there isn’t any expectation of repayment. The letter must be signed by both the gift-giver and the borrower.

2. The gift-giver’s bank statements - This is to show they have the funds to give the buyer as much money as promised.

3. A bank slip from the buyer’s account - This is to indicate when the money was transferred, to verify that the cash is from a legitimate source and that the borrower has an appropriate relationship with the donor, and to confirm the information provided in the letter.

Remember: you can't pay back the gift.

Down payment gift funds need to be just like that—a gift and not a loan that is expected to be paid. You need to make it clear with your mortgage lender that the money you received was entirely gifted and not something that you need to pay back eventually, because by then it will be considered mortgage or loan fraud. Besides, it can also put your loan qualification at risk since your debt-to-income ratio will be factored when you get a mortgage.

Try to make it a “seasoned” gift money.

It might make more sense to try and make your gift money “seasoned”, especially if you know that someone is going to help you buy a home (often in the case of parents or other relatives). Lenders refer to it as seasoned money when it has been sitting in your bank account for some time, at least for two months. When the gifted money is given in advance, you often don't have to worry about writing gift letter documentation.

Down payment gift funds make it easier for first-time home buyers to afford a home. If you anticipate accepting help, remember to consider the rules above so you can accept such a gift in a proper manner. Be upfront with your mortgage lender if you plan on using gift funds for the down payment. Don't forget to also talk to the individual or entities who are planning to give you money about the tax implications and other considerations.

--

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.

I have helped over 1300 Kentucky families buy or refinance their home over the last 20 years. Realizing that this is one of the biggest, most important financial transactions a family makes during their lifetime, I always feel honored and respected when I am chosen to originate their personal home loan. You can count on me to deliver on what I say, and I will always give you honest, up-front personal attention you deserve during the loan process.

I have several advantages over the large banks in town. First, I can search and negotiate for your loan options through several different mortgage companies across the country to get you the best deal locally. Where most banks will offer offer you their one set of loan products. I have access to over 10 different mortgage companies to broker your loan through to get you the best pricing and loan products that may not fit into the bank's program due to credit, income, or other underwriting issues.

You will not get lost in the shuffle like most borrowers do at the mega banks; you're just not a number at our company, you are a person and we will treat you like one throughout the entire process.